The post-COVID inflation surge was global, but inflation persistence was not. This column argues that the key difference lies in how strongly external shocks fed into domestic inflation dynamics through expectations, wages, and energy-price transmission. Countries with histories of higher inflation and stronger energy pass-through experienced substantially more persistent inflation, while credible policy frameworks helped contain second-round effects. Temporary energy-price smoothing through subsidies also reduced inflation propagation in some cases. In a world with more frequent supply shocks, the policy challenge may shift from preventing inflation shocks altogether to preventing them from becoming structurally embedded in domestic inflation dynamics.

For much of 2024 and 2025, policymakers increasingly converged on a reassuring narrative. The inflation surge had largely been defeated. Headline inflation rates declined across most advanced and emerging economies, energy prices stabilised, and central banks cautiously began discussing eventual normalisation.

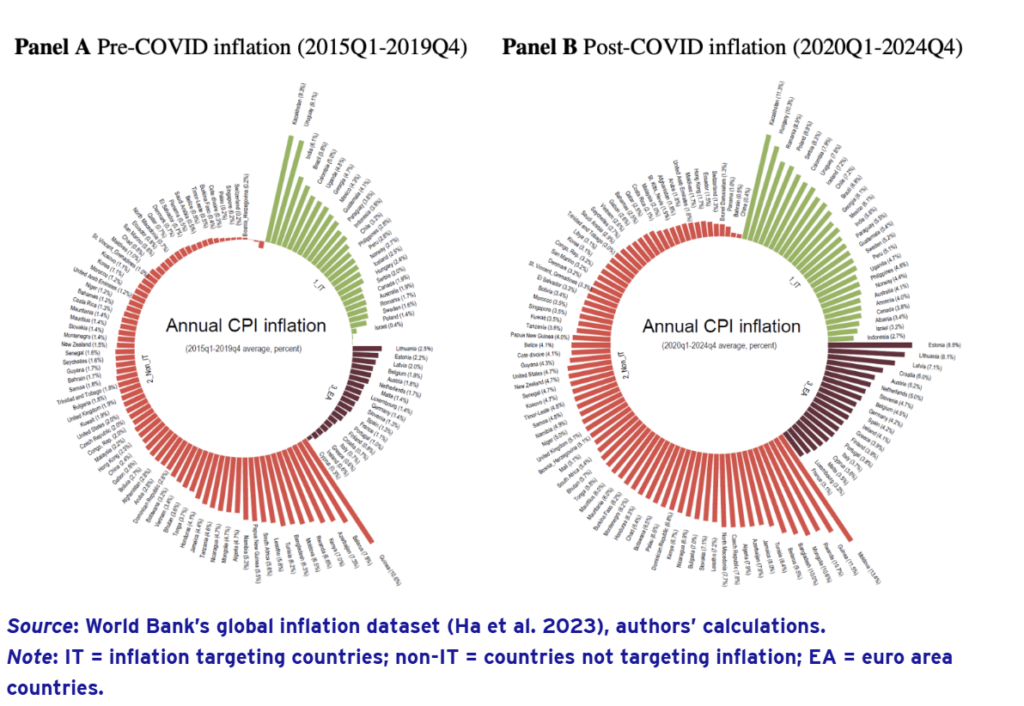

Yet beneath this apparent stabilisation lies a more uncomfortable reality. Inflation rates in many economies remain above the levels that prevailed before the pandemic, while price levels themselves have shifted permanently upward (see Figure 1). At the same time, repeated geopolitical tensions – most recently the conflict in the Middle East – energy fragmentation, climate-transition pressures, and industrial-policy competition continue to generate new supply disturbances.

Figure 1 Average annual CPI inflation: Pre- and post-COVID

Source: World Bank’s global inflation dataset (Ha et al. 2023), authors’ calculations.

Note: IT = inflation targeting countries; non-IT = countries not targeting inflation; EA = euro area countries.

The current policy debate is therefore changing. The question is no longer simply whether inflation has peaked. It is whether inflation can return to its pre-COVID behaviour or whether the global economy has entered a structurally more shock-prone environment with persistently higher inflation rates.

Recent discussions at many central banks increasingly revolve around this concern. Greene (2025) argues that central banks now operate in a world characterised by recurrent relative-price shocks and supply fragmentation rather than the unusually stable supply conditions of the Great Moderation. Powell (2024) similarly emphasises that supply-side disturbances have become more important drivers of inflation dynamics. Schnabel (2022) similarly argues that geopolitical fragmentation and the partial reversal of globalisation may expose central banks to larger and more persistent supply shocks than those prevailing during the Great Moderation.

The post-pandemic inflation episode offers an unusually revealing laboratory for studying this new world.

The inflation surge following COVID-19 was one of the most synchronised macroeconomic shocks in modern history. Virtually every economy confronted some combination of supply-chain disruptions, the sharp rebound in demand following reopening, labour shortages, commodity-price spikes, and then the energy and food shock following Russia’s invasion of Ukraine.

Yet inflation outcomes diverged enormously. Some economies experienced inflation that, while painful, remained relatively contained. Others saw inflation become deeply persistent, producing prolonged cost-of-living pressures and large cumulative increases in prices.

Why did similar global shocks generate such different inflation paths? A large literature has examined the origins of the inflation surge itself (Bernanke and Blanchard 2023, 2024). Much of that debate focused on the relative contributions of fiscal expansion, accommodative monetary policy, supply bottlenecks, and energy shocks. Those explanations matter. But they mainly explain why inflation rose globally. They do not explain why inflation persistence differed so dramatically across countries.

Our recent work (Imam and Poghosyan 2026) approaches the issue from a different angle. The crucial question was not simply the size of the shock. It was how economies absorbed and transmitted the shock once it arrived.

In economies with histories of higher inflation, firms and households appear to have interpreted the inflation surge differently (Gagnon and Kamin 2025). The distinction is important because inflation persistence increasingly appears linked not only to demand conditions, but also to the interaction between repeated supply shocks, expectations, wage formation, and energy-price transmission. In this sense, the post-pandemic inflation episode may mark less a temporary inflation spike than the return of supply-constrained macroeconomics (see also Imam and Poghosyan 2025).

One striking feature of the episode is that inflation rates eventually declined almost everywhere, yet they often stabilised above their pre-pandemic norms. Figure 2 shows that inflation did not fully revert to the low and stable patterns that characterised much of the 2000s and 2010s. Instead, post-pandemic inflation increasingly appears to behave less like a temporary ceiling and more like a new floor under inflation dynamics.

Figure 2 Distribution of CPI inflation

Source: World Bank’s global inflation dataset (Ha et al. 2023), authors’ calculations.

Note: Reported is the Epanechnikov kernel distribution. Outlier observations exceeding 20% in absolute terms are not included.

The political economy implications are significant. Households experience inflation not only through permanently higher price levels, but also through the fact that inflation rates themselves often stabilised above their pre-pandemic norms. Even after the initial shock faded, both prices and inflation rates remained persistently above the patterns households had become accustomed to during the Great Moderation. This matters because wage demands, savings decisions, and perceptions of economic stability are shaped not only by inflation spikes, but by the belief that inflation itself has become durably higher.

A central result of our paper is that two variables explain most of the cross-country divergence in post-pandemic inflation outcomes: countries’ prior inflation experience and the size of domestic energy-price shocks. Once these are taken into account, many institutional and macroeconomic variables commonly emphasised in policy debates lose explanatory power.

This does not imply institutions are irrelevant. Rather, it suggests that when shocks become sufficiently large and synchronised globally, institutions matter differently than they did during the Great Moderation.

The standard pre-pandemic framework often assumed that credible monetary regimes could largely prevent inflation from emerging. But large supply shocks cannot easily be neutralised by monetary policy alone. Central banks cannot produce natural gas, expand semiconductor production, or repair supply chains. What credibility appears to influence instead is the extent to which temporary shocks become embedded in wages, expectations, and broader pricing behaviour.

In other words, credibility matters less for preventing the initial shock than for containing the propagation mechanism afterwards. This becomes particularly visible when examining energy-price pass-through.

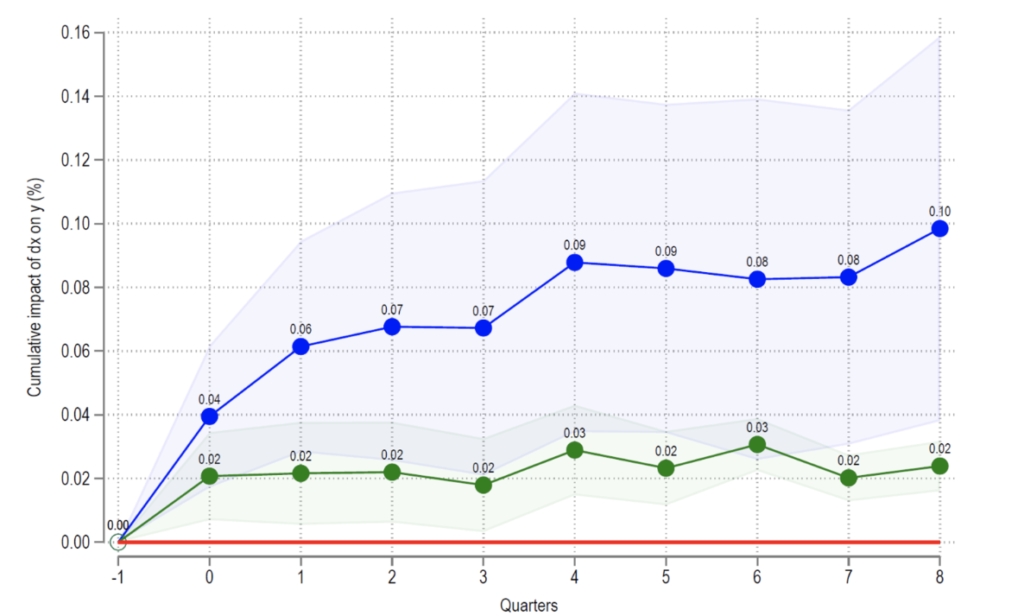

Using local projections for 70 advanced and emerging economies, we estimate how energy-price shocks transmitted into headline inflation before and after COVID. The results reveal a substantial structural shift: energy-price pass-through became materially stronger (see Figure 3) after the pandemic than during the pre-COVID decade.

Figure 3 Energy price pass-through: Pre- versus post-COVID period

Note: The figure shows the cumulative impact of a 1% change in energy prices on CPI inflation. The lines denote point estimates and the shaded area denotes the 95% confidence interval based on robust standard errors. Filled circles indicate significance. Blue line refers to post-COVID period, while green line refers to pre-COVID period.

The issue is not simply that the world experienced larger shocks after COVID. It is that economies themselves may have become more sensitive to shocks. During the Great Moderation, inflation behaved almost like a shock absorber: disturbances occurred, but the system dampened them relatively quickly. Globalisation, integrated production networks, stable energy markets, and relatively predictable geopolitics all helped prevent relative-price shocks from becoming generalised inflationary processes.

The post-pandemic environment appears fundamentally different. Energy fragmentation, geopolitical competition, industrial-policy rivalry, and supply insecurity now allow shocks to propagate more broadly and persistently through the economy. The shock absorbers themselves appear weaker.

The distinction between inflation-targeting and non-targeting economies reinforces this interpretation. Inflation-targeting countries experienced significantly lower energy-price pass-through than non-targeters, although pass-through remained positive even in highly credible regimes.

This nuance is important. Inflation targeting did not insulate economies from the shock. Rather, it moderated how strongly the shock propagated through the domestic economy.

One of the paper’s more unexpected findings concerns fossil-fuel subsidies (see Figure 4). Countries that temporarily expanded subsidies experienced materially weaker pass-through from energy prices to headline inflation. At first glance, this appears counterintuitive given the standard criticism that subsidies distort prices and weaken fiscal discipline.

Figure 4 Energy price pass-through: The role of fossil fuel subsidies

Note: The figure shows the cumulative impact of a 1% change in energy prices on CPI inflation. The lines denote point estimates and the shaded area denotes the 95% confidence interval based on robust standard errors. Filled circles indicate significance. Blue line refers to countries with relatively higher fossil fuel subsidies, while green line refers to countries with relatively lower fossil fuel subsidies as a share of GDP.

But the mechanism becomes clearer once energy is viewed not simply as a consumer good, but as a universal intermediate input. Energy enters transportation, logistics, manufacturing, food production, and services. Large energy shocks therefore diffuse through the entire price system. Once wage bargaining and backward-looking indexation begin responding to those price increases, inflation can become self-reinforcing. Temporary energy-price smoothing may therefore do more than mechanically reduce headline inflation. It may interrupt the transmission of shocks into wages when indexation is present, transportation costs, and broader price-setting behaviour.

This does not imply subsidies are costless or universally desirable. Persistent subsidies can undermine fiscal credibility, delay adjustment, and create inefficient energy use. Bernanke and Blanchard (2023) rightly emphasise that monetary and fiscal policy cannot permanently suppress relative-price adjustment. But the results suggest something more nuanced than the conventional debate often allows. Under sufficiently large supply shocks, temporary fiscal smoothing may reduce medium-term inflation persistence rather than merely postpone inflation.

The broader historical shift is striking. For much of the 2000s and 2010s, advanced economies became accustomed to a world in which globalisation, technological change, and integrated supply chains continuously dampened inflationary pressures. The dominant concern was secular stagnation and chronically insufficient inflation.

The post-pandemic episode challenged that framework abruptly. Perhaps the low-inflation decades before COVID were historically unusual rather than structurally permanent.

What may be emerging is not simply a more inflationary world, but a more shock-sensitive one, a world of repeated supply disturbances, geopolitical fragmentation, and structurally higher inflation volatility. In such an environment, the central challenge for macroeconomic policy may no longer be preventing inflation altogether, but preventing temporary shocks from becoming embedded in expectations, wages, and broader inflation dynamics. That represents a fundamentally different policy world from the one central banks confronted during the Great Moderation.

In the end, the post-pandemic inflation episode was not simply about who imported the shock. It was about which economies were able to prevent those shocks from becoming socially and institutionally embedded in domestic inflation dynamics.

Source : VOXeu

.jpg")

")

")

.jpeg")

")

")

")

")

")

")