")

Global food commodity markets entered 2026 on a relatively stable footing, supported by ample grain and edible oil supplies. However, escalating conflict in the Middle East has disrupted that stability, introducing new volatility into food trade and input markets. The World Bank Group’s April 2026 Commodity Markets Outlook projects a 2.5 percent increase in the global food commodity price index this year, but risks are firmly tilted to the upside. The emergence of El Niño conditions, rising energy and fertilizer costs, growing biofuel demand, and potential trade restrictions could all push food prices significantly above current projections.

Stronger or more prolonged El Niño than expected

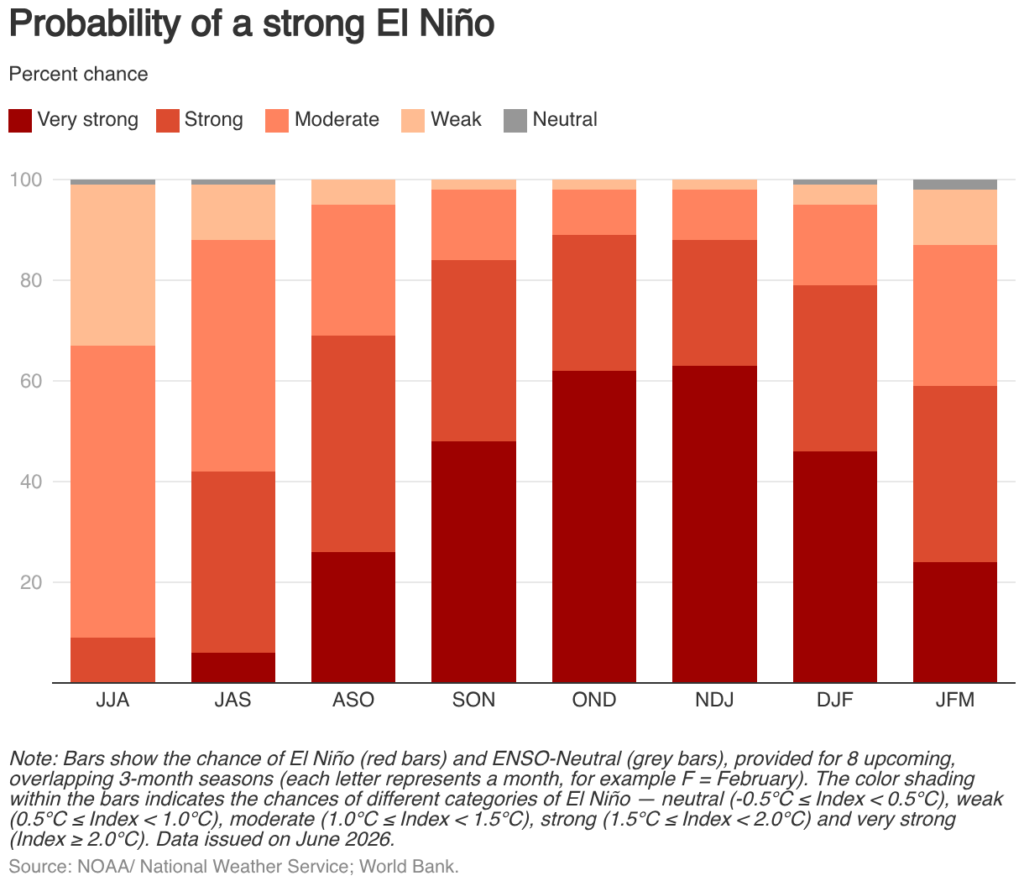

El Niño weather conditions have emerged and are expected to intensify to moderate or strong levels during the Northern Hemisphere fall, according to the U.S. National Oceanic and Atmospheric Administration. Forecasters estimate nearly a two-thirds probability that El Niño will reach a very strong intensity by November-December. For agricultural markets, the critical question is how strong El Niño becomes. Typically, El Niño brings prolonged drought to Southeast Asia and drier conditions across parts of Australia, northern Brazil, southern Africa, and South Asia—key producing regions for grains, sugarcane, and oilseeds. With agricultural markets already facing conflict-related cost pressures, a stronger or more persistent El Niño could disrupt multiple crop belts simultaneously and push food prices well above current projections.

Higher-than-expected input costs

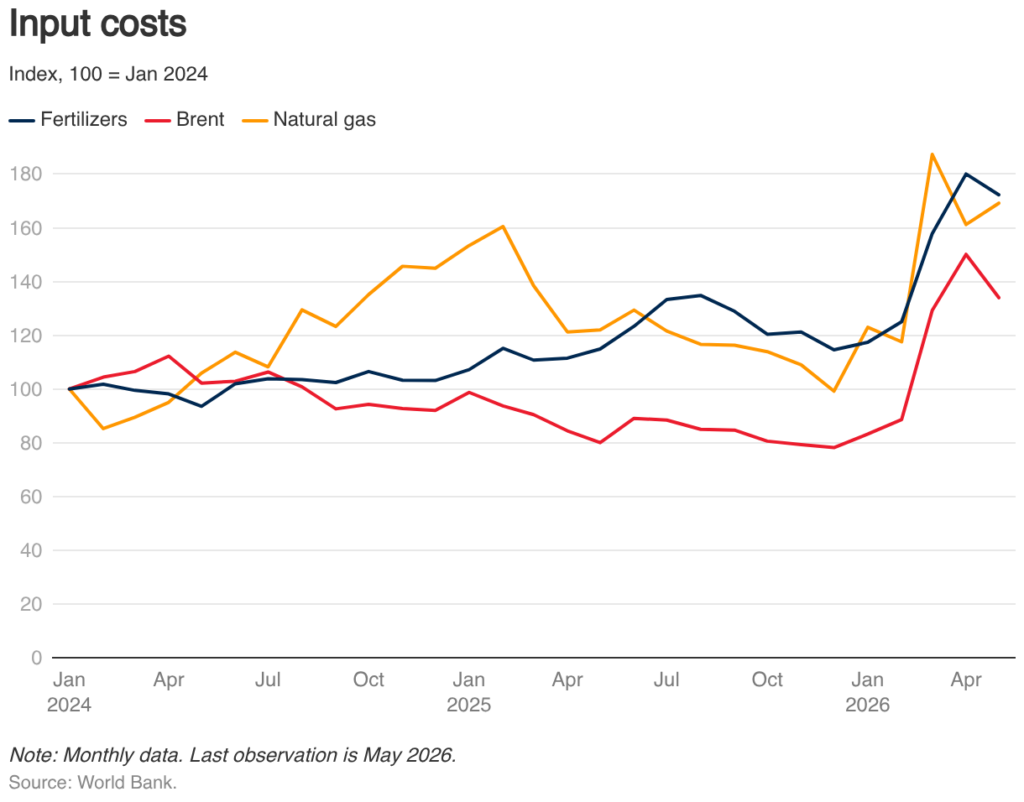

The closure of the Strait of Hormuz has disrupted global energy supplies, including fertilizers—especially urea and phosphate, two of the most widely used fertilizer products—and liquefied natural gas (LNG), pushing prices to their highest levels since 2022. Both are critical agricultural inputs: fertilizers directly, and natural gas as a key feedstock for nitrogen fertilizers. As a result, input prices have surged. The Commodity Markets Outlook baseline assumes that Middle East–related supply disruptions ease in the third quarter of 2026, limiting the severity and duration of supply constraints. The interim peace agreement between the United States and the Islamic Republic of Iran reported this week, which includes the reopening of the Strait of Hormuz, is broadly consistent with this assumption. However, if the disruptions persist, fertilizer and natural gas prices could rise far above current forecasts, creating significant upside risks to agricultural prices. In the near term, these risks typically manifest through higher production costs. Over the longer term, elevated fertilizer prices could lead farmers to use less fertilizer or shift toward crops that require less of it, lowering yields, tightening food supplies, and putting further upward pressure on prices.

Biofuel demand

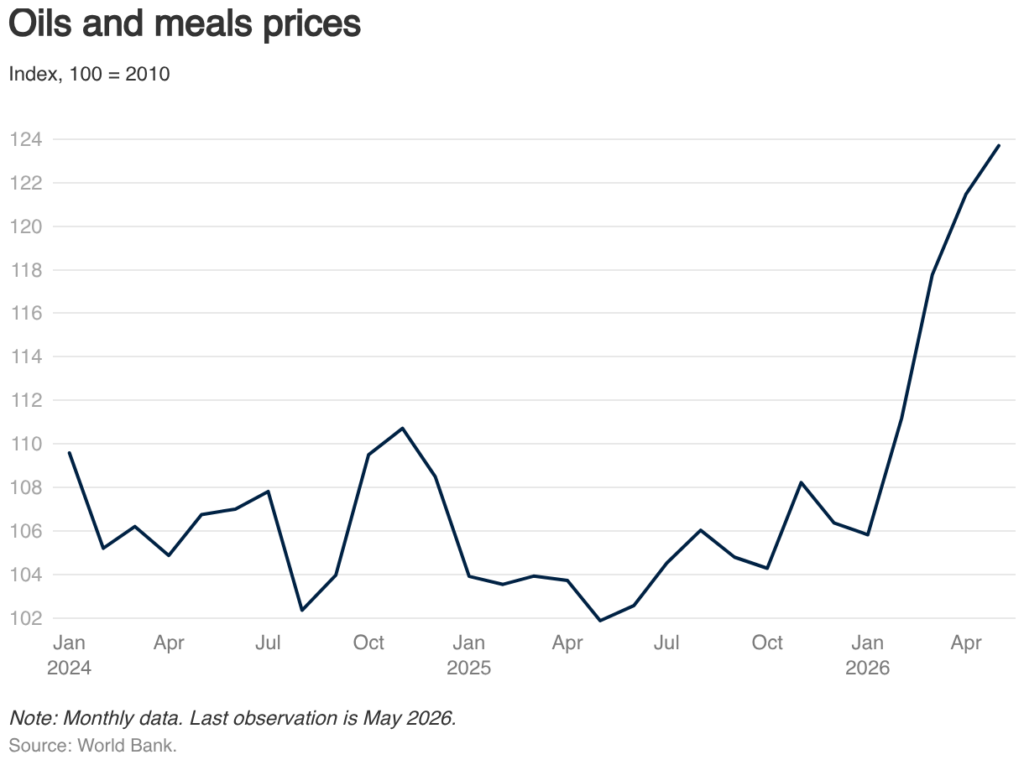

Higher crude oil prices have already increased the attractiveness of biofuels. This matters for food markets because the crops used to produce biofuels are the same ones that feed people, meaning higher energy prices can spill over into higher food prices. The World Bank Group’s oils and meals price index rose 11 percent in the three months since the conflict began, partly reflecting strong demand for biodiesel. Government policies are reinforcing this trend: several major economies have recently raised their blending mandates, which are rules requiring that a minimum share of biofuel be mixed into conventional fuel supplies. Indonesia is set to raise its mandatory biodiesel blend to 50 percent on July 1, Thailand has increased its blend from 5 percent to 7 percent, and the United States has raised the required volume of biomass-based diesel to 5.4 billion gallons in 2026 (from 3.4 billion in 2025) and 5.7 billion gallons in 2027. If high energy prices persist—or rise further should the conflict continue—prices of key biofuel feedstocks are likely to strengthen as well, particularly maize and sugar used for ethanol, and edible oils used for biodiesel. The impact could be felt most quickly in the sugar market, where mills, particularly in Brazil, can readily switch production between sugar and ethanol.

Export restrictions could amplify price swings

When food prices surge, governments often respond with export restrictions aimed at protecting domestic consumers. While these measures may provide short-term relief at home, they also constrain global supplies, heighten market volatility, and push international prices even higher. During the food price crises of 2008 and 2022, successive export bans on grains and edible oils amplified global price spikes and exacerbated food insecurity in import-dependent economies. With energy costs, fertilizer prices, and weather-related shocks all posing simultaneous risks, the threat of renewed trade restrictions is particularly acute. Low-income countries that rely heavily on food imports would be especially vulnerable.

The bottom line

Baseline projections point to only modest food price increases in 2026—an outcome that is relatively contained given the scale of the Middle East shock. Overall, however, risks are firmly tilted to the upside: a prolonged conflict, stronger biofuel demand, a more intense El Niño, or renewed export restrictions—alone or in combination—could push food commodity prices well above current projections, with the heaviest burden falling on the world’s most food-insecure populations.

Over the longer term, policy responses and biofuel demand could prove even more consequential. The recent conflict follows a series of disruptions that have reshaped commodity markets, including the COVID-19 pandemic, Russia’s invasion of Ukraine, and trade wars. Taken together, these shocks are likely to reinforce inward-looking policy shifts, with governments placing greater emphasis on energy and food self-sufficiency, strategic reserves, and supply security.

Source : World Bank

")

")

.jpeg")

")

")

")

")

")

")