The EU benefits greatly from its wide participation in international value chains. However, that integration is not exempt from strategic dependencies on products and inputs that are critical for Europe. This column examines the EU’s dependencies in traded goods using data from 5,400 products imported between 2017 and 2020. Foreign-dependent products span various sectors, including energy-intensive industries, health, renewables, and digital. China emerges as the primary source for these dependent products, followed by the US and Vietnam. Policymakers can use these insights to enhance supply chain resilience and mitigate vulnerabilities.

Over the past decades,the world has experienced unwavering changes in the shape of longer-term complex societal challenges: climate change, population ageing, and a massive digitisation of the economy and society. While some of those have brought about numerous opportunities, others have exerted pressures on Europe’s economy, industry, and society. An open-ended ‘permacrisis’ or ‘age of disorder’, anchored in relentless disruptions and high uncertainty, has added an additional layer of intricacy to the efforts in place to curb these challenges. The cumulative impacts of the COVID-19 pandemic, the Russian invasion of Ukraine, and the energy crisis have not only bolstered geopolitical frictions but also induced a deep redefinition of the architecture and dynamics of global supply chains.

While some of the societal costs associated with the refurbishment of global value chains were conceivably unavoidable, others resulted from well-known market failures. These occur when firms prioritise their individual interests, whether financial or otherwise, over broader societal concerns. For example, an overreliance on ring-fenced geographical areas for strategic inputs such as critical raw materials can induce a sub-optimal outcome from a societal point of view. Against this backdrop, policymakers around the globe have crafted new policy strategies to spur competitiveness and growth, while addressing the risks stemming from the poly-crisis. Many of those put a focus on uplifting economic and social resilience. In the EU, this materialised in a renewed industrial strategy with open strategic autonomy at its core. This new-fangled agenda marries openness to international trade with the creation of domestic capacity in strategic areas (European Commission 2021).

In this column, we present a methodology to measure the EU’s dependencies and vulnerabilities. Our approach tracks areas where such dependencies are prone to creating ex-ante risks of supply chain distress and, in doing so, our work complements recent studies (Attinasi et al. 2022, Baldwin 2022, Benoit et al. 2022, Inoue and Todo 2022, Martin et al. 2022, Lebastard et al. 2023, Schwellnus et al. 2023). We also aim at rounding out other studies that analysed global and national product vulnerabilities (Bonneau and Nakaa 2020, Di Comite and Pasimeni 2023, Jaravel and Mejean 2021, European Commission 2021, Reiter and Stehrer 2021, ECB 2023, Schwellnus et al. 2023).

The departure point of this column is 2021. In that year, the European Commission proposed a bottom-up, data-driven methodology to assess the EU’s product dependencies. In a recent paper (Arjona et al. 2023), we update this methodology by exploiting the novel FIGARO trade dataset by the European Commission that corrects for re-exports in international trade. Lack of treatment of re-exports is a drawback present in prevalent trade datasets that can lead to artificial shrinkages or upsurges in the number of dependent products.

A bottom-up, data-driven method to detect strategic dependencies

Our analysis sets its target on the universe of around 5,400 products imported by the EU from 2017 to 2020. We review and filter those products to identify a sub-set for which the EU experiences foreign dependencies. To be classified as foreign dependent with our method, a product must meet three criteria: first, the majority of non-EU imports of that product must come from fewer than three foreign countries; second, non-EU imports of the good in question must account for at least 50% of its total EU imports; and third, non-EU imports must exceed total EU exports. This is then complemented with an assessment of the relative rank of each of the traded goods on the three economic indicators that underpin each of the three criteria above, grouped in a single metric. We then select the top 10% of that distribution. In short, our methodology permits us to identify those goods which suffer from an excessive concentration on foreign sources, significant scarcity within the EU, and low possibilities for domestic substitution. We subsequently scan goods in sensitive areas such as security and safety, health, and the twin transitions.

Applying the methodology described above to the EU import data, we isolate 204 products as foreign-dependent, under four main blocks. First, dependent products are identified in energy-intensive industries. These are mostly raw materials used as inputs across many other industrial sectors. Some examples include manganese, nickel, aluminium, chromium, rare earth metals, molybdenum, borates, uranium, silicon, and permanent magnets. In addition, dependencies are identified for traditional energy inputs such as coal or petroleum coke and gases. Second, within the health industrial ecosystem, dependencies include heterocyclic compounds, alkaloids, medicines, vitamins, and medical instruments (e.g. scintigraphic apparatus, mechano-therapy or orthopaedic appliances). We also observe COVID-19-related goods where major supply chain distress was experienced at the onset of the pandemic, such as surgical gloves or protective garments. Third, within the renewables industrial ecosystem, dependencies are recognised in raw materials with heavy demand for the green transition, including photovoltaic cells or LED lamps. Fourth, on the digital front, we detect products such as laptops, mobile phones, monitors, and projectors.

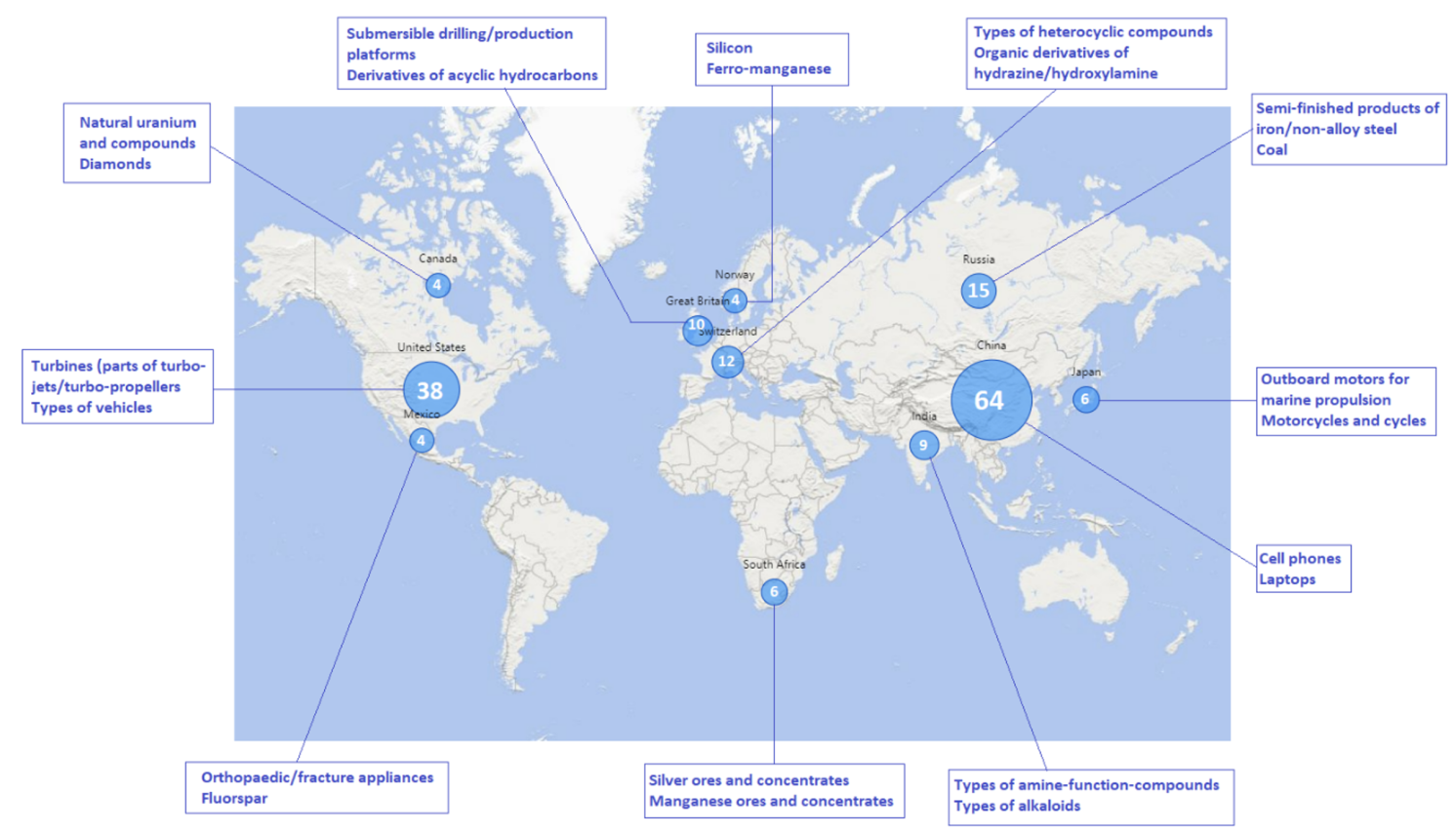

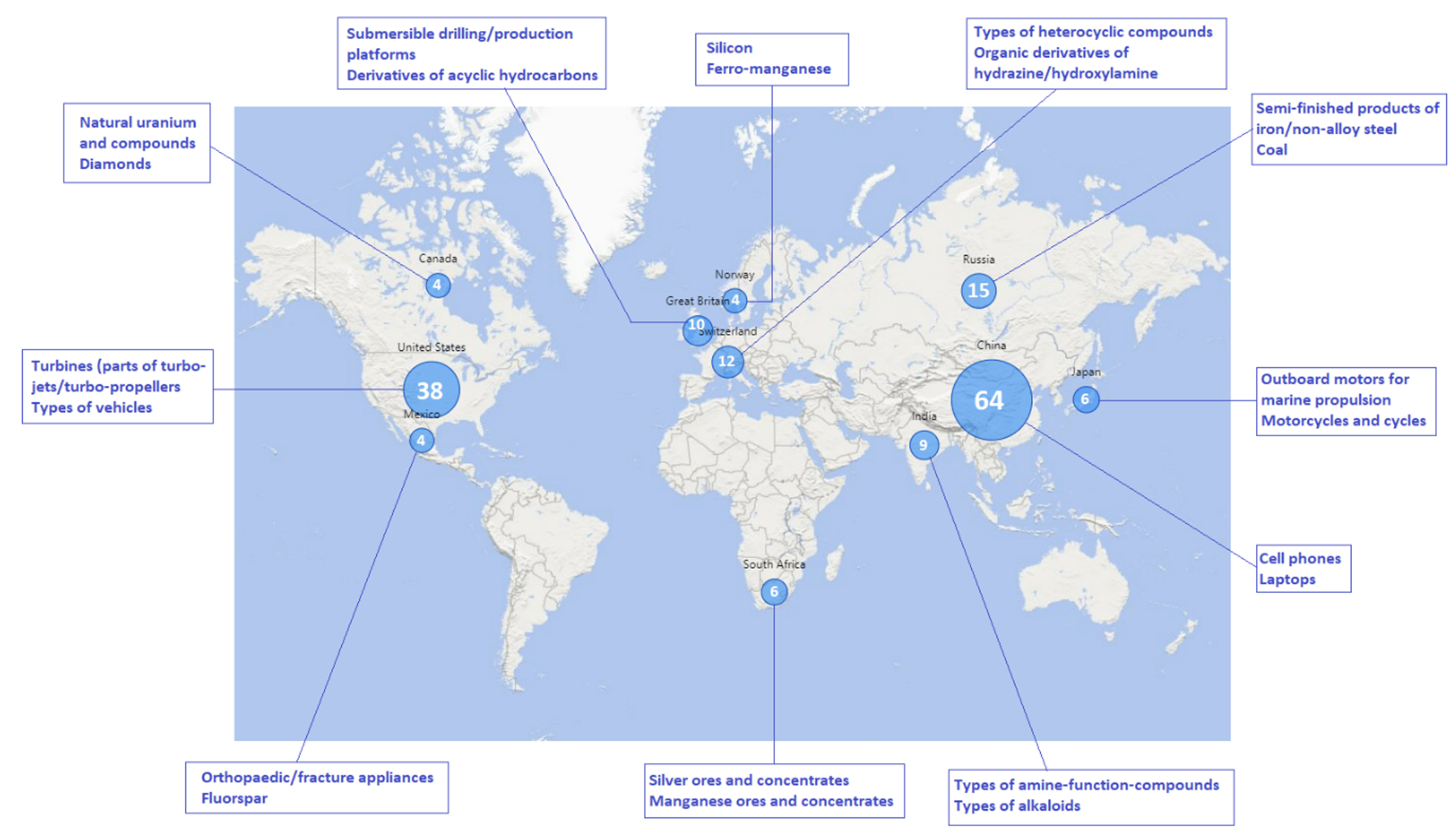

These 204 products where the EU experiences foreign dependencies represent around 9.2% of the total extra-EU import value. When it comes to origins, China represents more than half of this value, followed by the US and Vietnam with 9% and 7%, respectively. In the number of dependent products, China is the first source for 64 of them, followed by the US with 38 and Russia with 15 (see Figure 1). Examining the number of products rather than the value of imports is crucial since goods, despite facing low import values, may cause significant disruptions to society, as was the case with face masks during the COVID-19 pandemic.

Figure 1 Mapping the origins of 204 dependent products, including examples

Source: Authors’ computations based on the database – Trade-Figaro-Eurostat.

Risks of single points of failure

The list of EU dependencies in strategic ecosystems can be complemented with the main features of the global trade network associated with each of the 204 identified products. This allows us to detect goods whose production is highly concentrated at the world level and which can be considered highly vulnerable in case of supply chain distress. Our analysis argues that the relative risk of experiencing a global single point of failure (SPOF) for any of the 204 goods is higher when a single exporter is central to a large number of countries within a given trade network, and where world production is likely to be concentrated in a single country.

We calculate the risk of a global SPOF by comparing the relative position of each of the traded goods using the two metrics above. Products with the highest aggregate risk of an SPOF appear in decile 10 of the distribution of all 5,400 HS6 products. Products with the lowest risk of an SPOF locate in the lowest deciles. Once the relative position of each traded product is identified, we turn back to our identified list of 204 dependencies to inform policymakers when they develop mitigating actions to steer clear of such vulnerabilities. Out of the 204 EU-dependent products, close to 20% are in the highest decile and thus bear the highest risk of experiencing an SPOF, whereas only 6% are in the lowest risk category. Those products with the highest risk of an SPOF include goods in the health industrial ecosystem (antibiotics, vitamins, medical apparatus, and COVID-19 goods), digital (laptops and parts, radio-broadcast receivers, and mobile phones), and renewables (LED lights).

Conclusions

Our results imply that the risks associated with EU dependencies cannot be mitigated with a one-size-fits-all policy recipe. Improving our granular understanding of strategic dependencies and global SPOFs would allow, for example, us to differentiate between products where diversification through trade policy instruments is adequate from other products where risk mitigation may instead benefit from EU capacity building. More precisely, to address EU dependencies on products for which the associated risk of an SPOF is low, EU policies should be able to fully mobilise the power of trade policy instrumentation. On the other hand, if EU dependencies experience high risks of an SPOF, support for the creation and deployment of novel technologies, stronger R&D, circularity efforts, or stockpiling can appear as more appropriate solutions to support the building of internal EU capacity through industrial and innovation policies.

Against this backdrop, over recent years the EU has equipped itself with a set of policy measures to curb its strategic dependencies. In the case of raw materials, where EU dependencies are prominent, the recently adopted Critical Raw Materials Act (2023) has the goal of fostering the EU’s access to a secure, diversified, affordable, and sustainable supply of such materials, supporting a greater EU capacity for extraction, processing, and recycling. The European Chips Act (2022) and the Net-Zero Industry Act (2023) aim at accelerating the EU’s manufacturing capacity in chips and solar panels, respectively. These initiatives secure a central position for accurate and relevant monitoring tools capable of accurately measuring and disentangling strategic dependencies. Such tools should also be able to identify single points of failure within supply chains and thus provide early warning signals of potential supply chain disruptions.

")

")

.jpeg")

")

")

")

")

")

")