The 2022 Russian invasion of Ukraine severely disrupted European gas markets. Energy costs rose steeply, global natural gas flows were significantly reoriented, and policymakers’ focus shifted towards energy security. This column examines how the conflict has reshaped the natural gas market, with an emphasis on the role of liquefied natural gas. Europe has become a major importer of liquefied natural gas, crowding out imports to Latin America and Asia. Its gas market is becoming more integrated and global. Nonetheless, the outlook for the natural gas market remains subject to high uncertainty.

The Russian invasion of Ukraine constituted a significant breach of the global geopolitical order and of national sovereignty, with profound economic consequences that extend well beyond the direct effect of the war. These include, among others, a marked deterioration of the world macroeconomic outlook (Garicano et al. 2022, Albrizio et al. 2022, Alessandri and Gazzani 2023), disruptions in trade (World Bank 2022), and strong shockwaves across financial and commodity markets (Ferriani and Gazzani 2022, Boungou and Yatié 2022).

In a recent study (Emiliozzi et al. 2023), we focus on the impact of the war on energy commodity markets, and in particular on the reshaping of global energy flows, with a specific emphasis on the changes in the natural gas market. Up until 2021, Russia was the primary European provider of both natural gas and crude oil imports, accounting for 44% and 28% of the total extra-EU imports, respectively. Since the autumn of 2021, Russia’s weaponisation of its natural gas exports in response to the standoff on the Nord-Stream II pipeline approval contributed to a steady increase in natural gas prices. This trend deteriorated after the start of the conflict, with piped gas from Russia progressively diminishing throughout 2022 and causing widespread disruptions in energy markets. The conflict affected Europe first and foremost, although it produced global reverberations and sparked a worldwide reconfiguration of energy commodity flows for both natural gas and oil (Babina et al. 2023).

In this context, liquefied natural gas (LNG) emerged as a significant new player in the natural gas market, providing a critical contribution to ensure Europe’s energy security. LNG replaced a substantial portion of Russian pipeline exports to Europe, fundamentally changing the structure of the European gas market from regional and segmented into one that is more integrated and global.

The global reshuffle in LNG flows

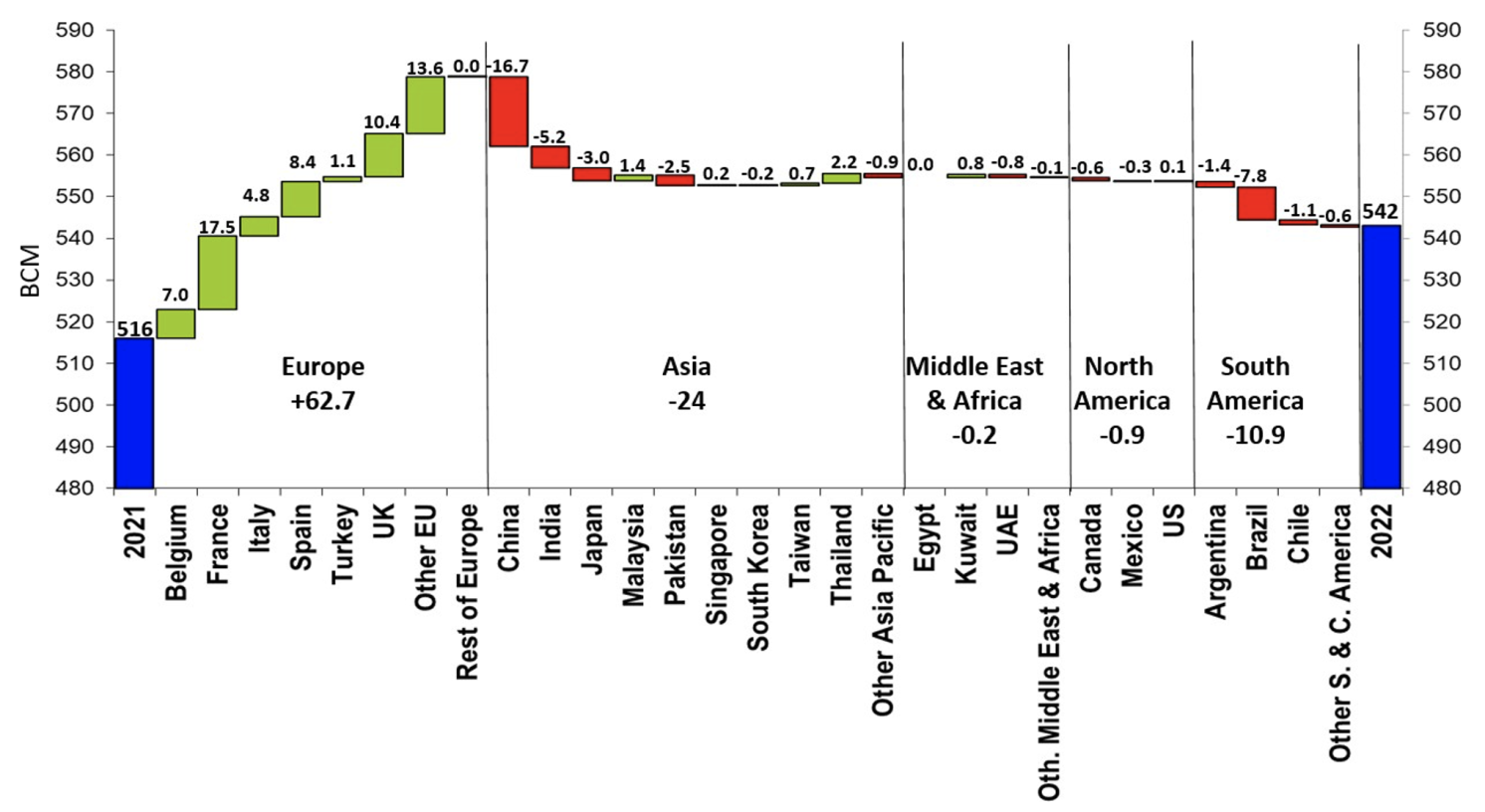

Historically, European countries mainly relied on piped gas to satisfy their gas consumption needs and absorbed excess supply at convenient prices from the global LNG market, whose main traditional importers had been Asian countries (China, Japan, South Korea). Since mid-2021, Europe had to draw significant amounts from the LNG market to compensate the foregone Russian imports and started to act as a major LNG importer worldwide (Figure 1). In 2022 European LNG imports surged by almost 60% on a yearly basis and, notably, the share of LNG over total European supply soared to 53% from an average of 20% between 2000 and 2019.

Figure 1 LNG imports by world region and major importer nation

Notes: CIS stands for Commonwealth of Independent States; BCM stands for billions of cubic metres.

Source: Energy Institute (2023).

To bolster this upward trend, European countries made substantial investments to expand their regasification infrastructure so they may further exploit the potential of the LNG market in the future. Notably, Germany, which had no LNG terminal until the end of 2022, has outlined plans to install several facilities. However, due to constraints on the expansion of the LNG supply in the short term, Europe’s rise as a LNG importer also crowded out imports in other regions such as Latin America (-11 billion cubic metres in 2022 with reference to 2021) and Asia (-24 billion cubic metres). 1 The countries most affected have been emerging and developing economies that could not compete with Europe for LNG cargoes due to skyrocketing gas prices.

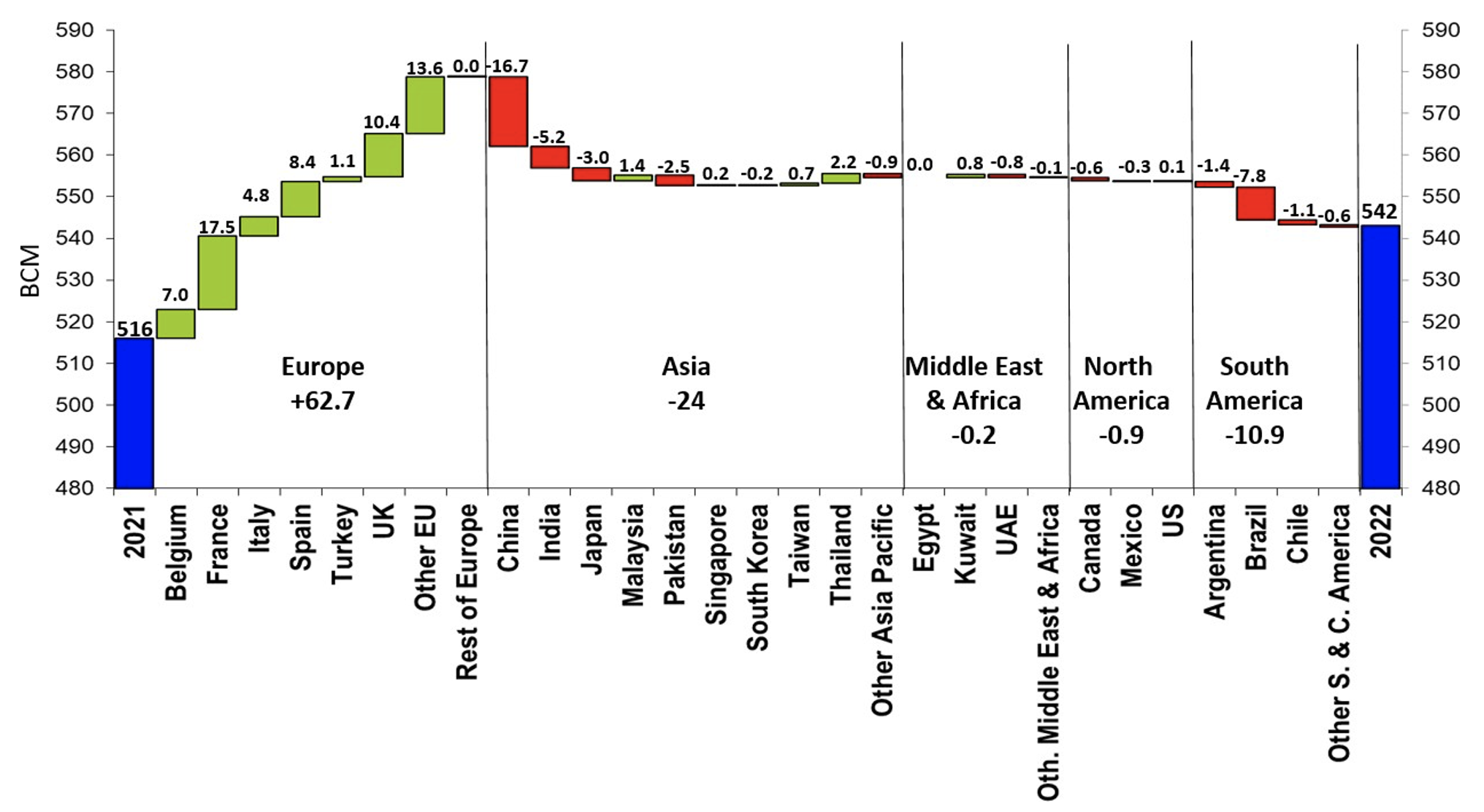

For both geographical reasons (LNG transportation is costly) and contractual (the US mainly relies on spot trades, in contrast to the other two major LNG producers – Australia and Qatar), the US emerged as the primary supplier of Europe in this novel configuration of the global gas market (Figure 2). While total US LNG exports expanded by 10% due to supply constraints (see above), flows towards Europe more than doubled (+140%) in 2022 on a yearly basis. Conversely, US exports to Asia halved and those to Latin America fell by about 70%. The drop in these LNG flows was only partially compensated by the mildly increased imports to Asia and Latin America from Qatar and Australia.

Figure 2 LNG exports by world region, 2021–2022 variation

Source: Energy Institute (2023).

The global LNG supply market is poised to increase significantly in 2025, benefiting from several LNG facilities coming online in the US. Consequently, the LNG market balances are expected to soften with benefits for the European economies in terms of energy security and procurement costs.

The European policy response to the crisis

Since the start of the Ukraine conflict, a strong policy response was put in place to counter the effects of the energy crisis. Adopted policy measures can be divided into two main categories: (i) structural measures that address natural gas consumption, supply, and storage, and (ii) fiscal relief measures primarily intended to support firms and households affected by surging gas and energy prices.

In terms of structural measures, in March 2022, the EU heads of state issued the Versailles Declaration, outlining the pillars of the EU’s response to the energy crisis. These pillars were later incorporated in the EU Commission’s REPowerEU plan (May 2022), the central policy framework for the EU’s energy strategy. The plan aims to rapidly reduce the dependence on Russian fossil fuels and guarantee the long-term sustainability and stability of the EU energy system. The plan’s principles were implemented through regulatory interventions that set storage capacity targets, introduced gas consumption reductions, and established a joint gas-purchasing facility and a correction mechanism to curb gas prices. Moreover, EU countries enhanced their LNG capacities and expanded import terminals, trying to diversify natural gas suppliers and forming partnerships with non-Russian counterparts to boost LNG and piped gas imports.

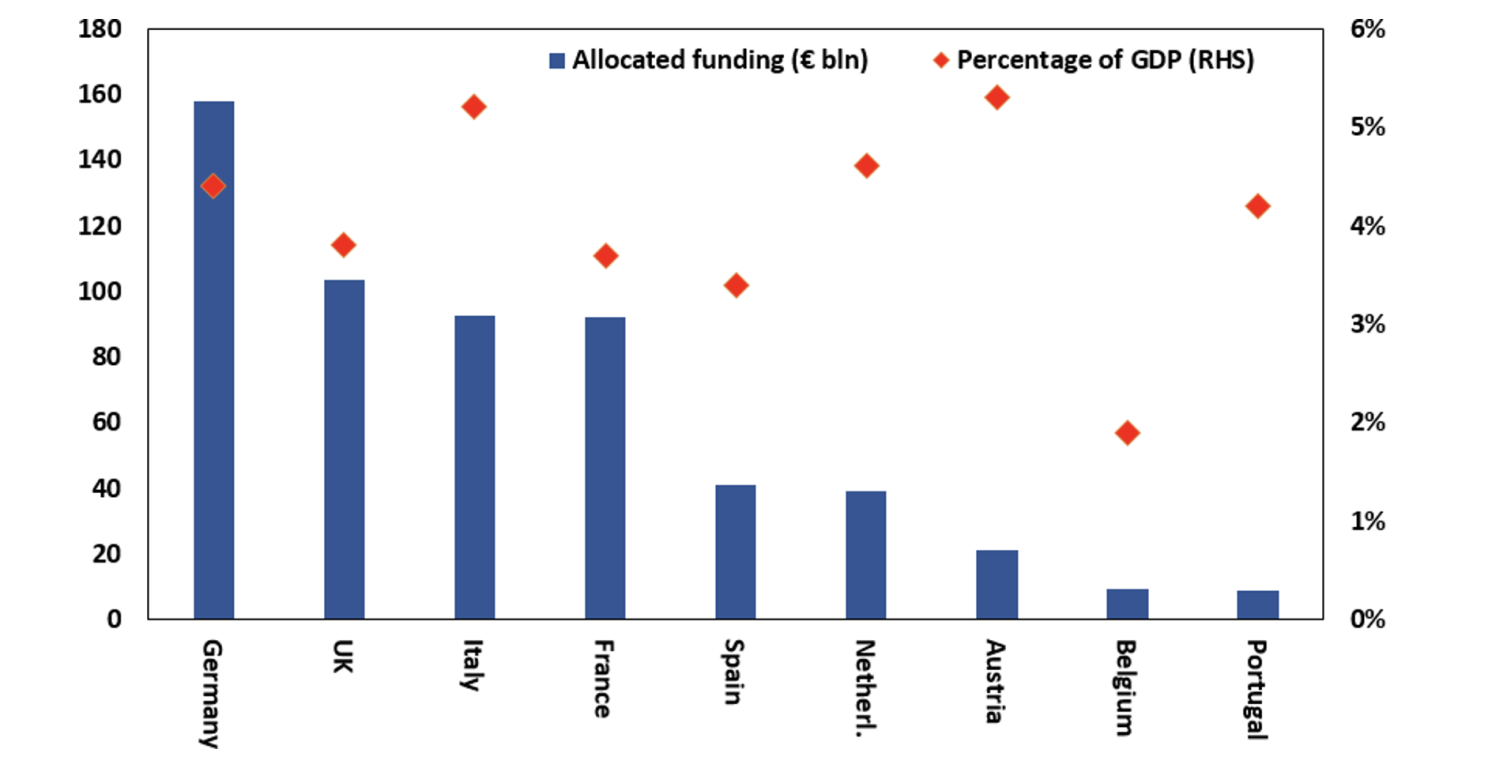

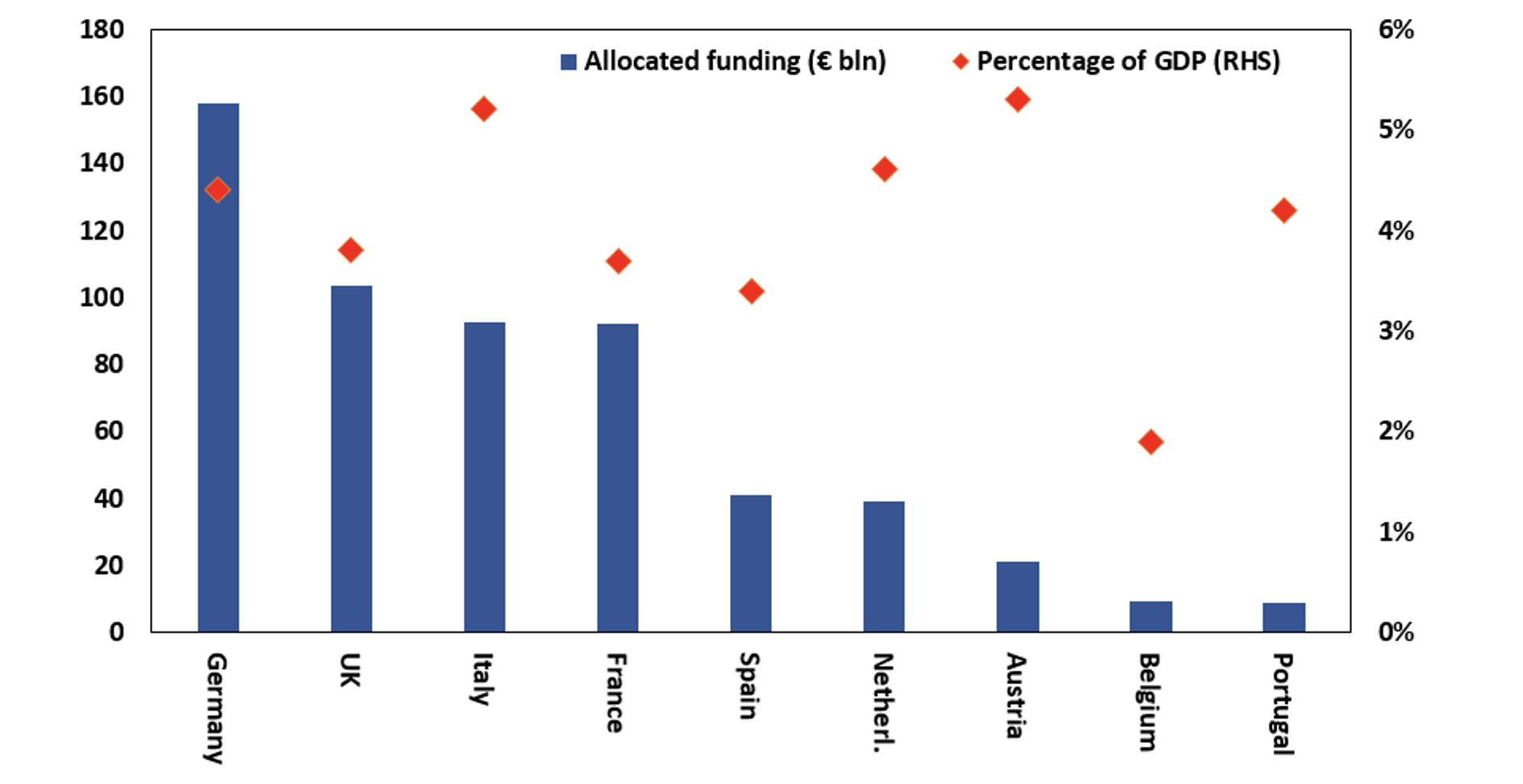

To mitigate the effects of energy prices on both households and firms, EU governments also adopted several fiscal support measures in the form of energy tax abatements, energy price ceilings, and fiscal transfers to vulnerable parts of the population. These measures inevitably burdened governments’ finances: European countries allocated over €650 billion between September 2021 and January 2023 to address the impact of the energy crisis. The lion’s share of this sum was put in by Germany, which adopted fiscal measures for around €158 billion, while Italy and France allocated approximately €90 billion each (Figure 3).

Figure 3 Government response to the energy crisis among selected European countries, September 2021 to January 2023

Source: Sgaravatti et al. (2023).

At the euro-area level, fiscal interventions for 2022 amounted to roughly 2% of the bloc’s GDP (Checherita-Westphal and Dorrucci 2023). Yet, the application of several national measures in an untargeted manner raised concerns about the absence of a coordinated EU energy policy, which could potentially exacerbate competitive challenges in the EU and undermine the EU single market (Ferriani and Gazzani 2023, Bialek et al. 2023).

Source : VOXeu

")

")

.jpeg")

")

")

")

")

")

")