Recent research has shown that the stance of monetary policy can influence financial stability. This column provides an explanation for the effects of monetary policy on credit growth based on a ‘credit creation theory of banking’. In this framework, ‘funds’ are liquid bank deposits created by the banking system independently of private saving(s). The central bank policy rate has a direct effect on credit supply by influencing the refinancing costs of banks. This provides a clear mechanism through which central banks can influence bank lending and financial stability.

A recent study by Grimm et al. (2023: 34) “provides the first evidence that the stance of monetary policy has implications for the stability of the financial system. A loose stance over an extended period of time leads to increased financial fragility several years down the line”. However, the paper says relatively little about the theoretical transmission mechanisms from low policy rates to financial instability: “Why, though, do money and credit expand in the first place? By analyzing this question, we contribute to the strand of the literature that focuses on potential causes of credit booms. To the best of our knowledge, this strand is relatively thin.”

An interesting new explanation of the link between the central bank’s policy and credit growth is provided in recent paper by Kashyap and Stein (2023). The authors argue: “(…) it now appears clear that both conventional and unconventional monetary policy actions gain much of their traction over the real economy by influencing a range of risk premiums in financial markets, where the risk premium on an asset is the expected return that an investor can expect to earn above and beyond the safe rate on a government bond of comparable maturity” (p.55). However, this transmission channel focuses mainly on non-banks and on money market funds. As far as banks are concerned, it neglects the effects of the central bank policy rate on the liability side of bank balance sheets which can compensate the negative effects of lower interest rates on the accounting income of banks.

In a recent paper, we provide an alternative and more direct theoretical explanation for the effect of central bank policy rates on credit growth. Our model differs from standard models in that it is not based on the ‘financial intermediation theory of banking’, but on the ‘credit creation theory of banking’ (Werner 2014). The main differences between the two approaches can be illustrated by comparing the standard loanable funds model with a model of the market for bank loans.

In the loanable funds model, ‘funds’ are an all-purpose commodity that can be used interchangeably as a consumption good, as an investment good, and as ‘capital’ or ‘saving(s)’ that banks intermediate from savers to investors. Households supply the good on the ‘capital market’, where there is demand from investors who use it to increase the capital stock. Thus, deposits drive loans. In this setup, the role of banks is limited to the intermediation funds, as they cannot produce or consume the all-purpose commodity. The same applies to the central bank, which therefore has no role to play in this model.

With the loanable funds model still the dominant paradigm in monetary macroeconomics, it is not surprising that Mian and Sufi (2018: 50), for example, are puzzled by the dynamics of private credit growth:

“Much of the work on the credit-driven household demand channel takes the expansion of credit supply as a given. But what kind of shock leads to credit supply expansion? We should admit that we have now entered a more speculative part of this essay”.

Indeed, with household saving as the sole source of funds, the strong credit growth preceding financial crises is difficult to explain. This reflects the fundamental flaw in the model, namely that the monetary sphere is identical to the real sphere. In fact, only two decisions can be made: (1) the saving decision, which is identical with the consumption decision; and (2) the investment decision. How can one expect to explain the mechanics of the financial system with consumption and investment?

This is different in our model of bank lending: the monetary sphere is not constrained by the real sphere, since ‘funds’ are liquid bank deposits. They are created by the banking system ex nihilo, i.e. completely independently of private saving. The mechanics of this approach have been explained in detail by the Bank of England (McLeay et al. 2014) and the Deutsche Bundesbank (2017). The logic is quite simple: by lending to a customer, the bank credits his/her deposit account. Thus, the very act of lending creates deposits (i.e. money).

In this model, the central bank can directly influence the supply of credit by banks. This is because of the secondary effects of bank credit creation. In most cases, borrowers use their new deposits to make payments to another bank. For the bank that made the loan, this means a reduction in its reserves at the central bank. Assuming that it had an optimal level of reserves before the loan, the bank needs to replenish its deposits with the central bank. This can be done by borrowing from other banks on the money market or directly from the central bank. In the case of an interbank loan the interest rate on this borrowing is close to the central bank’s policy rate. In the case of central bank refinancing it is equal to the policy rate.

In addition to the central bank’s policy rate, in our model the supply of bank loans depends on the banks’ assessment of risk and the overall economic situation, represented by the output gap. Thus, in the model of the market for bank loans, the central bank’s policy rate is a key determinant of the cost of bank loans.

On the demand side, our monetary model is not restricted to demand for investment loans that increase the capital stock. It can also be related to the purchase of existing assets, particularly real estate. We assume that the demand for loans depends negatively on the interest rate on bank loans and positively on the level of economic activity.

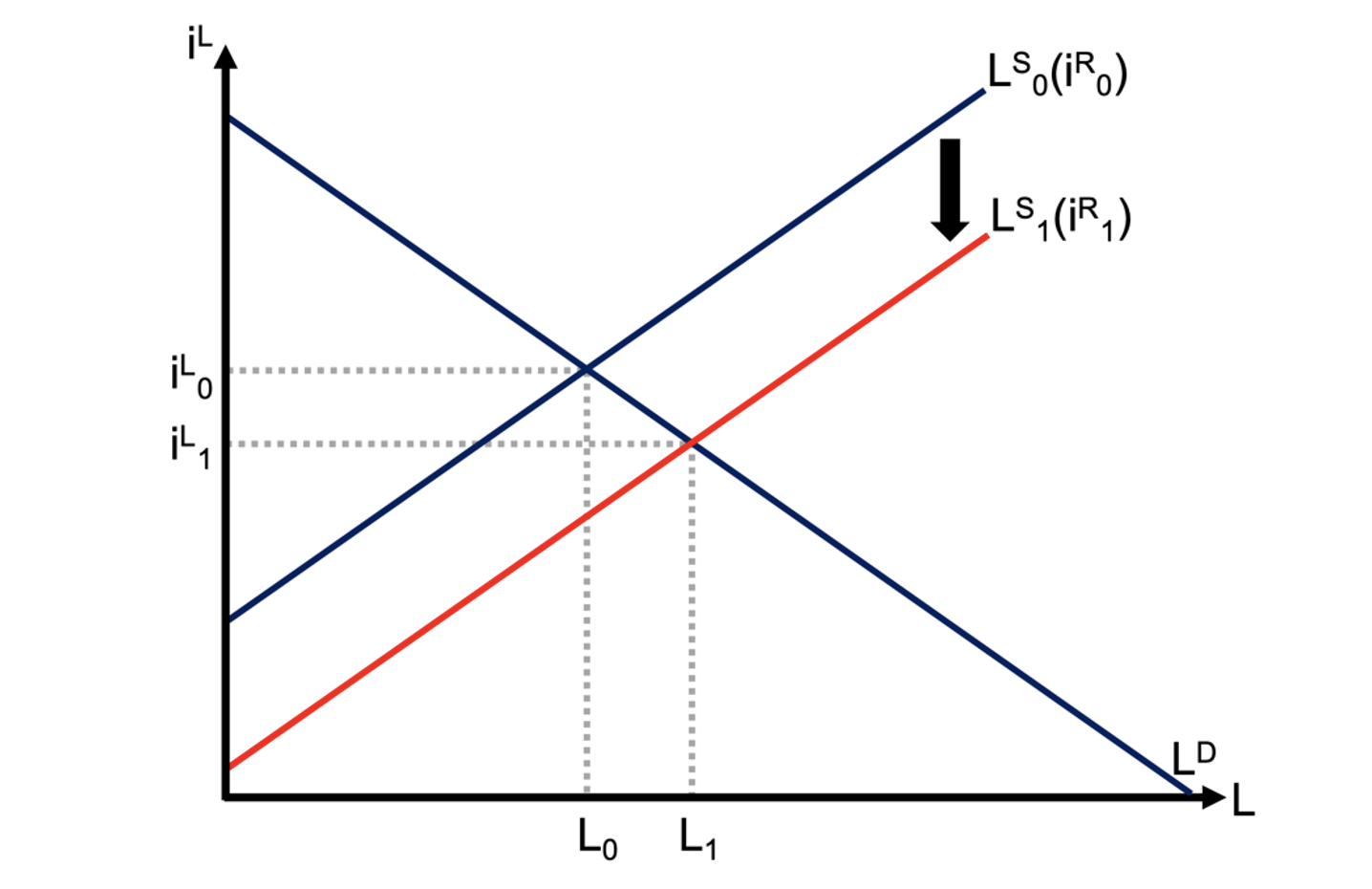

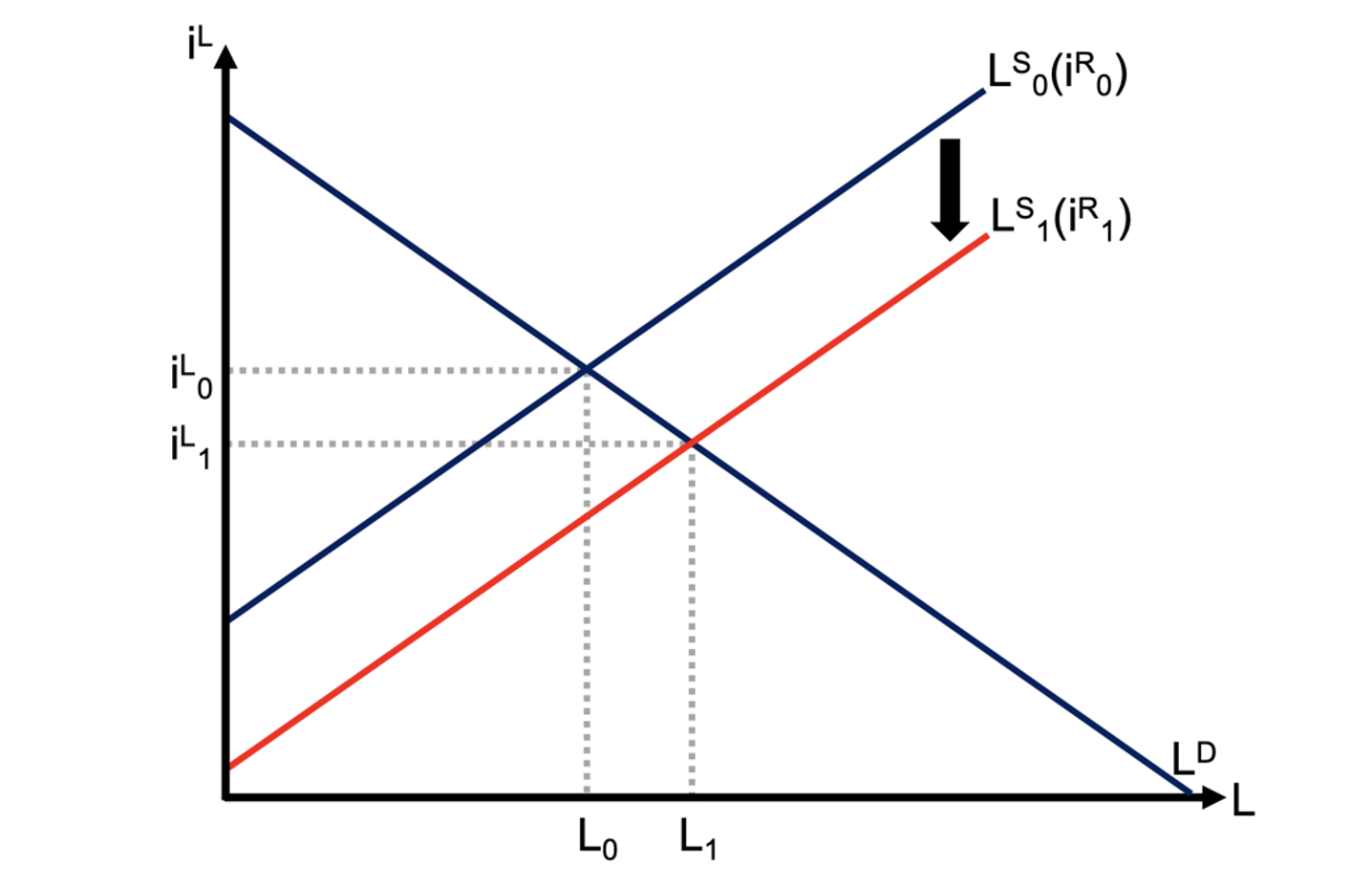

The impact of the central bank policy rate on the amount of credit in the economy can be easily described in the model. If the central bank lowers the policy rate (iR) from, for example in order to stimulate the economy, the supply of bank loans (LS) shifts downwards along the demand curve (LD) due to the reduced refinancing costs of banks. This lowers the loan interest rates (iL) and increases the equilibrium amount of loans (L) in the economy (Figure 1):

Figure 1 Change in policy rate in bank loan market

The model differs from the textbook multiplier which underlies the bank lending channel in that it assumes reverse causality. The textbook multiplier is rightly criticised for assuming that an increase in monetary base causes a higher amount of bank loans and money (Carpenter and Demiralp 2012). In our model, the amount of bank loans is determined in the market for bank loans for a given central bank policy rate. The multiplier translates the amount of bank loans into the required monetary base. For a given multiplier, this implies that the central bank must passively supply the required amount of monetary base.

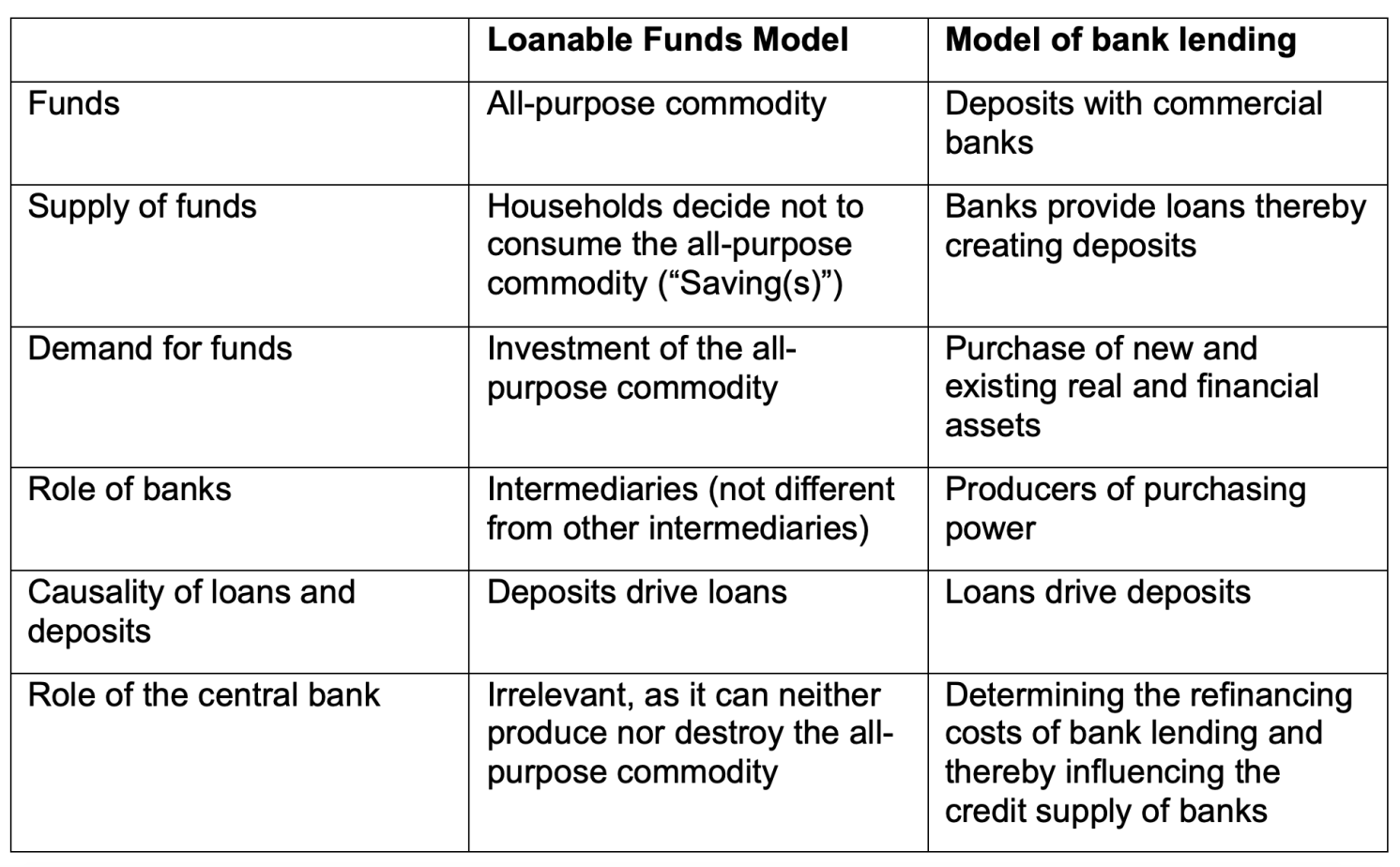

To sum up, it is not surprising that models that are essentially based on the loanable funds model, in which the role of banks is limited to the intermediation of funds created by savers, have difficulty in explaining the effects of the central bank’s policy rate on bank lending and financial stability. This is different in a monetary model with banks as ‘producer of purchasing power’ (Schumpeter 1934), 4 where the central bank’s policy rate plays an important role in the supply of bank credit. Table 1 summarises the fundamental differences between the two alternative approaches.

Table 1 Loanable funds model versus a monetary model of bank lending

Source : VOXEu

")

")

.jpeg")

")

")

")

")

")

")