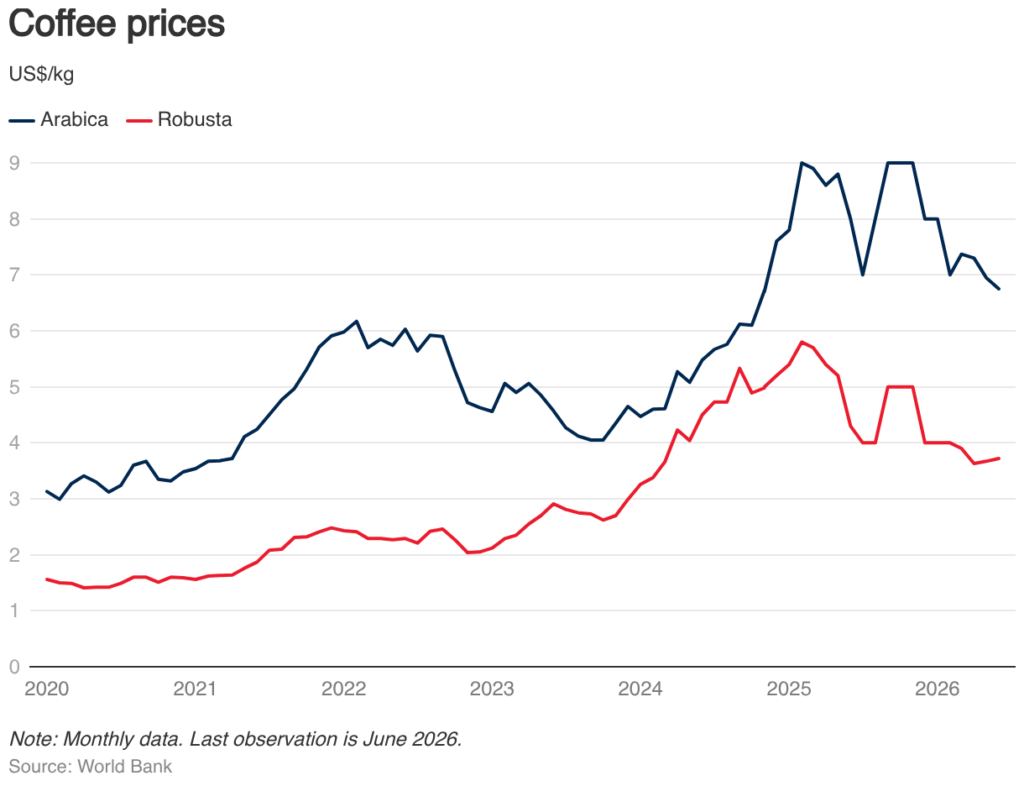

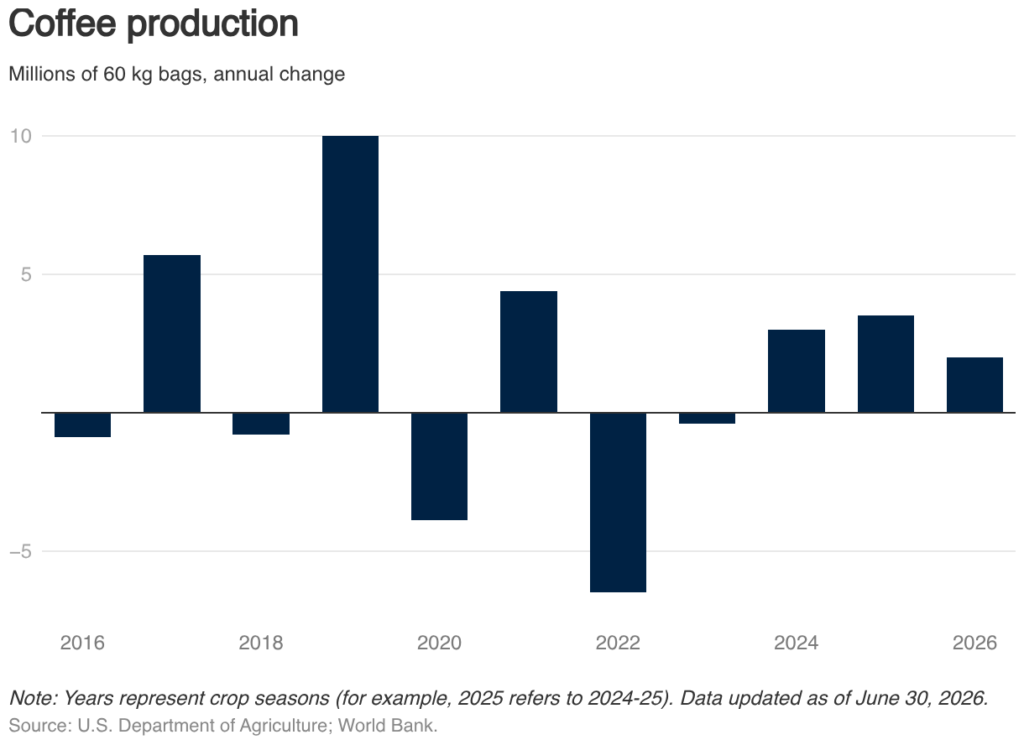

Coffee prices continued to ease in 2026Q2, helped by stronger global supply prospects and the removal of U.S. tariffs on Brazilian imports earlier in the year. Arabica prices slipped nearly 7 percent (q/q)—now sitting 17 percent below their level a year ago. Robusta prices fell even faster, dropping 9 percent in the quarter and landing 25 percent lower than a year earlier. Global production is also on the upswing, projected at 177.5 million bags during the 2025–26 season, a nearly 2 percent increase from the previous season and the third straight year of growth. With supply recovering, the price outlook points to further softening: Arabica, after soaring more than 40 percent in 2025, is expected to fall 14 percent in 2026 and ease again in 2027. Robusta is projected to decline 18 percent in 2026, followed by a smaller 3 percent dip in 2027. Still, the forecast is subject to considerable risks. Persistent heavy rains in Brazil—source of more than one‑third of the world’s coffee—could trigger disease outbreaks, while a stronger‑than‑expected El Niño could disrupt production and tighten markets again.

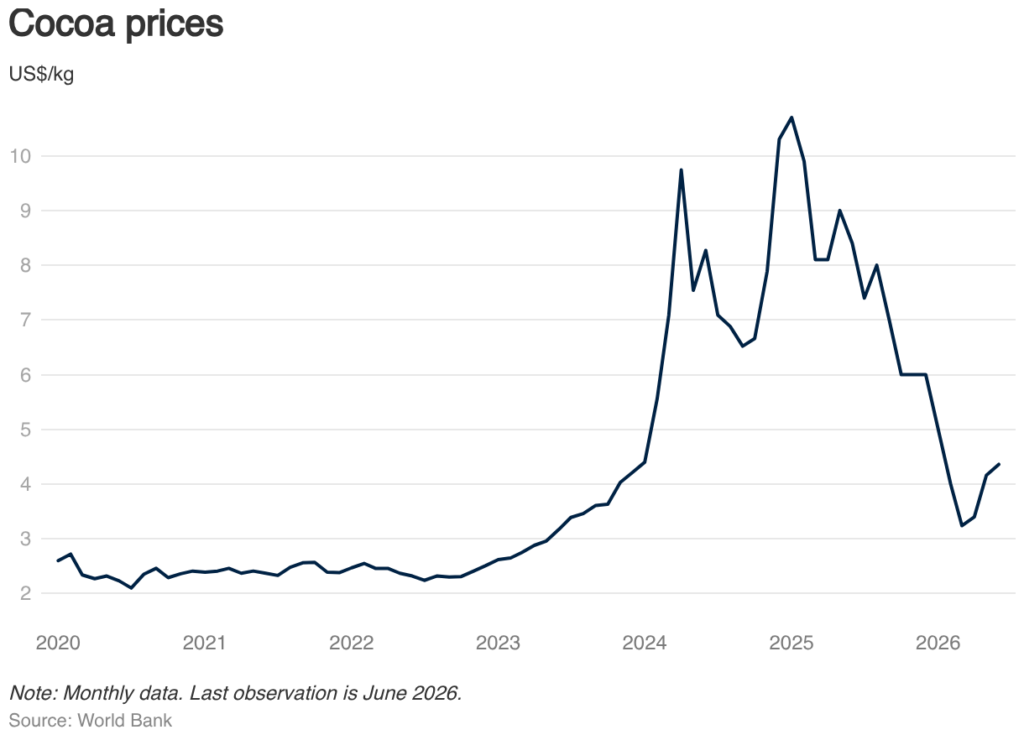

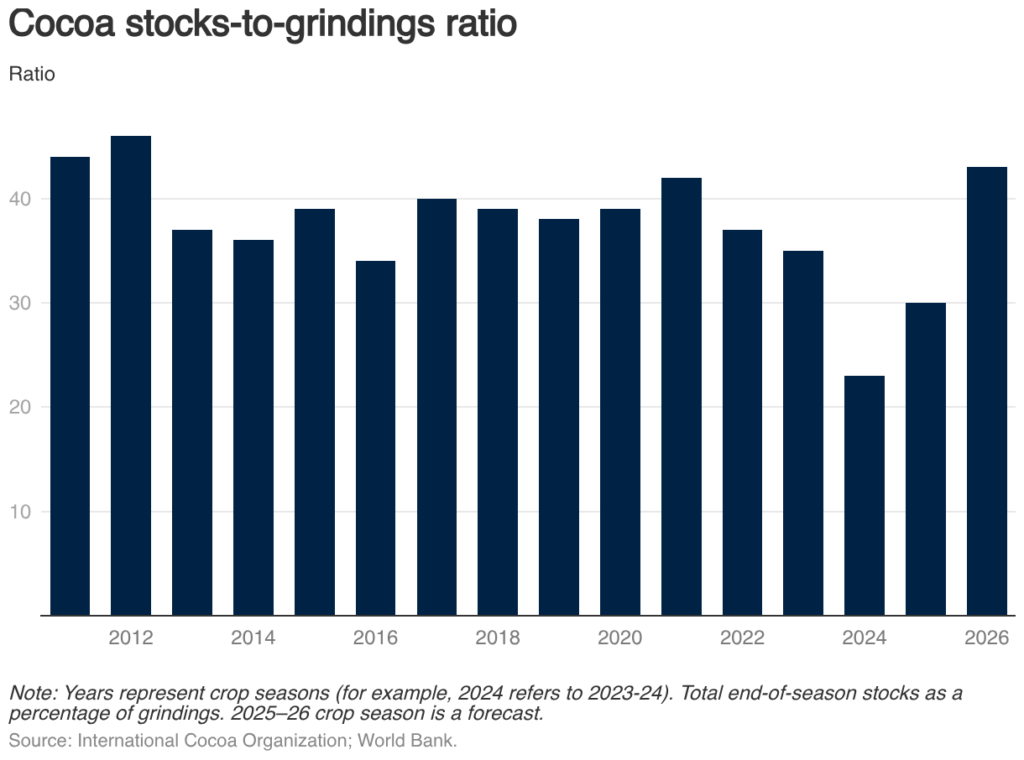

Cocoa prices have inched higher over the past three months, averaging $4.35/kg in June, but they are still more than 50 percent lower than a year ago. The steep drop from the early‑2025 peak reflects a sharp improvement in supply for the 2025–26 season, along with softer demand. Favorable weather in West Africa—especially Côte d’Ivoire and Ghana, which together produce about 60 percent of the world’s cocoa—has fueled a strong production rebound. Output this season is estimated to be more than one‑third higher than last year, pushing the global stocks‑to‑grindings ratio to 43 percent, slightly above its long‑term average of 41 percent. With supplies recovering, prices are expected to plunge more than 50 percent in 2026 before stabilizing in 2027 as markets rebalance. Still, the outlook remains weather‑sensitive. A stronger‑than‑expected El Niño could disrupt the recovery and tighten supplies again.

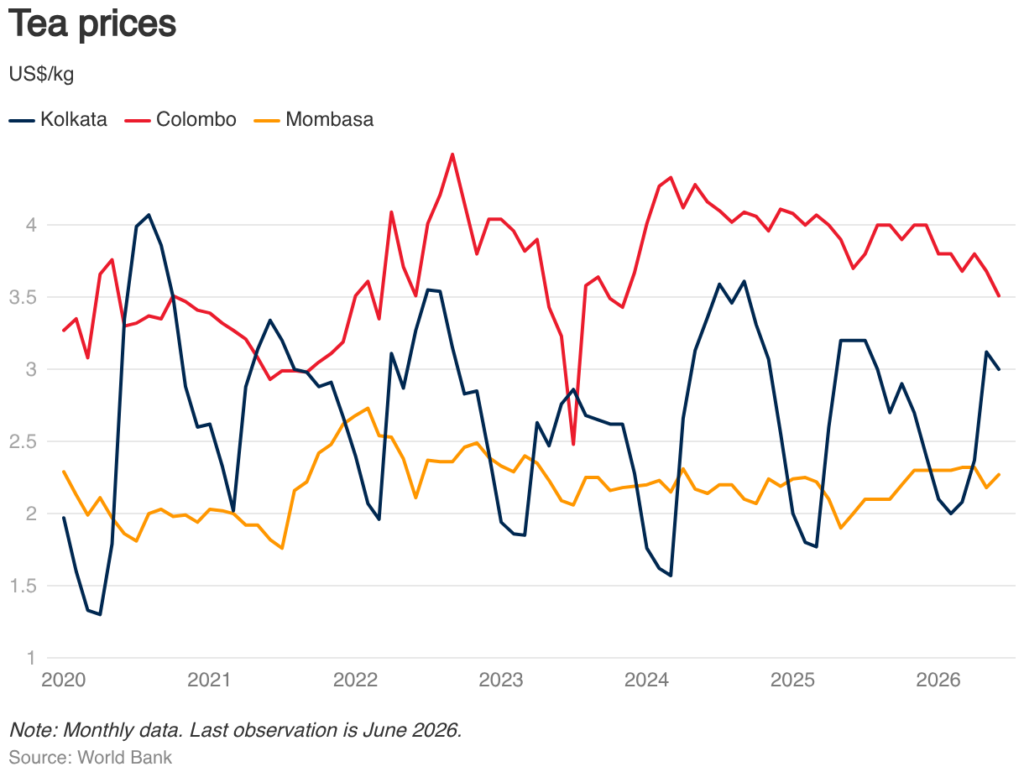

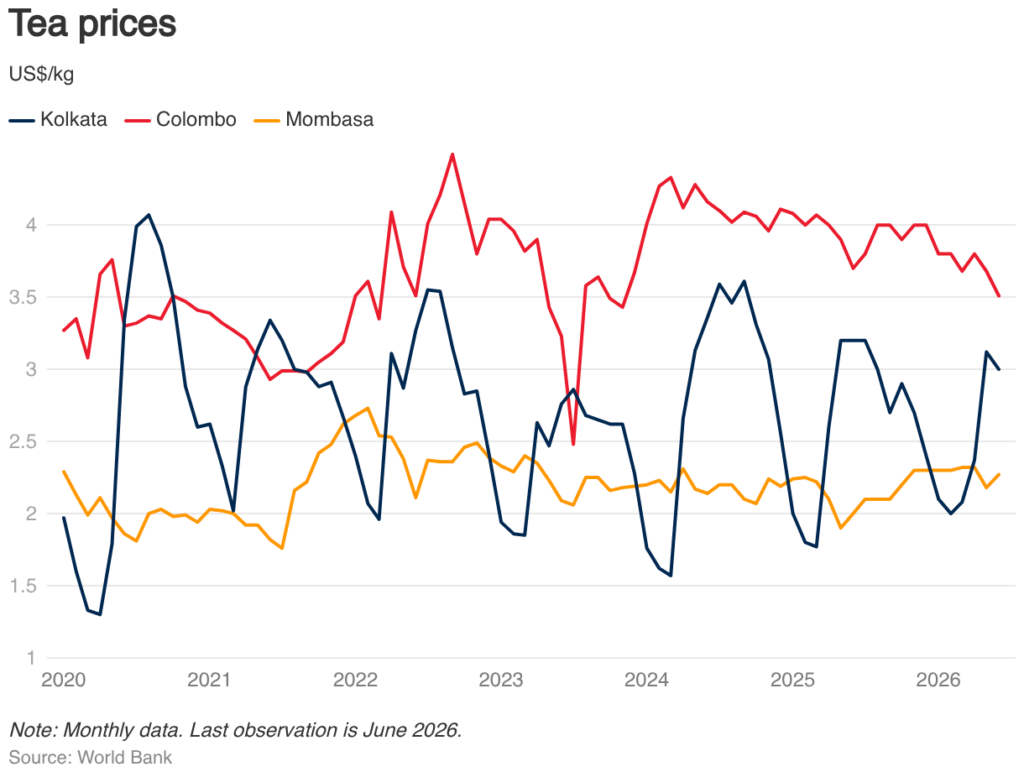

Tea prices (three‑auction average) edged lower in 2026Q2 (q/q). After falling 6 percent in May, prices at the Mombasa auction rebounded and have since stabilized. In contrast, prices at the Kolkata and Colombo auctions have softened over the past two months, reflecting ample global supplies. Despite some weather concerns in East Africa, the global tea market remains well supplied, largely due to rising output South Asia, including North India and Bangladesh. After easing 4 percent in 2025, tea prices are projected to decline by an additional 2 percent in 2026, weighed down by weak demand in the Middle East and North Africa (MENAP). A gradual recovery is expected in 2027 as demand conditions normalize. Risks to the price outlook remain tilted to the downside, particularly for East African teas. They include demand weakness in MENAP if shipping disruptions through the Strait of Hormuz do not normalize within 2026Q3.

Source : World Bank

")

")

.jpeg")

")

")

")

")

")

")