A successful transition to a green economy depends crucially on the availability of various critical raw materials. Currently, China dominates the production and processing of many of these materials, and most of the reserves are in countries that are not politically aligned with the Western economies. This column discusses the current situation and potential policy solutions.

With the World Meteorological Organization (WMO) issuing a warning that global temperatures are likely to surge to record levels in the next five years, the task of limiting global warming in line with the Paris Agreement – keeping global temperature rises well below 2°C (and ideally as low as 1.5°C) relative to pre-industrial levels – is becoming more challenging by the day. The necessary large-scale roll-out of clean technologies to fully decarbonise the electricity supply, electrify most final energy use, and scale up the use of low-carbon hydrogen requires a range of critical raw materials (Energy Transitions Commission 2023).These include (i) copper for wiring, (ii) rare earth elements for electric motors, (iii) lithium, nickel, and graphite for batteries, and (iv) silicon for solar photovoltaic (PV) panels. The amounts of materials involved are significant (Valckx et al. 2021, IEA 2022). Few substitutes are available for these inputs at present, and Western economies have poor access to many of them. This would be challenging at the best of times but is even more fraught with rising geopolitical tensions and Russia’s war on Ukraine. In recent work (EBRD 2023), we document the scramble for critical raw materials and discuss possible solutions.

Western economies have poor access to many critical raw materials

The supply risk that is associated with a critical raw material is determined by (i) where it is mined and processed, and (ii) the general availability of reserves (known commercially viable deposits in the ground). For example, rare earth elements tend, on average, to be more abundant than silver, gold and platinum (despite what their name suggests); however, few of those deposits are concentrated and economically viable to mine (Van Gossen et al. 2014).

If a country does not have critical raw materials within its territory, firms located in that country may seek to acquire mines overseas or import such materials from trading partners that are regarded as reliable (for instance, countries that are aligned in geopolitical terms).

To analyse the extent to which such similarities in values might affect countries’ bilateral trade in critical raw materials, we use data on the United Nations (UN) General Assembly voting between 2014 and 2021 and, following a large political science literature, measure countries’ bilateral political attitudes towards one another using the similarity of their UN votes. We divide them into two blocs based on (i) average ideal points on a unidimensional scale and (ii) the Jenks natural breaks classification method. Bloc 1 comprises countries that are more closely aligned with the United States and other Western economies, while Bloc 2 contains the rest of the world (including China). Of the various countries in Bloc 2, Armenia is the closest to Bloc 1 using this measure.

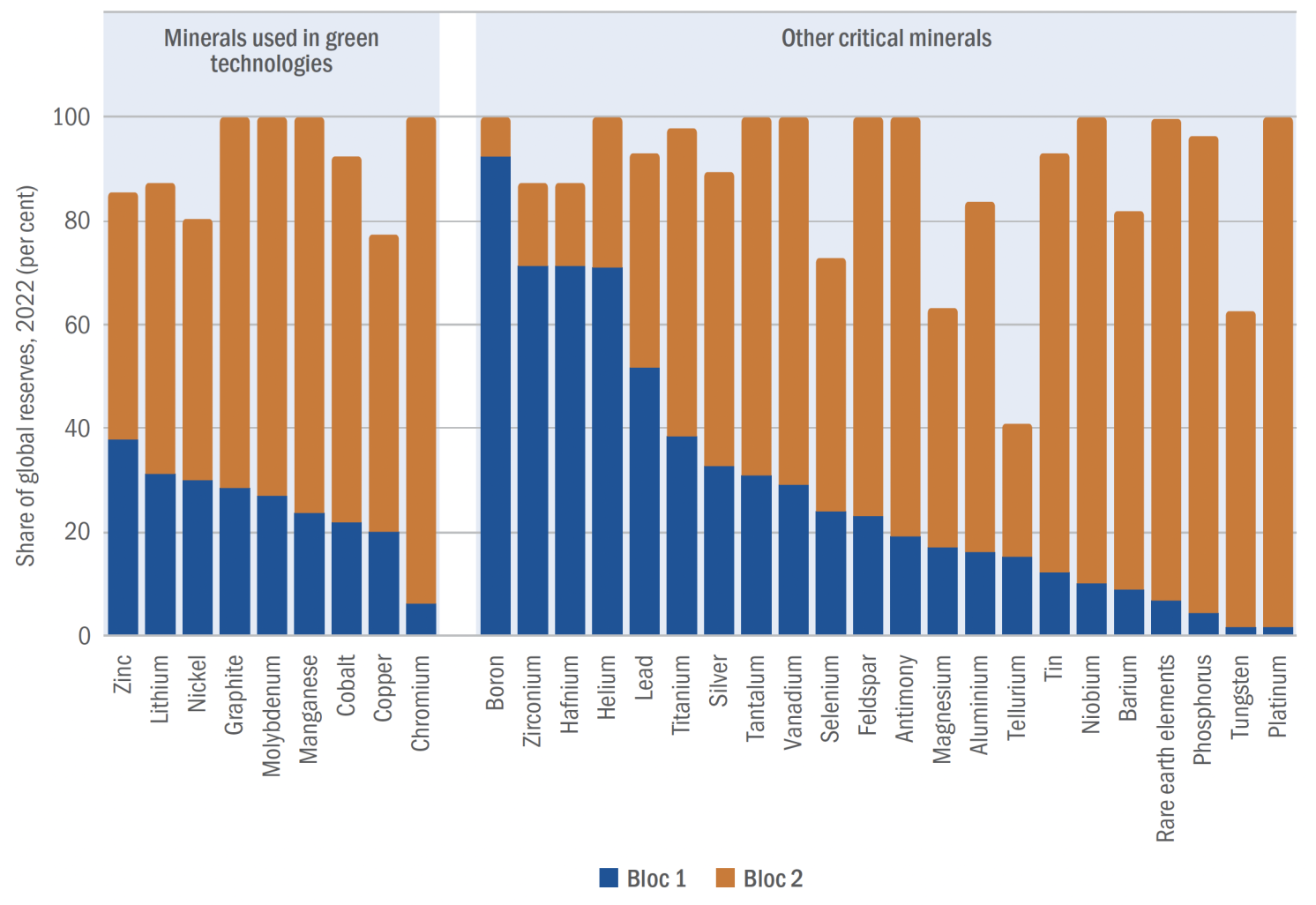

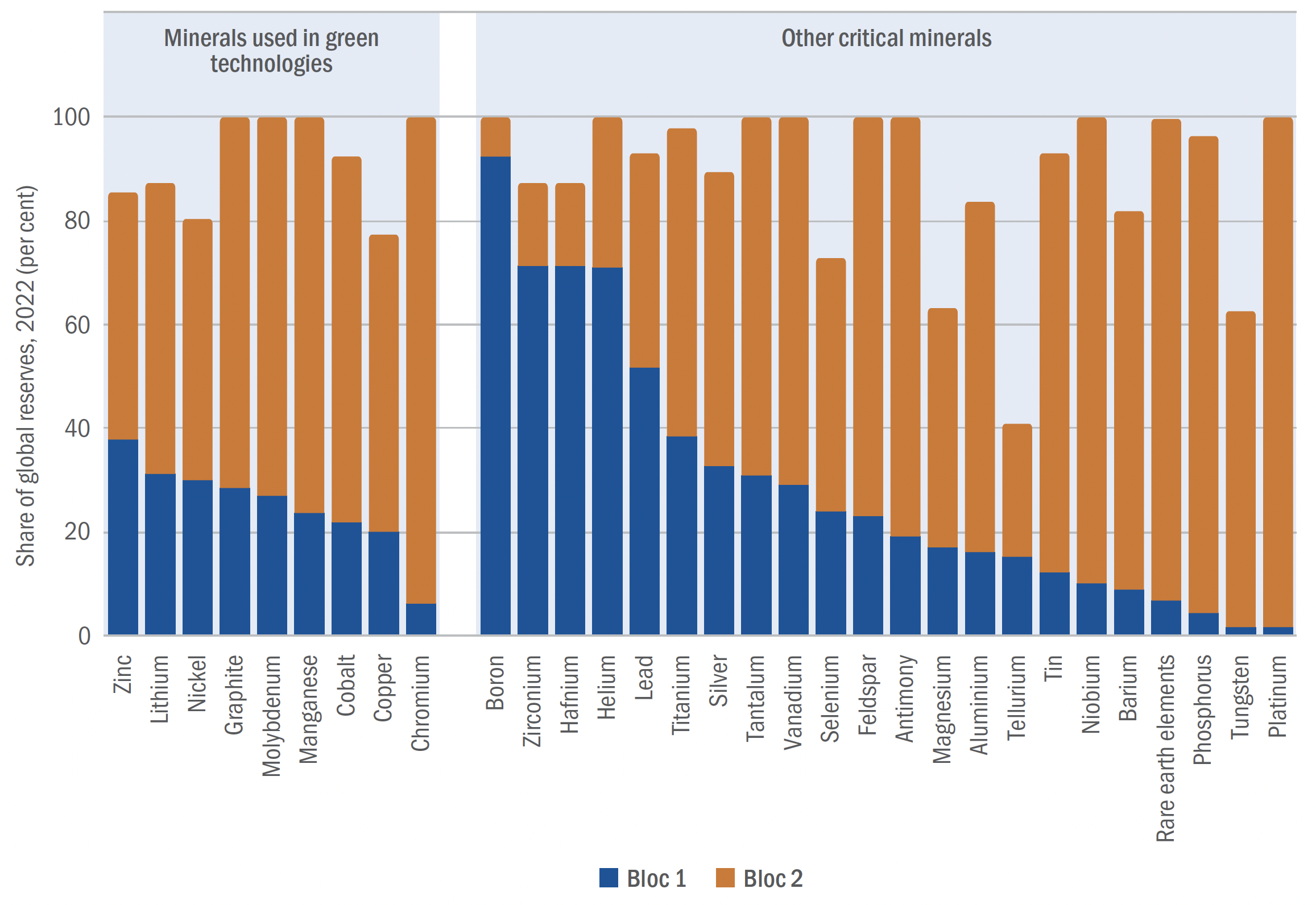

Figure 1 shows that Bloc 2 dominates the known reserves of all raw materials critical for the green transition, as well as most other critical raw materials (except for boron, zirconium, hafnium, helium, and lead). Importing critical raw materials from politically aligned trading partners would thus not solve the problem.

Figure 1 Reserves of critical raw materials in countries geopolitically aligned with the West and the rest of the world

Source: S&P, Voeten (2013) and authors’ calculations.

Note: Based on the location of mines.

China dominates the production of most critical raw materials

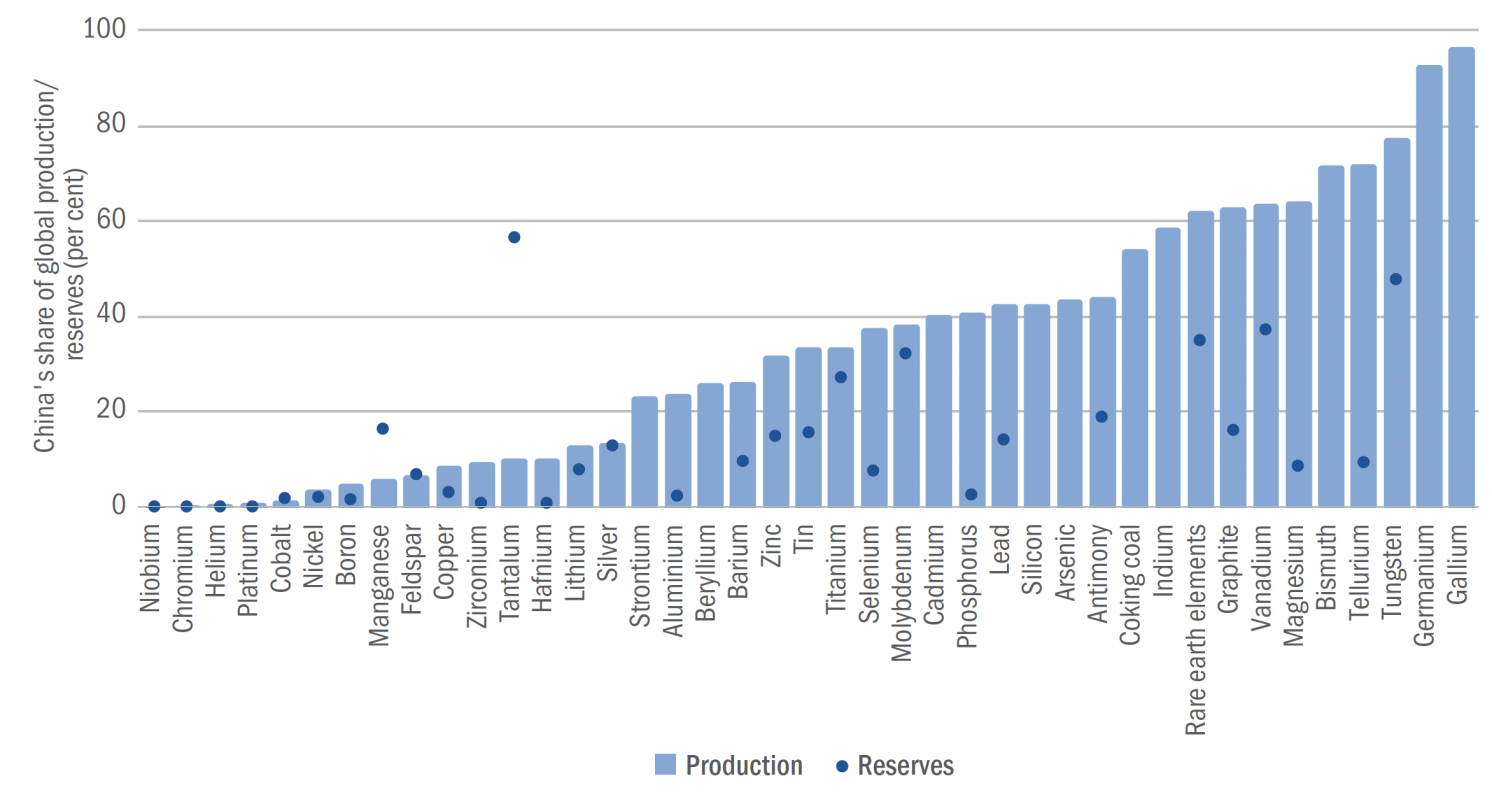

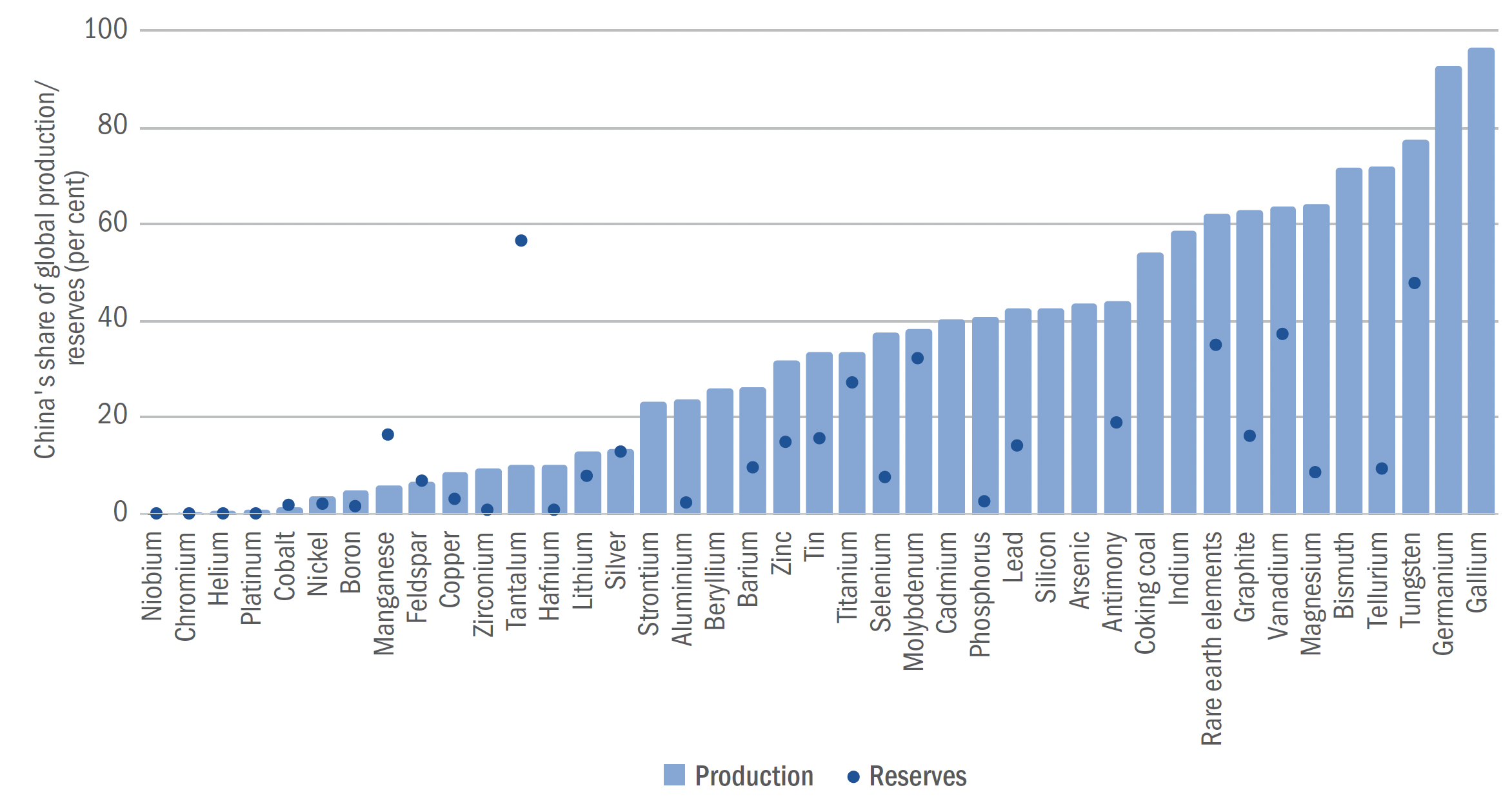

The production of critical raw materials is heavily concentrated in a handful of countries, particularly China (Figure 2). The minerals with the highest levels of geographical concentration are gallium and germanium (used in chips), followed by niobium (used in steel alloys) and tungsten (used in wear-resistant metals). In contrast, zinc (used to protect steel from corrosion), silver (used in solar cells) and copper mining are the most geographically diversified.

Reserves are only slightly more geographically diversified. While China has more than half of all known reserves of tantalum (used in electronic components), as well as significant percentages of the world’s reserves of tungsten, vanadium (used in batteries and steel) and rare earth elements, almost 90% of all known reserves of niobium and boron (used in fertilisers, EVs, wind turbines and solar panels) are in Brazil and Türkiye, respectively.

Figure 2 In 2021, China dominated the production of most critical raw materials

Source: EBRD (2023).

Note: “Platinum” refers to the platinum group of metals. Data on reserves are not available for certain minerals. Production refers to 2021, while known reserves to 2022.

As the scramble for resources has intensified, major mining companies have sought to explore deposits and buy mines around the world. While companies headquartered in the US and Canada own the most mines overseas, Chinese companies have been actively buying overseas mines over the past decade. In Africa, which is home to about 30% of all known mineral resources, the number of Chinese-owned mines has doubled since 2013. From an individual country’s perspective, acquiring overseas mines increases the security of supply for critical raw materials.

Does it matter?

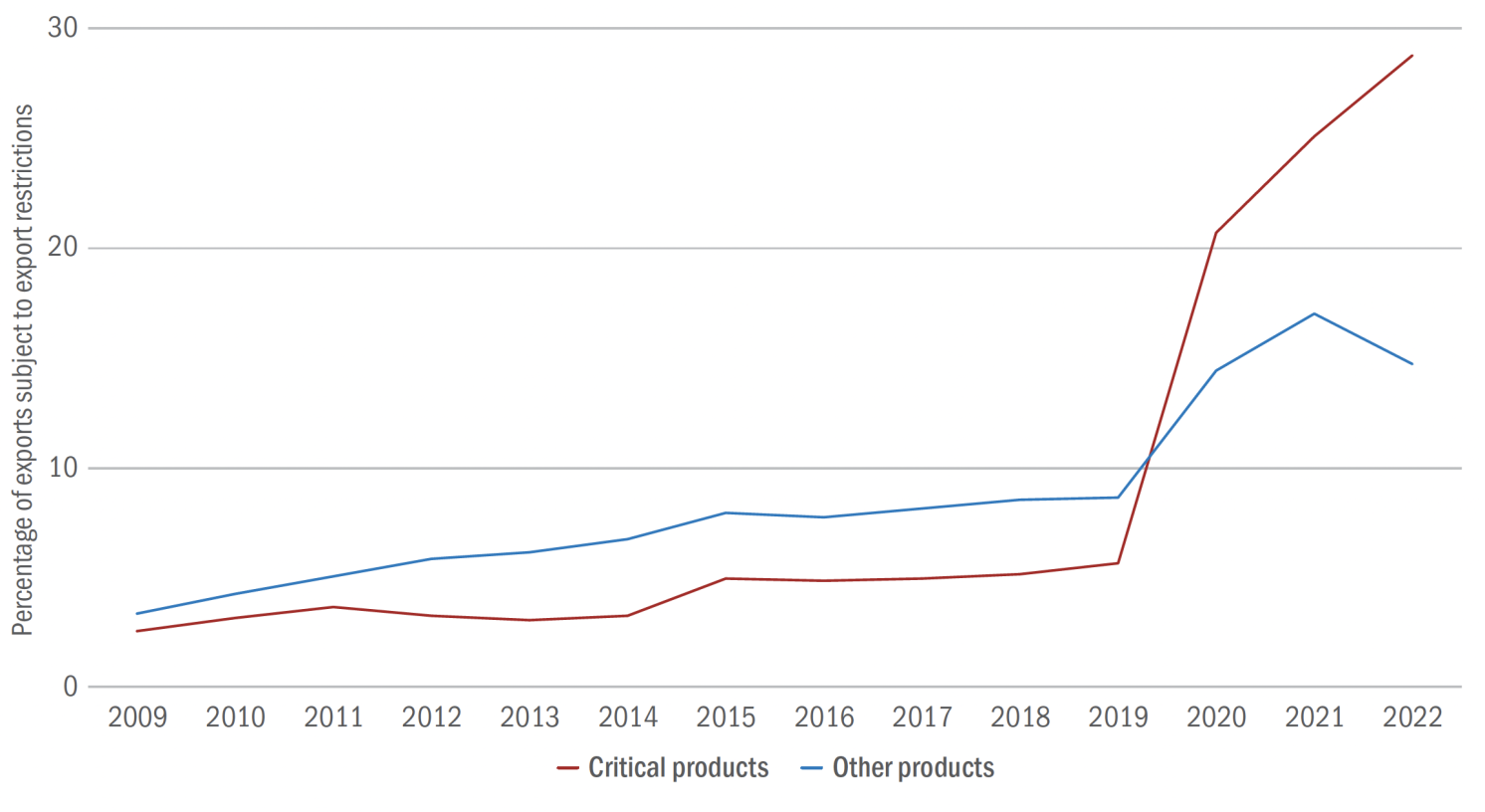

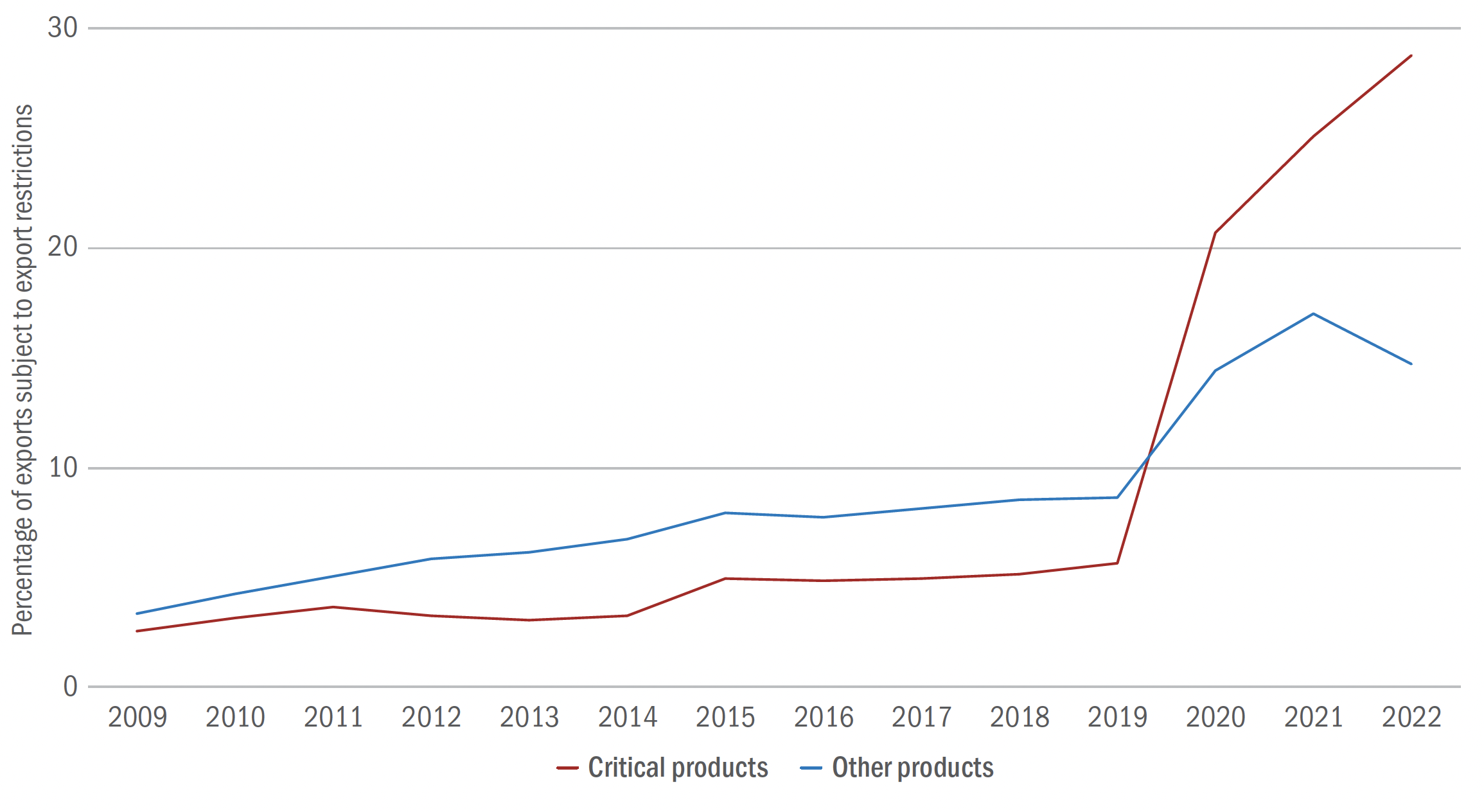

Access to critical raw materials and products that (currently) cannot be manufactured without them is important because they are crucial for a successful green transition. While demand for critical raw materials has grown in recent years, the percentage of critical products that are subject to export restrictions shot up around 2020. Data on export restrictions taken from the Global Trade Alert can be combined with data on international trade flows to gauge the economic importance of such restrictions (Evenett and Fritz 2020). This analysis reveals that around 30% of global exports of critical raw materials by value were subject to restrictions in 2022, up from just 5% in 2019 (Figure 3). A much smaller increase, 5 percentage points, was observed for other products over that period, reflecting broader trends in terms of geopolitical tensions and the fragmentation of global trade (Aiyar and Ilyina 2023).

Figure 3 Export restrictions on critical products have surged since 2019

Source: EBRD (2023).

Note: Global Trade Alert data as at 11 July 2023.

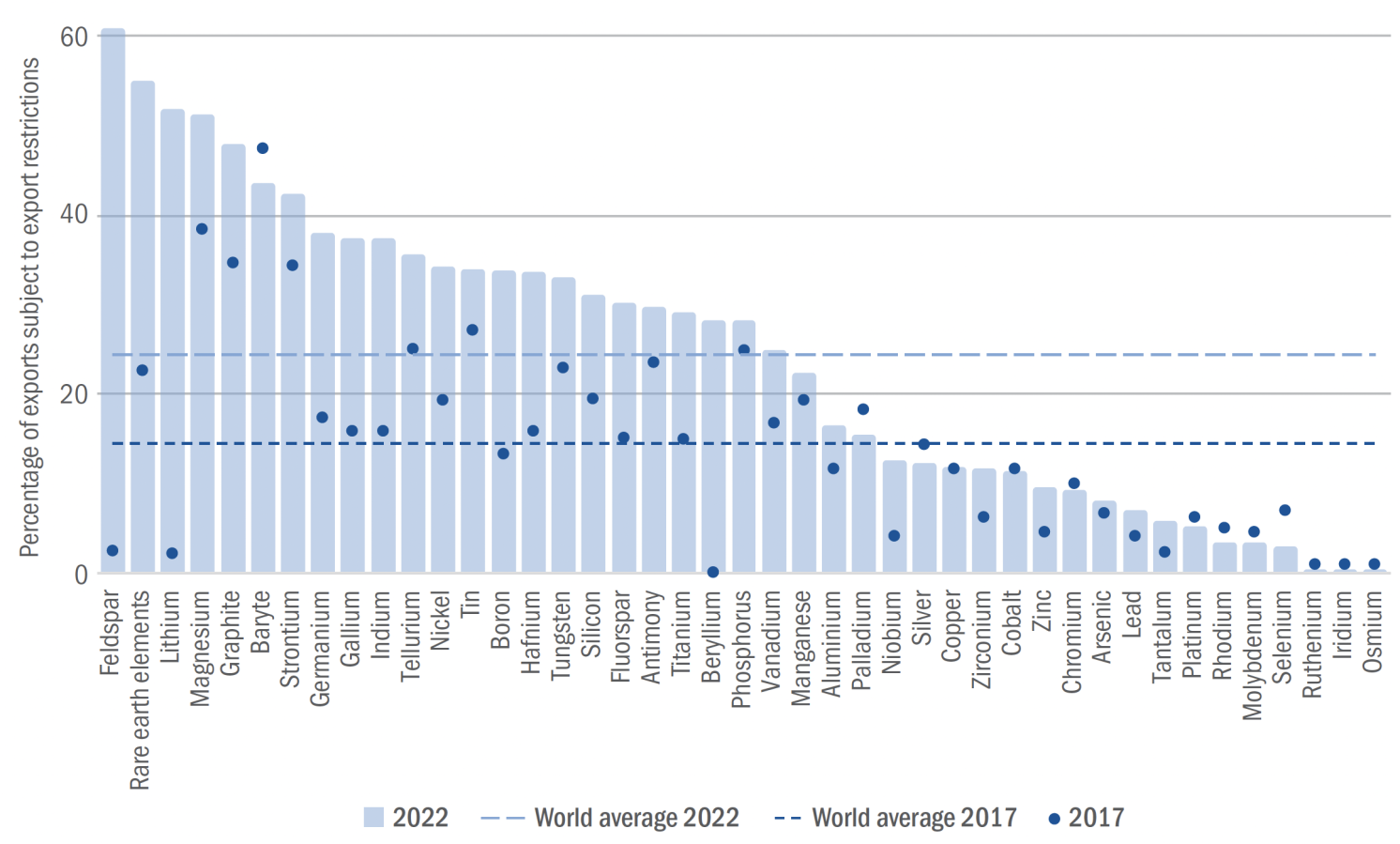

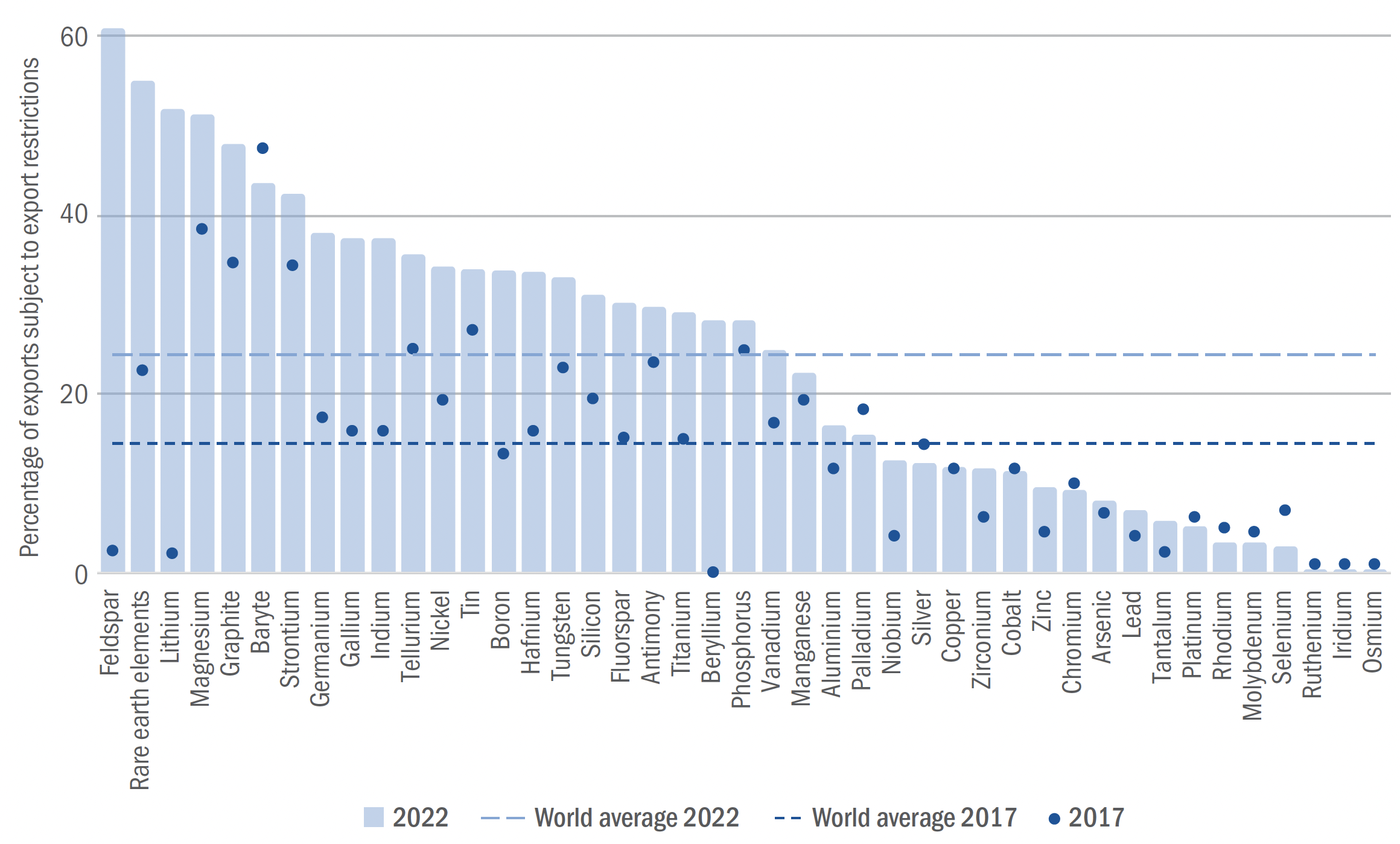

The biggest increases in the percentage of critical materials subject to export restrictions occurred in the US, Vietnam, and China.In terms of individual materials, export restrictions have been tightened for feldspar, lithium, and rare earth elements, while trade in selenium, baryte, and palladium has become less restricted (Figure 4).

Figure 4 Export restrictions have increased substantially for lithium and rare earth elements

Source: EBRD (2023).

Note: Global Trade Alert data as at 11 July 2023.

Countries impose export restrictions on critical raw materials to capture more of their value by embedding them in other domestically manufactured products, or to make it more costly for others to obtain them. For example, when the US CHIPS and Science Act of 2022, which provides subsidies for the construction of semiconductor manufacturing plants, prohibited recipients of such subsidies from expanding semiconductor manufacturing in China or other countries that pose a threat to US national security, China retaliated by imposing restrictions on exports of gallium and germanium.

Source : VOXeu

")

")

.jpeg")

")

")

")

")

")

")