The pandemic led to a significant shift in preferences toward suburban living in the US and an increase in relative house prices in suburban compared to urban areas. In several US cities, this dynamic has flattened the traditionally negative relationship between house prices and distance from city centres. This column documents the continued nature of these shifts in the US, their heterogeneity across different US cities, and contrasts them with the experience in Europe. The authors argue that disparities in socioeconomic characteristics and property sizes between US and European suburbs underlie the trend divergence. The analysis also highlights how the suburban versus urban valuation shift was predominantly driven by high-income household migration in the US.

Housing markets have long been characterised by a premium for city-centre living, with property prices reflecting a negative relationship with distance from the urban core (Albouy et al. 2018). In the US, the COVID-19 pandemic altered this relationship. The shift towards remote work, coupled with a growing preference for more spacious living and reduced need for proximity to urban centres, prompted a shift towards suburban living (Ramani and Bloom 2021, Liu and Su 2021). This shift effectively flattened the previously steep gradient between house prices and their distance from city centres, with suburban homes witnessing a more rapid increase in value compared to their urban counterparts (Gupta et al. 2022).

In a recent paper (Biljanovska and Dell’Ariccia 2023), we investigate whether house price gradients in the US – defined as the elasticity of house prices to the distance from the city centre – have continued to rise or have reverted to pre-pandemic levels. Furthermore, we examine whether similar trends were observable beyond the US, focusing on selected European countries, including Denmark, France, and the UK, thereby providing a broader perspective on the pandemic’s impact on housing markets. Finally, building on these findings, we explore the factors contributing to the heterogeneity of house price behaviour across American metropolitan areas, with a particular focus on how differing features of the markets between the US and Europe might explain these variations.

Persistent weakening of the house price and distance relationship in the US

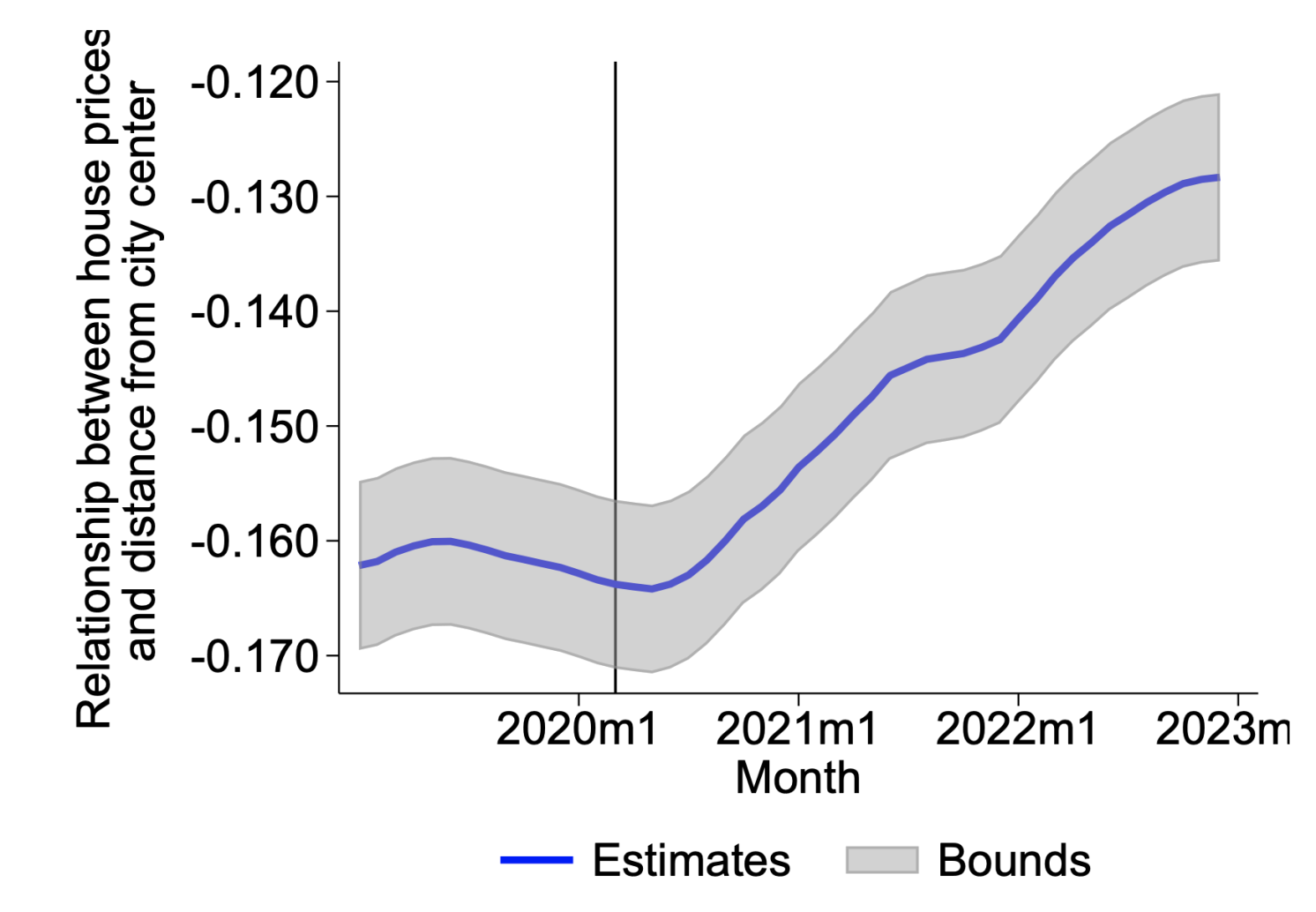

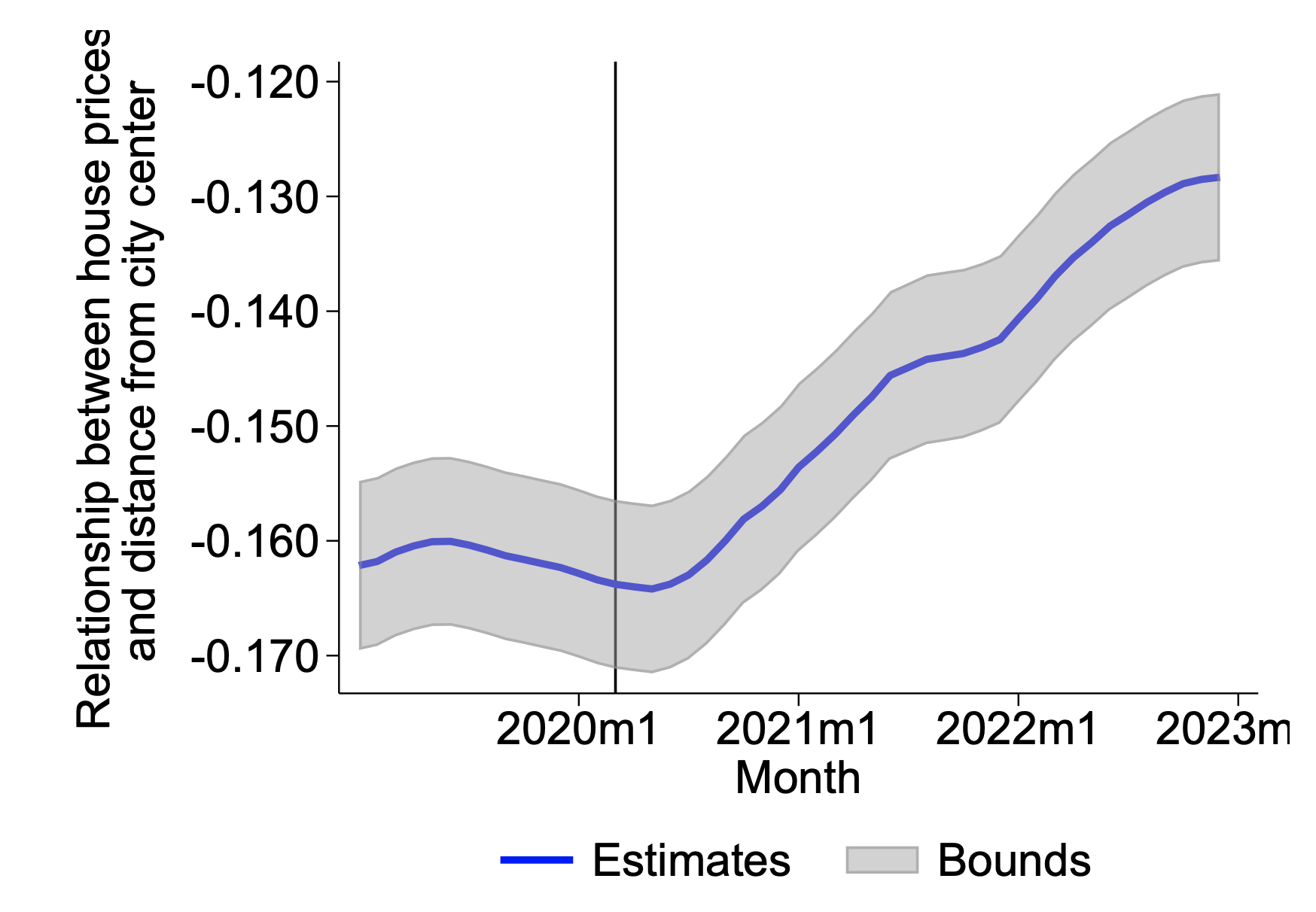

The effect of the pandemic on relative house prices in American cities is proving highly persistent (Figure 1). The average price gradient across the top 30 US metropolitan areas continued to climb, even as the pandemic was fading away. In other words, house prices in the outer regions of cities continued to outpace their inner counterparts until the second half of 2022. The persistence of this trend is likely due to the continued popularity of remote work and the desire for more spacious living.

Figure 1

Note: The figure plots the time-varying relationship between house prices and distance from a central zip code. The estimates are obtained from a panel regression from the top 30 metropolitan areas in the United States over the period January 2019 to December 2022. The vertical line marks March 2020, noting the start of the pandemic.

Lack of weakening in the house price and distance relationship in Europe

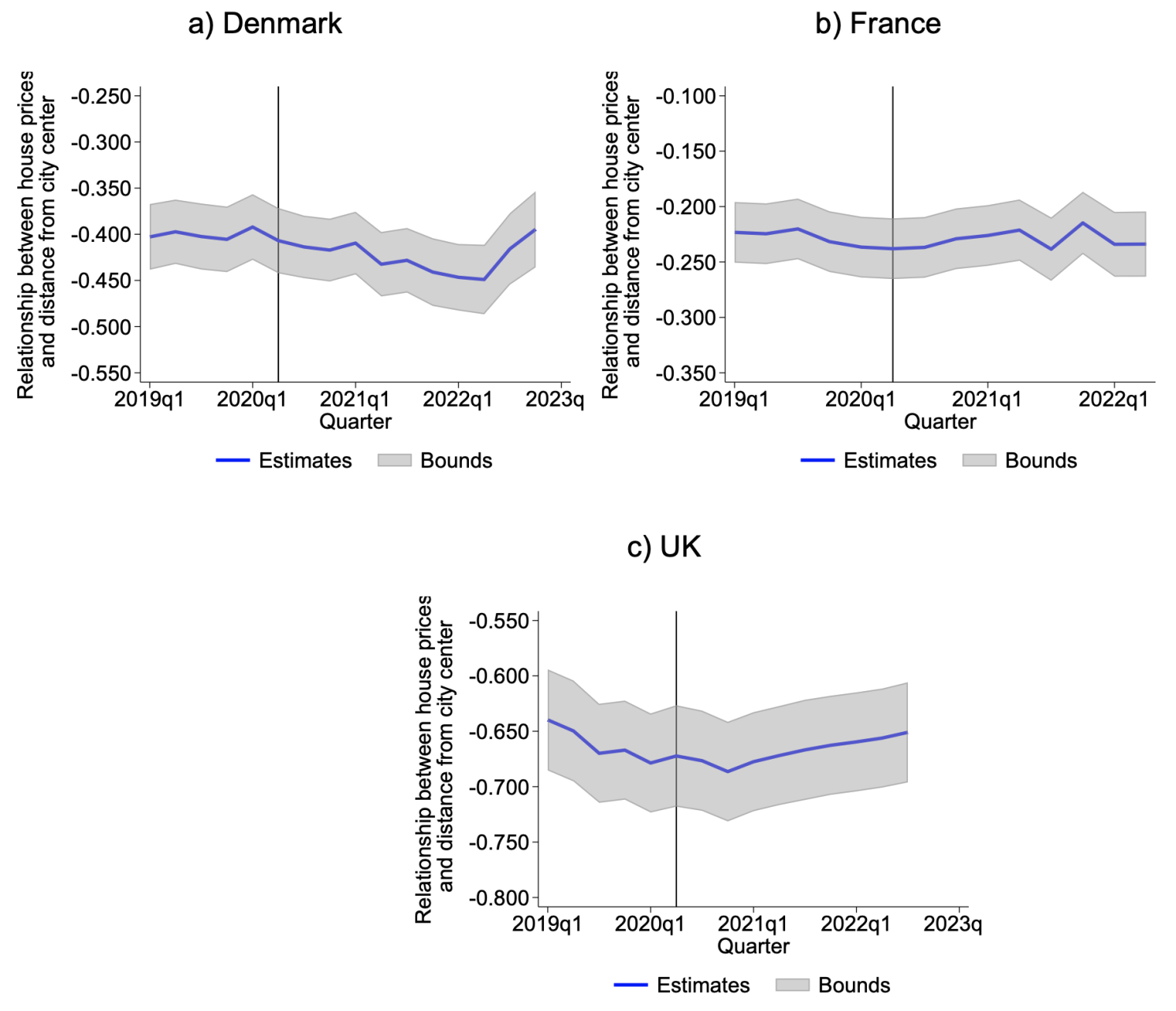

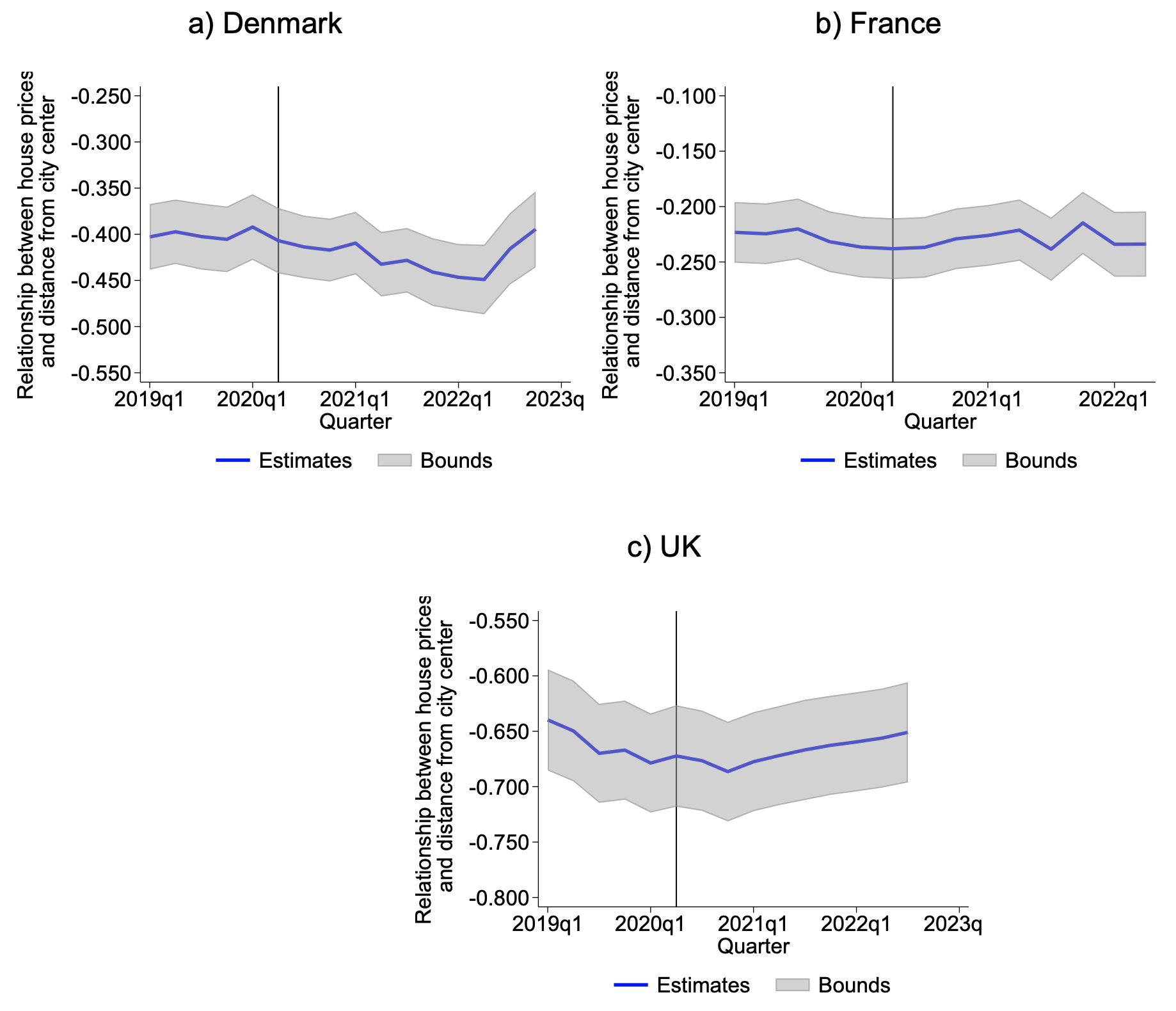

This continued flattening of the gradient did not seem to find a counterpart in Europe. Relative house prices in cities in Denmark, and to a large extent in France and the UK, did not follow the same trajectory seen in the US (Figure 2). In these countries, gradients held steady from 2020 to 2022, indicating that the pandemic did not notably alter households’ preferences between suburban and downtown living.

Figure 2

Note: The figure plots the time-varying relationship between house prices and distance from a central postcode. The estimates are obtained from a panel regression from the largest 2 cities in Denmark (Copenhagen, Aarhus), 3 cities in France (Paris, Lyon, Marseille), and 6 cities in London (London, Birmingham, Leeds, Liverpool, Manchester, Sheffield). The estimates are obtained from a panel regression for each country individually over the first quarter of 2019 to the last quarter of 2022 (or latest data available in 2022). The vertical line marks March 2020, noting the start of the pandemic.

We posit that differences in socioeconomic and property characteristics between US and European suburbs can help explain the divergence in housing markets dynamics across the two sides of the Atlantic and the heterogeneity across American metropolitan areas. Relative to city centres, European suburbs tend to be poorer and offer more limited services. In contrast, in the US, suburbs tend to be richer than city centres and often come with higher quality of public services. In addition, the property structures in the suburbs differ significantly between the two regions. American suburbs feature larger homes and amenities, attributes that became highly desirable during the pandemic. European suburbs, on the other hand, tend to offer smaller living spaces, appealing to a broader, more economically diverse population. Both these elements may have represented an obstacle for relatively wealthier Europeans to relocate outside cities.

Did some cities in the US have the European experience?

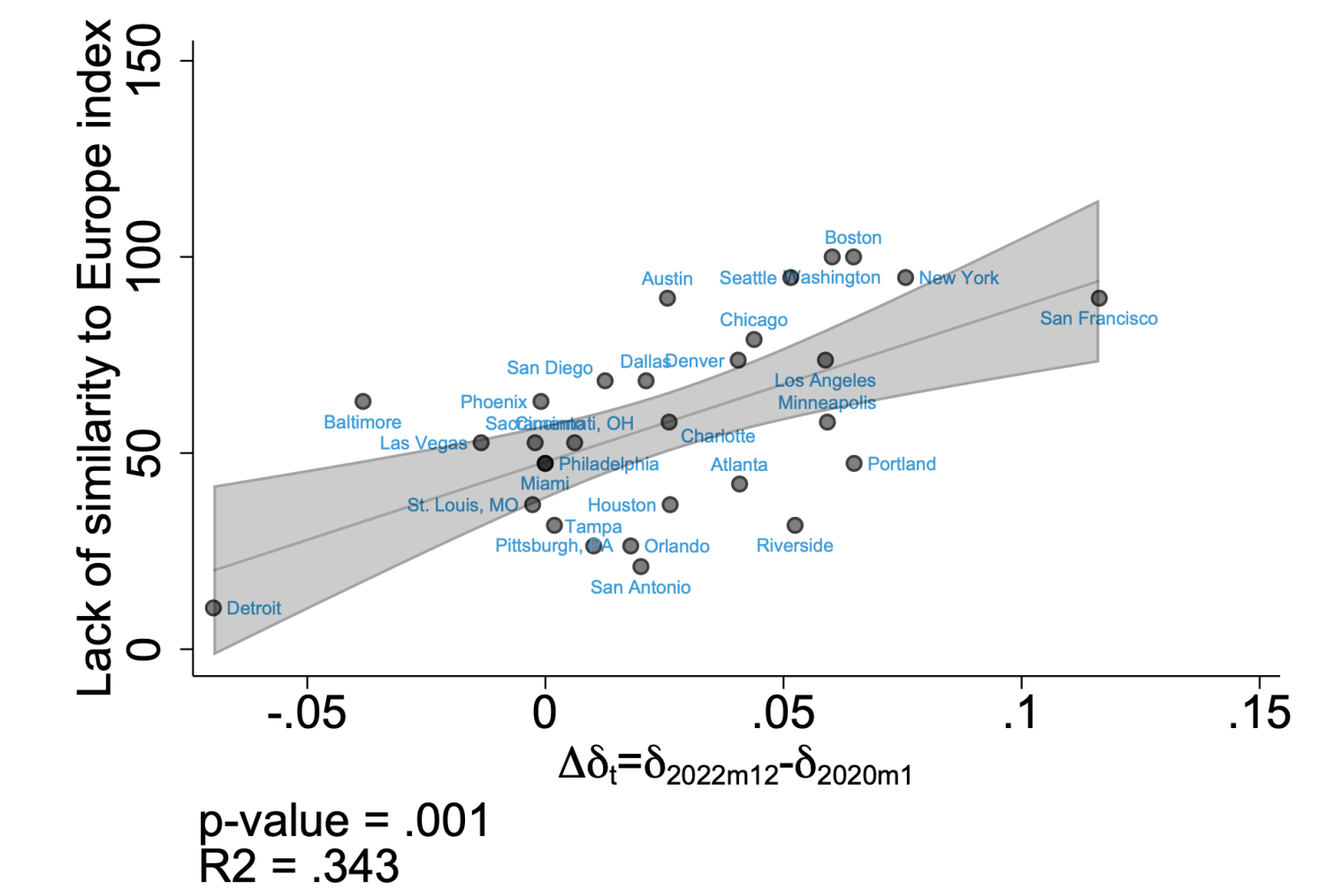

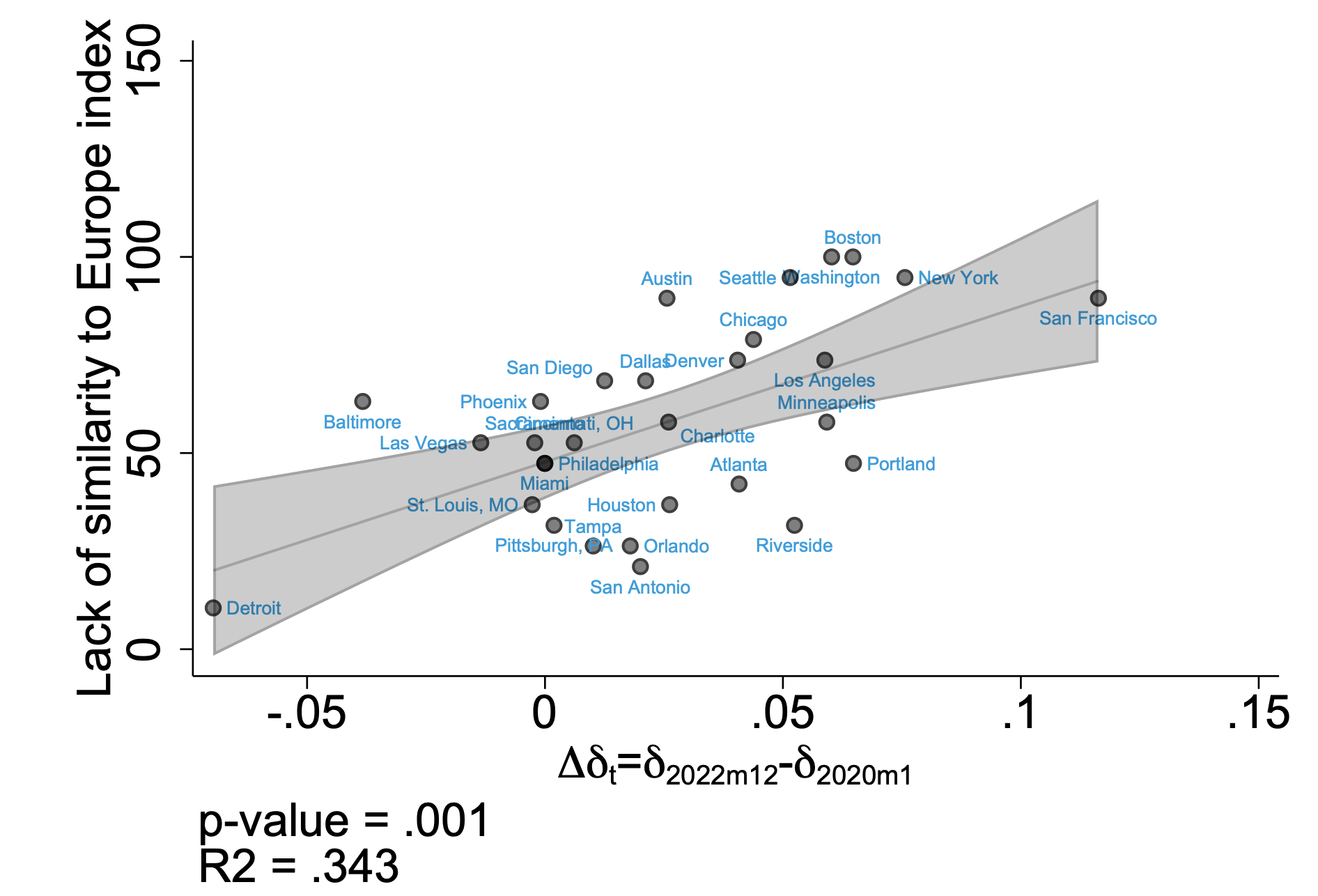

By exploiting the variation in house price gradients across the top 30 MSAs in the US, we investigate whether American cities with suburban characteristics akin to Europe in terms of relative income and property size experienced a less pronounced flattening of price gradients. Our hypothesis would suggest that such cities would exhibit a milder increase in price gradients. Our analysis supports this notion: MSAs with suburbs characterised by relatively lower average income and smaller property sizes indeed showed a more modest rise in their price gradients (Figure 3).

Figure 3

Note: The scatter plot shows the relationship between the similarity-to-Europe index and the change in the price gradient between January 2020 to December 2022 for the top 30 metropolitan areas in the United States. A larger value of the index implies lower similarity to Europe in terms of household income and property size in suburban areas.

Flight of the rich

We then analyse the demographics driving the urban exodus and the rise in suburban house prices. Our findings indicate that the significant increase in suburban prices is largely due to the mobility of affluent households, whose jobs support remote work and whose financial means support relocation. This trend underscores the impact of high-income mobility on suburban demand, consistent with Gupta et al. (2022), who identify remote work as a key factor behind the variation in house price gradients across US metropolitan areas.

What are the implications of these shifts for the future of commercial and residential real estate?

These shifts in real estate markets have multifaceted implications for both commercial and residential sectors. For commercial real estate, particularly in the US, the persistence of urban-suburban house price rebalancing reflects continuing preference for working from home with immediate challenges, including low occupancy rates in office buildings and decreased city-centre traffic, which in turn may affect regional banks due to concentrated exposures. Moreover, US cities may confront medium-term financial strains from lower tax revenues, exacerbated by reduced business activities and the exodus of affluent residents.

On the residential side, the influx of wealthier residents into suburban areas carries significant consequences for housing affordability. While existing homeowners may see an increase in their property values, enhancing household wealth, the surge in house prices poses a substantial barrier to entry for new buyers. This escalation in prices may precipitate a demographic shift, sidelining lower-income households from suburban markets and reshaping the socioeconomic composition of these communities. At the same time, a rebalancing of demand away from the most coveted neighbourhoods in city centres may ameliorate the affordability problems in some downtown areas.

Source : VOXeu

")

")

.jpeg")

")

")

")

")

")

")