Debt mutualisation is a politically complex and sensitive topic. Advocates argue that it lowers debt service costs and could enhance incentives for compliance with fiscal rules. Opponents say that it would lead countries to abandon any remaining fiscal restraint and is a political non-starter as one country must pay for the past deficits of another. This column argues that jointly issued euro area debt of about 15% of the region’s GDP could be issued safely and without direct fiscal transfers; but debt mutualisation is no silver bullet.

The pandemic revived a longstanding debate between euro area countries on whether to jointly issue debt to address the deep economic downturn – an idea first raised by the German Council of Economic Advisors in 2011 (Weder di Mauro et al. 2011, see also Micossi 2020).

Debt mutualisation – transferring a portion of existing sovereign debt to a joint euro area agency – is a politically complex and sensitive topic (D’Amico et al. 2022). Advocates argue that it lowers debt service costs and could enhance incentives for compliance with fiscal rules. Opponents say that it would lead countries to abandon any remaining fiscal restraint and is a political non-starter as one country must pay for the past deficits of another.

In a new paper (Ando et al. 2023), we take a different approach. On purpose, our analysis asks a narrow question and carefully avoids a broader one.

The narrow question is: How much revenue could be raised in the euro area via a mutualisation without direct fiscal transfers from low-debt countries to high-debt ones? The answer, as explained below, is about 15% of the region’s GDP, representing about 16% of its outstanding public debt. The broader question is: Should it be done? An answer to that question is well beyond our analysis. It requires addressing many additional political and technical hurdles, including how to ensure countries remain on a safe fiscal trajectory from that point onwards. Instead, our analysis, without arguing in favour of or against any specific proposal, provides a framework that contributes to recent discussions on the case for a fiscal union in the euro area and on the need to reform the European fiscal architecture (Berger et al. 2019, D’Amico et al. 2022, IMF 2022). These discussions are essential amid elevated public debt and rising interest rates.

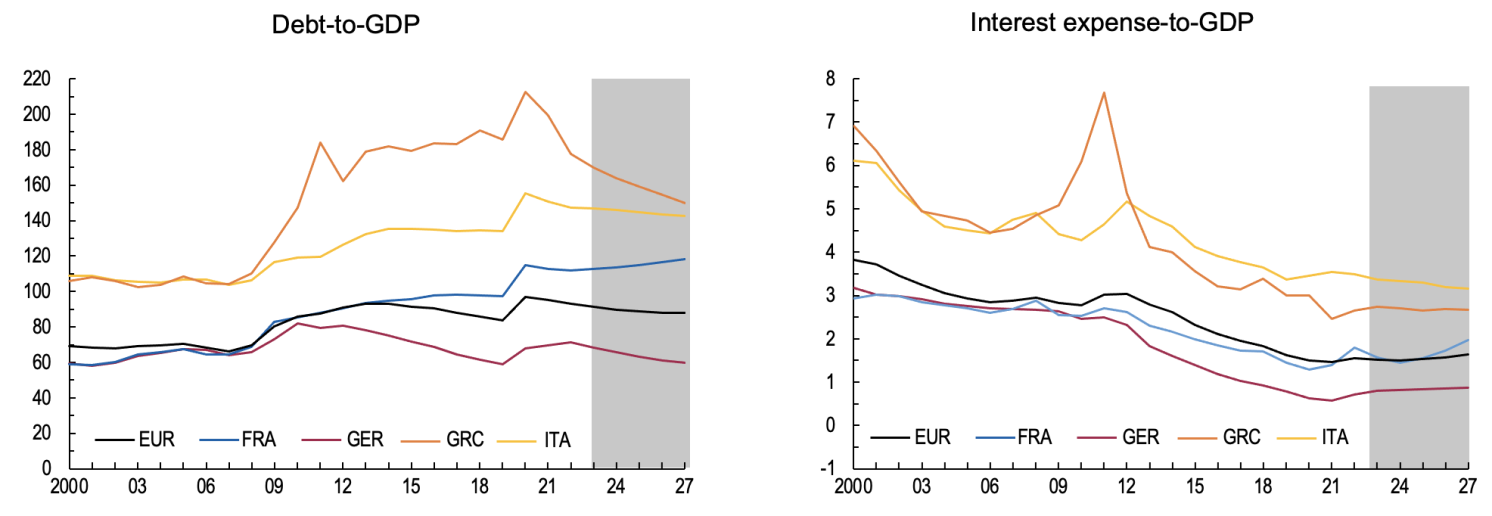

Figure 1 Debt and interest expense-to-GDP

Our approach estimates the benefits that could be obtained by capitalising a common and largely untapped implicit fiscal resource: the convenience yield on a euro area safe asset. This refers to the high price international investors are willing to pay to hold truly safe assets. This well-documented scarcity is one of the reasons yields on the safest assets, such as US Treasuries or German Bunds, are lower than the competition.

If this convenience yield is large enough, average interest rates on safe assets will be lower than growth rates. This has been the case since at least the global financial crisis. Even now, with tighter monetary policy, nominal interest rates for safe assets remain lower than nominal growth rates.

In such an environment, it is theoretically possible (Blanchard 2023) to issue some debt and roll it over permanently (together with interest payments), without having to raise taxes to pay either interest or principal. Both debt and GDP would grow over time, but because GDP grows faster than debt, the ratio of the two would shrink, making the debt increasingly insignificant from an economic point of view.

But what is true in theory is not necessarily true in practice. Interest rates and growth fluctuate. Moreover, if the amount of debt becomes very large in relation to the size of the economy, it is unlikely investors would still consider it safe, and interest rates would soar. In other words, how much safe debt could be issued without the need for future taxes is a quantitative question.

Using stochastic simulation tools, we tackle this question by calculating the amount of additional debt that could be issued through the creation of a European Debt Management Agency, while making sure that the debt remains safe. By this, we mean that the rolled over debt declines in relation to GDP with at least 95% probability, at a three-year horizon.

Even under conservative assumptions, we find that such an agency could issue up to 15% of the region’s GDP.

Next, we consider a simple scenario where this new common resource is used to retire some national debt for the ten euro area countries with debt ratios in excess of the Treaties’ 60% threshold. Allocating the proceeds from the agency proportionally to GDP would reduce debt-to-GDP ratios by an average of 26 percentage points in each of these countries.

This would offer significant fiscal relief. On average, it would reduce the level of primary balances (the excess of government revenues over expenditures excluding interest expenses) required to put debt-to-GDP ratio on a firmly downward-sloping trend between 0.4% of GDP per year (Belgium) and 0.7% (Italy).

However, we find that, at current policies, this would not be sufficient, on its own, to ensure declining debt ratios with 95% probability for Belgium, Finland, France, and Spain. Based on the stochastic simulations in our paper, for these countries, an additional fiscal consolidation of between 1.3% and 2.3% of GDP per year is still needed to start lowering debt, with a high probability, after three years.

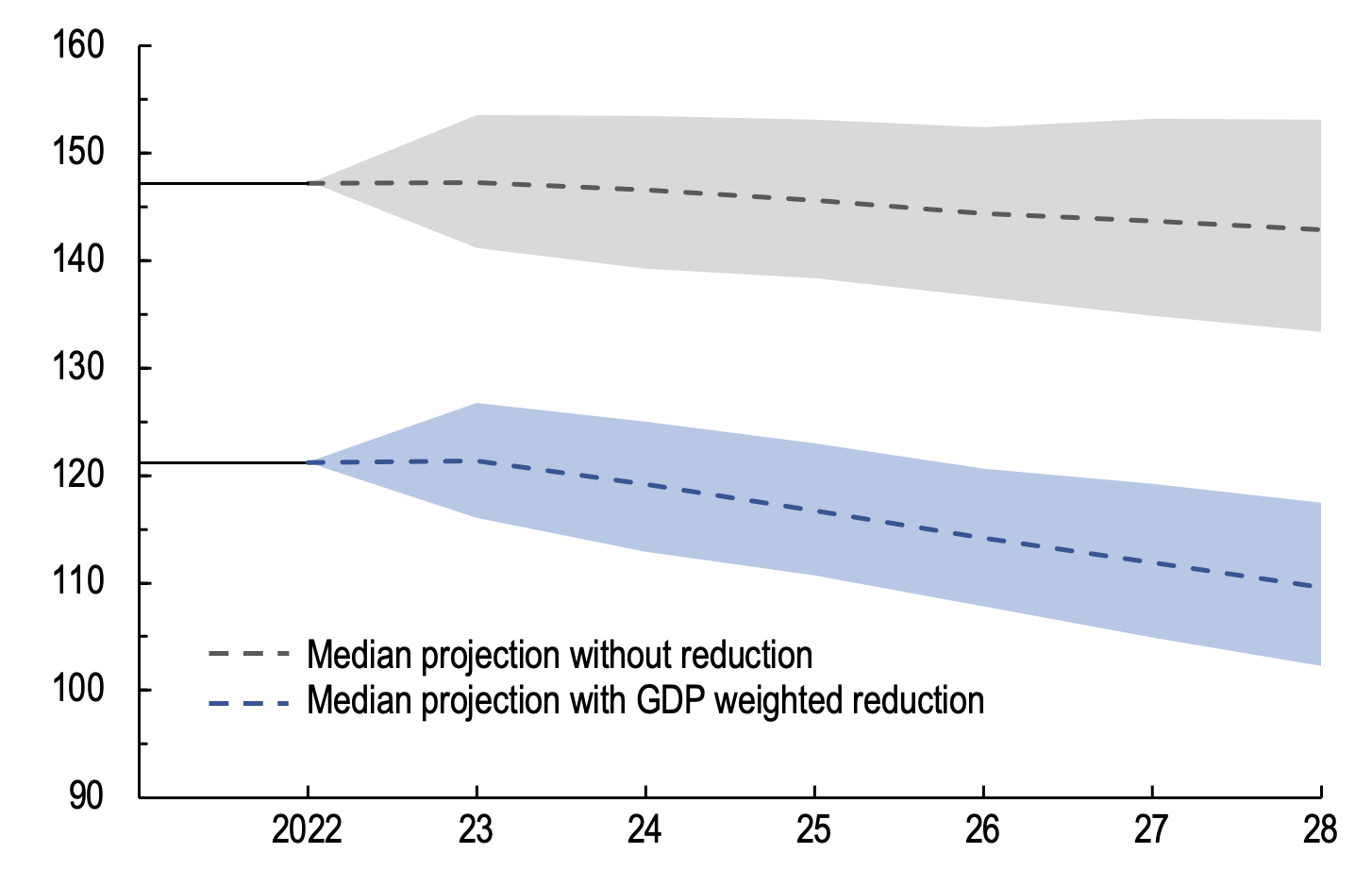

For Italy, by contrast, debt mutualisation would help to put the country’s debt on a declining path, with a probability of over 95% after three years. Without debt mutualization, instead, it is likely that Italy’s debt-to-GDP ratio would remain stagnant or increase over time.

Figure 2 Effects of mutualisation in Italy

Stochastic simulations for debt to GDP

Source: WEO October 2022 and IMF staff calculations.

Note: Shaded areas represent 5th-95th percentile projections.

Such a substantial debt issuance by the agency could impact the yield faced by other safe asset issuers in the region, such as Germany. On the one hand, debt mutualisation could help lower the risk of future fiscal crisis which would also affect low debt countries. This would push down the Bund’s rate. On the other hand, the increased supply of a euro area safe asset could decrease the price of close substitutes such as the Bund. This would push Bund rates up. The analysis in our paper represents an upper bound estimate (as it does not take into account the first effect described above) but suggests that the impact on German public finances would likely be manageable (in a way, one can see this cost as the price of insurance against the risk of a sustainability crisis).

We also consider what would happen if the yields on the remaining national debt increased because of debt mutualisation. Under conservative assumptions on the associated premium, the gains in terms of the reduction in the required fiscal consolidation to ensure declining debt ratios with high probability would be significantly more modest. For instance, in the case of Spain, the required fiscal consolidation is reduced from 1.8% of GDP without debt mutualisation to 1.7% with mutualisation.

Implications

Debt mutualisation could help reduce debt levels and improve public finance sustainability in some euro area countries, but it is unlikely to be sufficient to fully put public finances on a safe path.

Clearly, the benefits depend on the real interest rate being lower than the real growth rate with sufficiently high probability. With the recent tightening of monetary policy, real interest rates have increased and growth is slowing, reducing the scope for a self-funded debt issuance (Collard et al. 2023). But higher rates and slow growth also pose risks for national debt trajectories. Our simulations take as starting point nominal one-year interest rates on mutualised debt of 1.42% in 2022. Our results show that, even with these relatively higher rates (and lower growth as projected in the World Economic Outlook), the agency could safely issue debt up to 15% of euro area GDP.

Debt mutualisation is not a silver bullet. A precondition for its success is a comprehensive package of complementary reforms carefully calibrated and implemented to ensure countries remain on a sound debt trajectory and minimise moral hazard (the idea that mutualisation would reduce fiscal discipline in countries that receive debt relief). For instance, the EU’s decade-old push for a unified banking market would also need to be completed and national concentration limits imposed to prevent banks and sovereigns from going insolvent in a debt crisis. A proper fiscal framework should also be implemented (IMF 2022). None of these would be easy. But the reduction in debt levels along the lines analysed above could in principle be part of the package.

Source : VOXEu

")

")

.jpeg")

")

")

")

")

")

")