Despite falling interest rates over the past decades, investment rates have not increased as standard economic theory would suggest. This column constructs a global database of firm discount rates and cost of capital using corporate conference calls, and matches this to investment rates. It finds that changes in the cost of capital only modestly affect discount rates, giving rise to a time-varying wedge between the two measures. A standard model enriched with discount rate wedges helps resolve the ‘investment puzzle’ in the US. These findings have implications for modelling firm behaviour and for the design of policy by governments and monetary authorities.

A pressing puzzle in economics is why investment rates have been low over the last decades, despite falling interest rates and booming stock prices (Tambalotti et al. 2018). Falling interest rates imply that firms can obtain capital at a lower cost. According to textbook theory, a lower cost of capital should make firms willing to invest in projects offering lower returns, which in turn should have made firms invest in more projects overall.

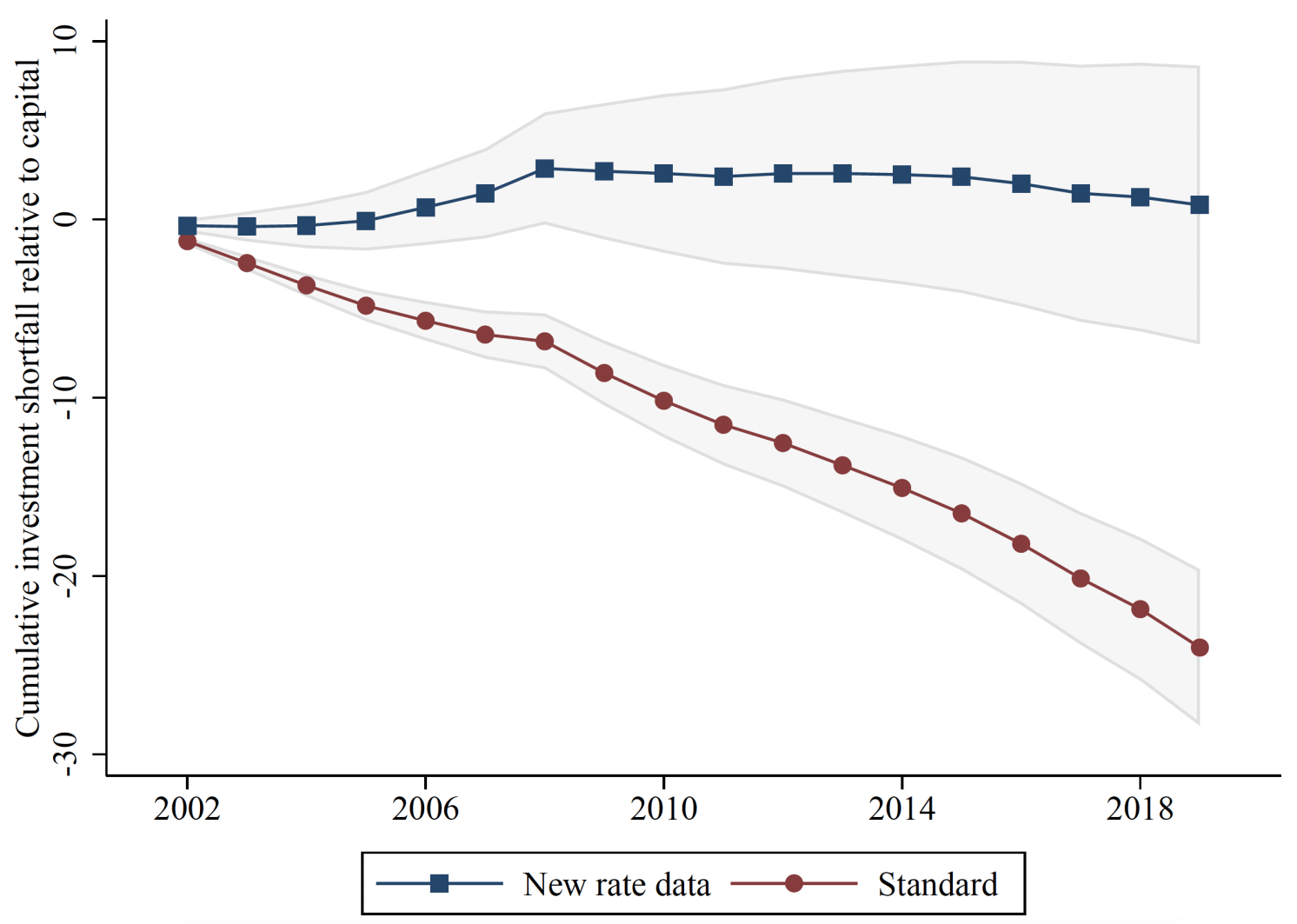

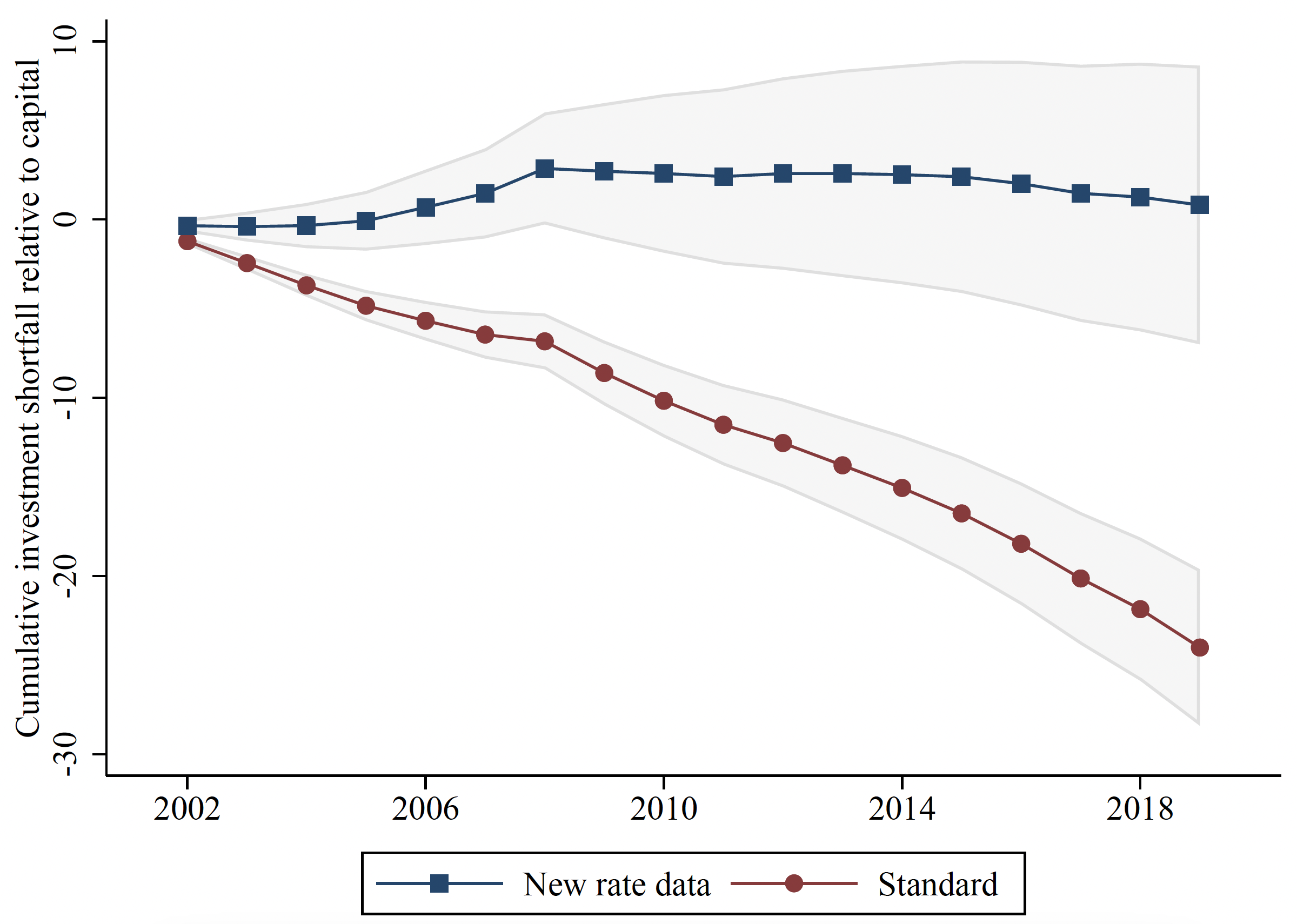

In a recent paper (Gormsen and Huber 2023), we show that firms do not behave as simply as in our textbooks. Specifically, firms do not always move their required returns on capital (their so-called discount rates) one-for-one with the cost of capital. Based on newly collected data, we show that firms know that their cost of capital has dropped substantially over the last two decades, but at the same time firms have hardly decreased their discount rates. Once we enrich standard models with the measured wedge between discount rates and the cost of capital, we account for a large part of the missing investment puzzle. As shown in Figure 1, there is little missing investment in the US if we use the newly measured discount rates, relative to those assumed in the standard model. The results point to an intriguingly simple explanation of the puzzle: firms do not automatically decrease their required returns with the cost of capital.

This insight matters beyond the missing investment puzzle. Most models in economics rely on the simple logic linking the cost of capital, discount rates, and investment. This is true for canonical economic models going back to at least Jorgensen, but also for the workhorse models dominating macroeconomics, finance, industrial organisation, and so on today (e.g. Inklaar et al. 2022). These models may have to be revised to capture the realities of firm behaviour. The results are also relevant for modern policymakers because they imply that government intervention through monetary policy or credit supply may not be as powerful as policymakers typically assume. Finally, and perhaps most important, there are implications for real welfare: growth slows when firms stop investing into new machines and technologies.

Figure 1 Newly measured discount rates account for missing investment in the US

Measuring firms’ discount rates and cost of capital

Our paper measures firms’ discount rates and cost of capital using corporate conference calls (also see Hassan et al. 2019). The majority of listed firms hold quarterly conference calls, during which managers inform financial analysts and investors about their firms’ operations and sometimes share their discount rates and cost of capital. Conference calls are held regularly, so analysts can compare reported discount rates to realised outcomes and calls often appear as evidence in securities lawsuits. These aspects incentivise managers to report accurate values.

We collect transcripts for conference calls between 2002 and 2021 and identify 74,000 paragraphs where managers discuss their discount rates or cost of capital. We read through each paragraph with a team of research assistants and manually extract relevant information. The product of this data collection is a global database of firms’ discount rates and cost of capital, matched to investment rates. The data contain roughly 2,500 firms across 20 countries. A unique feature of our data is that we can trace how discount rates and the cost of capital develop within firms over time.

Linking the cost of capital, discount rates, and investment

We use the new data to study the link between discount rates and the cost of capital. We document that changes in the cost of capital only modestly affect discount rates, in contrast to the stylised view. On average, a one percentage point increase in the cost of capital leads to a 0.3 percentage point increase in the discount rate. In addition, we find substantial variation in discount rates that is unrelated to the cost of capital. These results suggest that discount rates have ‘a life of their own’ beyond the cost of capital.

The weak relation between discount rates and the cost of capital gives rise to a time-varying wedge between discount rates and the cost of capital. We find that the average wedge in the US has increased by around 2.5 percentage points between 2002 and 2021, as the cost of capital has decreased while discount rates have remained more stable. This increase is large relative to typical movements in financial prices, for example, those due to secular interest rate trends and monetary policy (Krishnamurthy and Vissing-Jørgensen 2011, Rossi et al. 2022, Swanson 2011). An increase of this magnitude is likely to be important for our understanding of investment dynamics.

Indeed, we show that discount rate wedges are associated with investment fluctuations at the firm level. A one percentage point increase in the wedge lowers the investment rate by 0.9 points. This estimate is robust to controlling for firm and year fixed effects, Tobin’s Q, the cost of capital, analyst cash flow expectations, and other firm characteristics. The results suggest that discount rates and wedges accurately capture components of firms’ investment demand beyond the investment opportunities available to firms.

Implications for aggregate investment

As shown above in Figure 1, once we enrich a standard model with the average measured discount rate wedges, aggregate US investment is roughly in line with the predictions of the model. This finding helps to disentangle competing interpretations of the missing investment puzzle. Low investment relative to the cost of capital could imply that the marginal profitability of capital is low. Alternatively, it could imply that firms require returns above the financial cost of capital. It has so far been difficult to distinguish the two competing explanations because existing data do not measure how firms’ marginal profitability or required returns (i.e. discount rates) have changed over time. Our data reveal that the evolution of firms’ required returns is indeed large enough to account for much of the missing investment. In this sense, one may not need a large decrease in marginal profitability to explain the data. Relatedly, the results contribute to the debate on the falling labour share in national income, as growing discount rate wedges imply that the falling labour share is in part driven by rising rents accruing to firms.

Discount rate wedges also reduce the effect of the financial cost of capital on the investment rate by a factor of ten in a standard model. This finding may help to explain why macroeconomic models that abstract from discount rate wedges need to assume large adjustment costs to match the investment elasticities estimated in micro data (Gilchrist and Zakrajsek 2012, Zwick and Mahon 2017).

Drivers of discount rates

We also study why discount rate wedges vary across firms and over time. We consider three theories: (i) the interaction of market power with beliefs about value creation, (ii) idiosyncratic firm-level risk, and (iii) financial constraints. First, we systematically analyse manager statements on conference calls. We find that many managers believe that high discount rates raise shareholder value. High discount rates may signal profitability or managerial prudence, consistent with models where investors worry about overinvestment. While the benefits of wedges may accrue to firms independent of market power, we show that firms with market power are able to maintain wedges at a lower cost to their profitability. This implies that firms with more market power are more likely to choose high and steady discount rates over time, even when the cost of capital is falling. A second theory is that firms with irreversible assets postpone investments in the face of increased risk, which can lead riskier firms to use higher discount rates. And third, financial constraints may generate discount rate wedges. Using cross-sectional variation, we find that market power, risk, and financial constraints are all associated with higher discount rate wedges, consistent with the three theories.

We also analyse the drivers of time variation in discount rate wedges. We find a strong role for market power. In particular, firms with high market power (measured in 2000-2002) have kept their discount rates stable since 2002, despite the falling financial cost of capital. Firms with low market power have, in contrast, decreased their discount rates almost one-to-one with the financial cost of capital. This pattern is consistent with the idea that many managers are averse to lowering their discount rates and only do so in response to competitive pressures. Market power has therefore limited the extent to which the secular decline in the financial cost of capital has been incorporated into firms’ discount rates.

Source : VOXeu

.jpg")

")

")

.jpeg")

")

")

")

")

")

")