Economic growth is crucial for realising developmental goals, eradicating poverty, and ensuring the sustainability of debt burdens. Over the last two decades, the world has faced two large recessions, both of which have had a long-tail of dampened growth. This column uses a new dataset of potential growth measures to illustrate that potential growth has shown a steady and widespread decline over the last decade, with all the fundamental drivers of growth losing momentum over time. The authors also find that adverse shocks can have a persistent negative effect on potential growth.

Global growth has been slowing for a decade (Qureshi 2019). The slowdown was widespread: in 80% of advanced economies and 75% of emerging markets and developed economies (EMDEs), average annual growth was lower during 2011-21 than during 2000-10. A slowdown in total factor productivity (TFP) growth is also well-established, notwithstanding a sense of rapid technological change in areas such as digitisation or artificial intelligence (Anderton et al. 2023). Global population growth has slowed (Daly and Gedminas 2023). In addition, investment growth has weakened over the past decade in many advanced economies and EMDEs (World Bank 2023).

Was this slowdown simply the result of a series of shocks rocking the global economy or was it a reflection of weakening fundamentals? We examine this question in the context of potential growth – the maximum growth rate an economy can sustain over the longer term at full capacity and employment without igniting inflation.

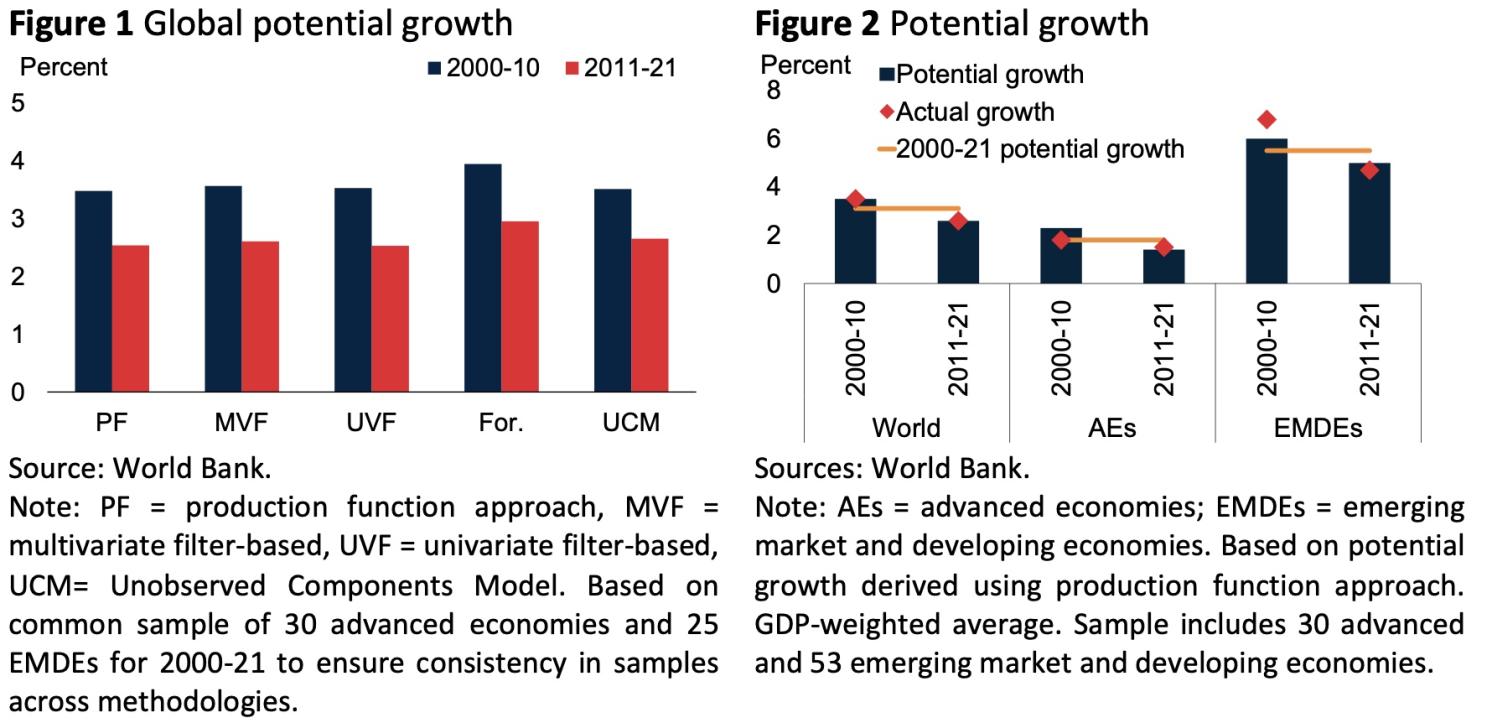

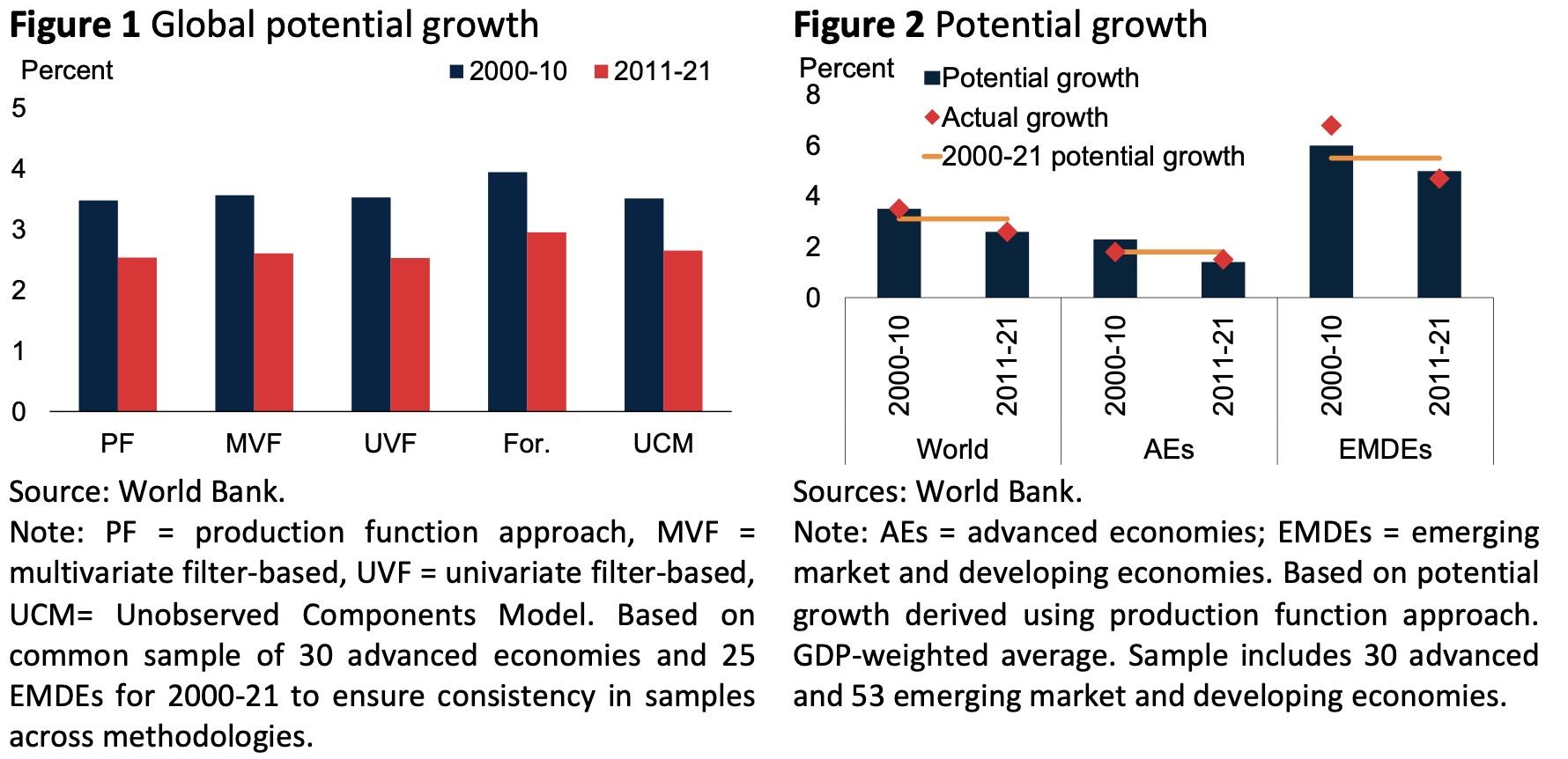

To answer this question, we develop the first comprehensive database of the nine most commonly used measures of potential growth for the largest available country sample—of up to 173 economies (37 advanced economies and 136 EMDEs)—over 1981-2021 (Kilic Celik et al. 2023). These measures comprise one based on the production function approach; five based on the application of univariate filters (Hodrick-Prescott, Baxter-King, Christiano-Fitzgerald, Butterworth, and Unobserved Components filters); one based on a multivariate Kalman filter; and two based on long-term growth forecasts. The database is publicly available on the World Bank website.

A basic comparison across potential growth measures shows that forecast-based estimates tend to be systematically higher than other estimates, and estimates based on univariate filtering techniques are lower. Estimates based on filtering techniques tend to be the most volatile and to track actual growth most closely, as expected. Estimates based on the production function approach tend to be the most stable and the least correlated with actual growth as they capture slow-moving drivers of potential growth.

Weakening potential growth

Regardless of the measure of choice, an internationally widespread decline in potential growth occurred between 2000-10 and 2011-21 that was driven by a multitude of factors. This is shown by all estimates of potential growth, globally and for the main country groups—advanced economies and EMDEs (Figure 1). Global potential growth, as estimated using the production function approach, fell to 2.6% a year on average during 2011-21 from 3.5% a year on average during 2000-10; advanced-economy potential growth fell to 1.4% a year on average during 2011-21, 0.8 percentage point below its 2000-10 average; and EMDE potential growth fell to 5.0& a year during 2011-21 from 6.0% a year during 2000-10 (Figure 2).

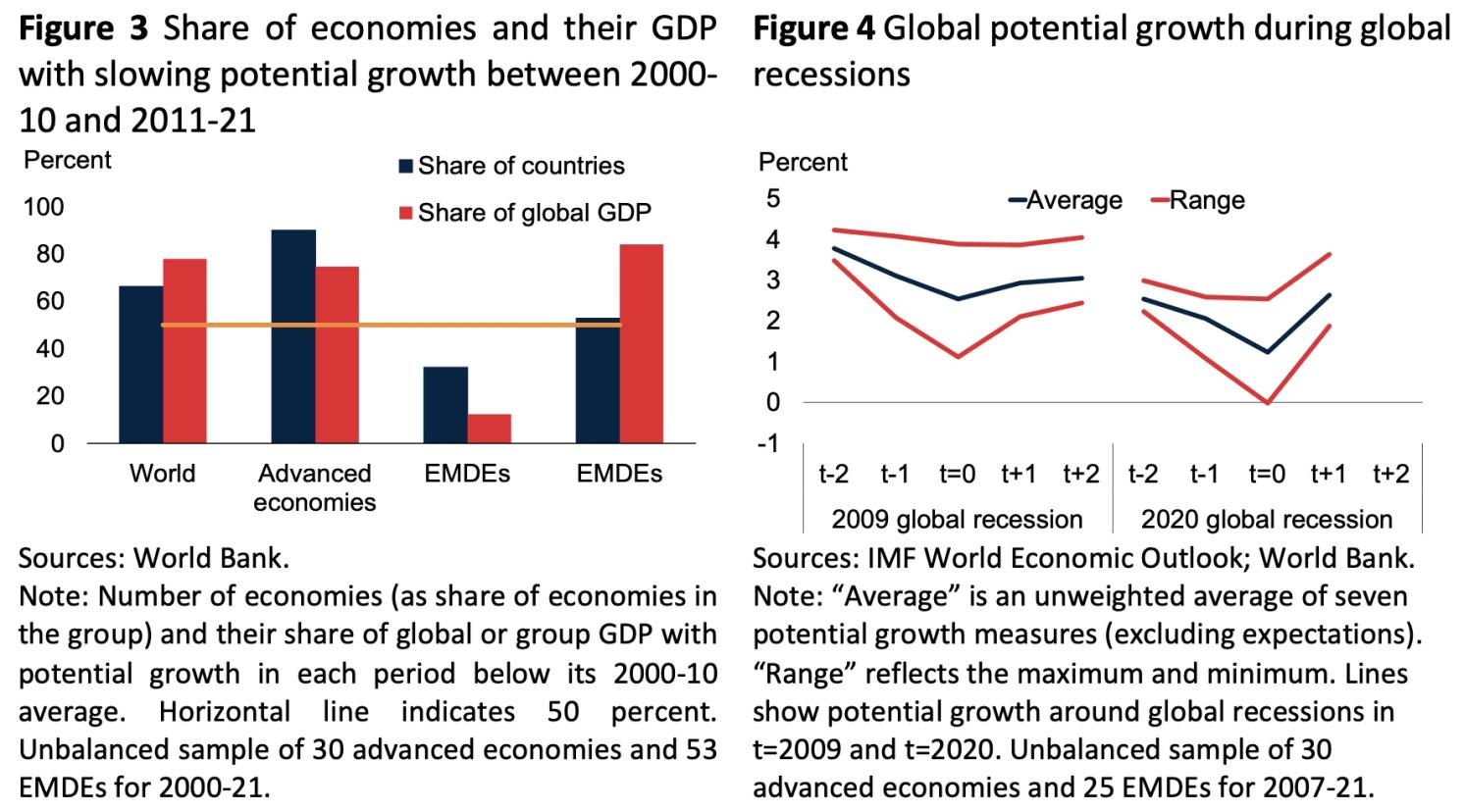

The decline in potential growth was highly synchronous across countries: during 2011-21, potential growth was below its 2000-10 average in 96% of advanced economies and 57% of EMDEs (Figure 3). This widespread decline reflected a multitude of factors. All the fundamental growth drivers faded in 2011-21: TFP growth slowed, investment weakened, and labour force growth declined.

Lasting damage from adverse shocks

In addition to weakening fundamental drivers of growth, a series of adverse shocks lowered potential growth, such as recessions, banking crises, and health crises. In local projections estimations, we show that each of these events had a persistent impact on potential growth. For example, recessions were associated with significant declines in potential growth even five years later.

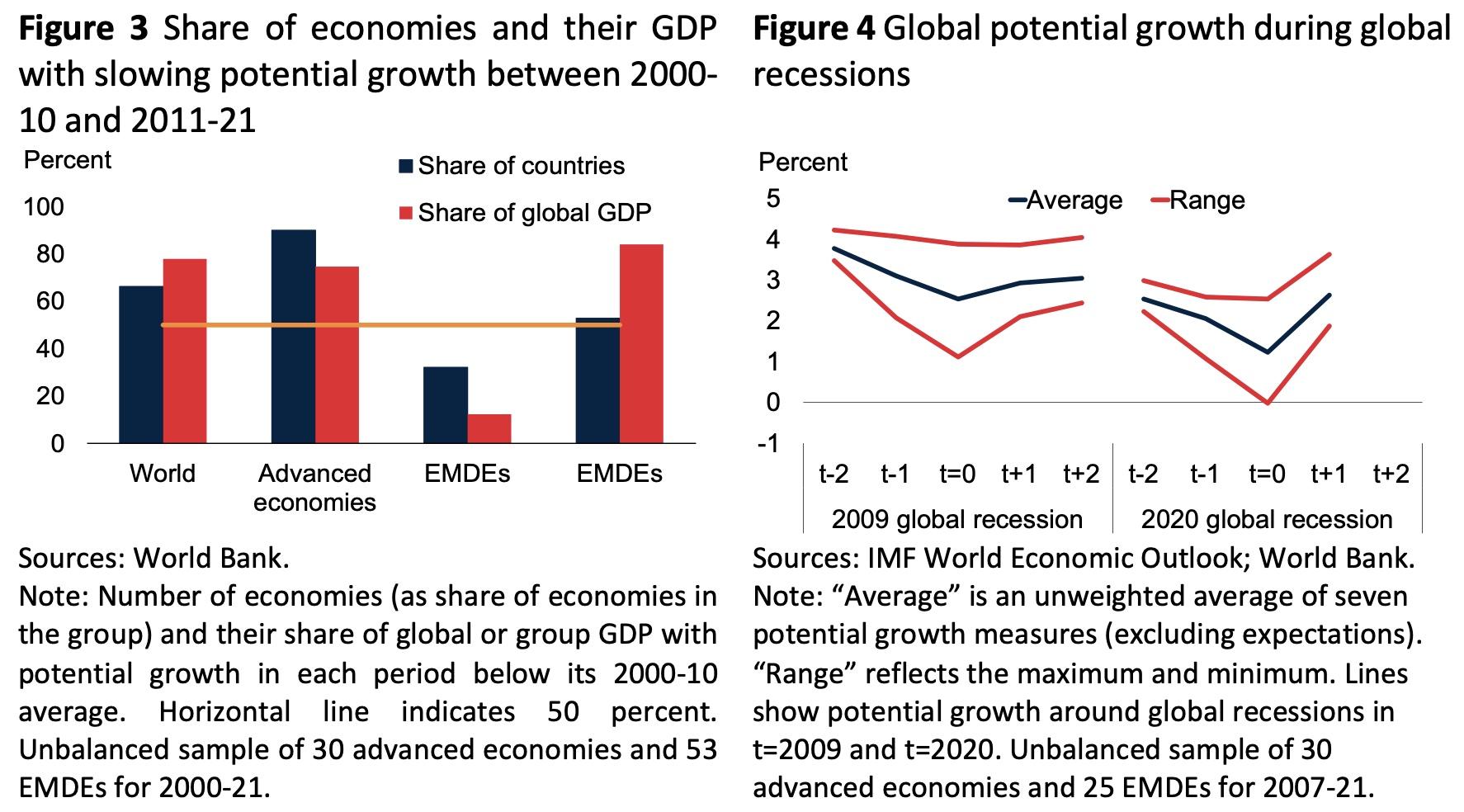

The 2000-21 period spans two global recessions—the 2009 recession triggered by the global financial crisis and the 2020 recession caused by the COVID-19 pandemic. These recessions disrupted fixed capital investment and caused widespread employment and output losses. In the case of the 2020 recession, disruptions of education systems caused by pandemic-induced reductions in social interaction also slowed down human capital accumulation. By the production function-based measure, global potential growth slowed by 1.2 percentage point in 2009 and 1.3 percentage point in 2020, compared to two years before the respective recessions (Figure 4).

Setbacks in progress towards development goals

Current trends suggest that the potential growth slowdown of the past decade will continue into the next decade (Kose and Ohnsorge 2023). Robust potential growth is the foundation of progress towards achieving development goals such as the eradication of poverty. The broad-based weakening of all the main drivers of growth and the lasting damage of the many recent crises therefore suggests further setbacks in such progress.

By reducing the government’s revenue-raising capacity, persistently lower potential growth also reduces debt sustainability and raises debt burdens. Against the backdrop of already record high government debt, this further constrains governments’ ability to pursue development goals.

In fact, the current better-than-anticipated growth in some economies may yet be revealed to reflect unsustainable demand booms that disguise weak potential growth only temporarily. If such booms are manifested in persistently high inflation and current account pressures, central banks may eventually face the challenge of restoring price and financial stability amid weak growth.

Source : voxeu

")

")

.jpeg")

")

")

")

")

")

")