In February 2023, a series of violent earthquakes struck southern and central Türkiye and northern and western Syria. This column provides early estimates of the likely economic impact of the earthquakes in Türkiye, drawing on the country’s experience with the 1999 earthquake as well as evidence from over 40 major earthquakes in 25 countries. Overall, the net impact on economic growth is likely to be less than 1 percentage point in 2023 as the boost from reconstruction may offset the initial negative impact within the same year.

In February 2023, a series of violent earthquakes struck southern and central Türkiye and northern and western Syria. A magnitude 7.8 earthquake and numerous aftershocks resulted in widespread damage and tens of thousands of fatalities in the region.

In this column, we provide early estimates of the likely effect of the 2023 February earthquake on Türkiye’s economy. We start by looking at the impact of major earthquakes in general, building on the experience of 25 economies and employing the synthetic control method. We then look at the impact of the 1999 earthquake in Türkiye and focus on similarities and differences between the 1999 and the 2023 earthquakes.

Economic impact of earthquakes: Earlier studies

Natural disasters such as earthquakes, floods, typhoons, and hurricanes can inflict serious damage on economies, destroying equipment, buildings and infrastructure and disrupting lives and production.

The exact magnitude of such effects on output is nevertheless widely debated. Some authors argue that earthquakes (and natural disasters in general) have significant negative effects on economic growth (Barro and i Martin 2003, Raddatz 2009). Recent work also notes potential spillovers propagating throughout the economy via trade linkages and supply chains (The et al. 2011, Ruta et al. 2021). Others, however, find mild or even positive effects on growth (Albala-Bertrand 1993, Barone and Mocetti 2014, Caselli and Malhotra 2004, Loayza et al. 2012, Porcelli and Trezzi 2019, Skidmore and Toya 2002).

The economic effects of earthquakes depend on the destruction they cause, the pre-existing economic conditions, and the ability of the economy to reallocate resources towards reconstruction (Hallegatte et al. 2022). Poorer economies, those with lower levels of government spending and weaker institutions are more likely to experience larger negative effects of earthquakes on growth (Cavallo et al. 2013, DuRose 2023, Lackner 2018, Noy 2009, Toya and Skidmore 2007). Effects are unequal within countries as well, with the poorest often being most exposed to the fallout from natural disasters (Colmer 2021).

Evidence from the synthetic control method

We examine the average impact of over 40 major earthquakes in 25 countries, using a ‘synthetic control’ method. This analysis draws on countries’ experience following earthquakes with at least 1,000 fatalities, including, for instance, earthquakes in Chile, Colombia, Haiti, India, Indonesia, Italy, and Japan. The synthetic control method compares the performance of economies that experienced earthquakes with that of similar economies which did not experience such natural disasters. Those comparators are chosen to be similar to the impacted economy in terms of GDP per capita, growth in the variable of interest (such as GDP or government spending), population, and population density.

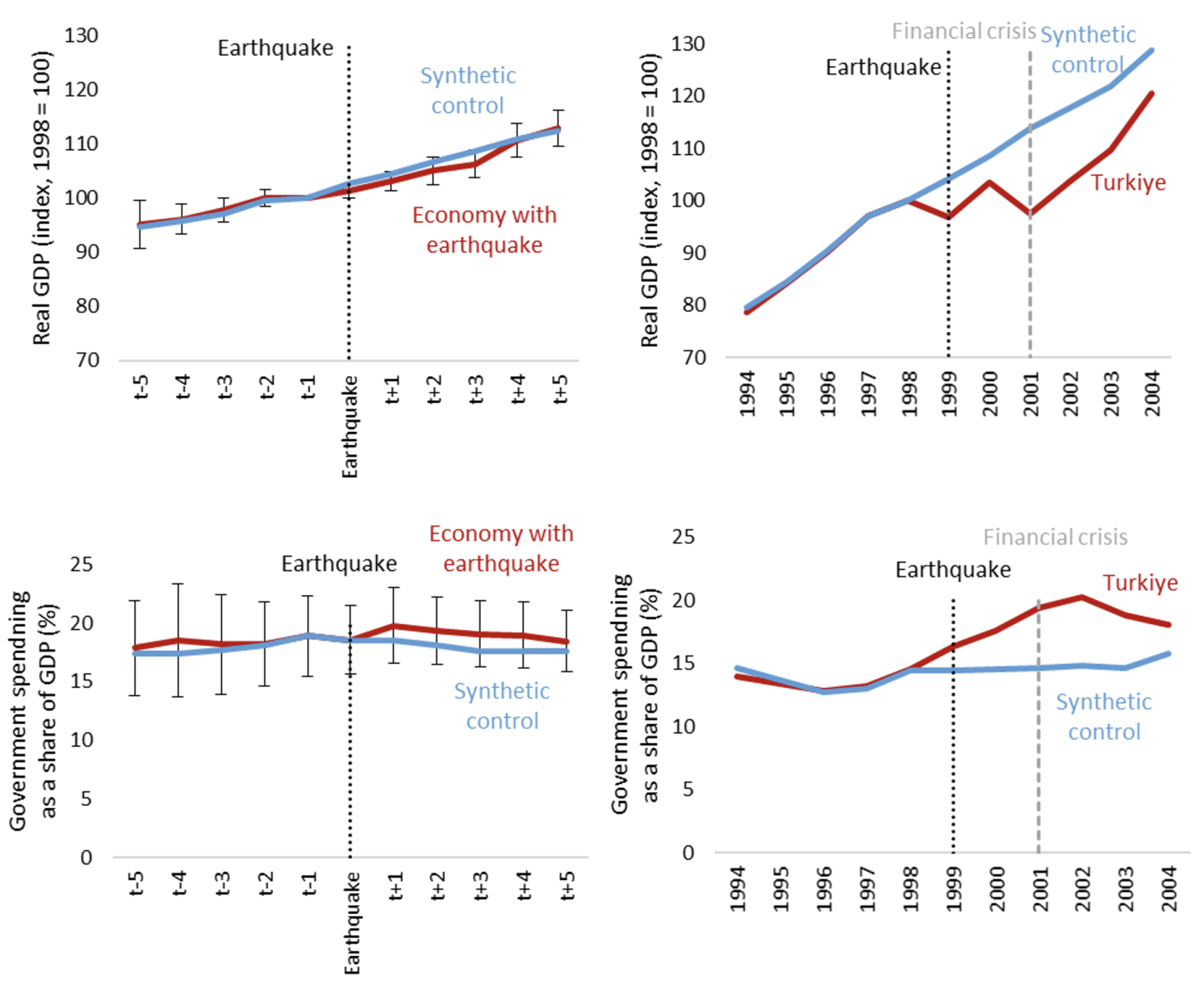

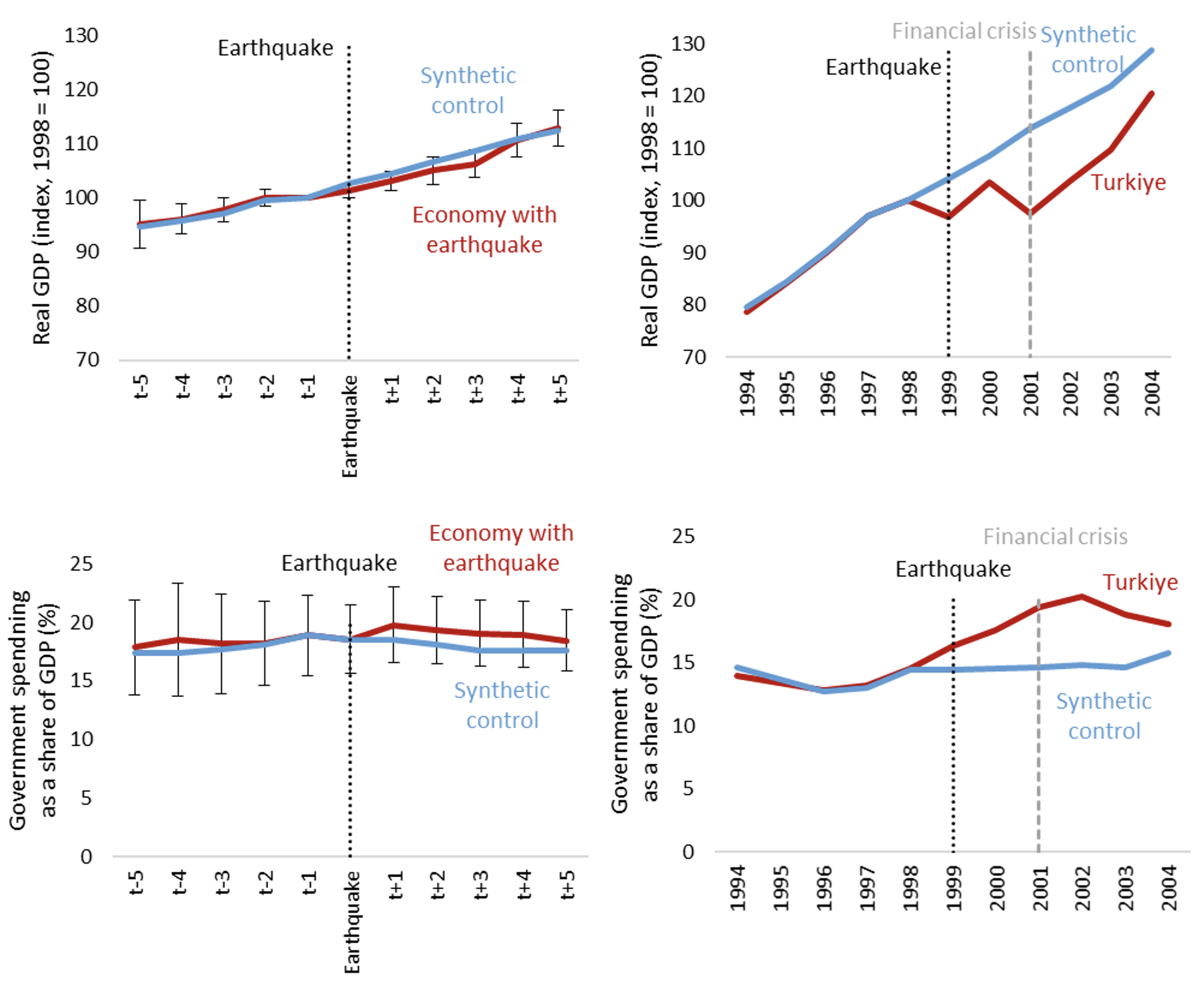

In the year after an earthquake, GDP is, on average, around 1 percentage point lower in economies affected by earthquakes than in otherwise similar economies, though the difference is not statistically significant, reflecting the large variation in growth outcomes in the sample (Figure 1, left panels). The impact is also short-lived as substantial reconstruction efforts boost GDP (including through increases in government spending). These estimates are consistent with earlier work examining the effects of natural disasters more generally using a similar methodology (Cavallo et al. 2013).

Figure 1 Estimates of the impact of earthquakes on GDP and government spending

Sources: Maddison Tables, Penn World Tables and authors’ calculations.

Notes: Synthetic control denotes a counterfactual growth path based on the evolution of the variable of interest in a weighted average of economies that were similar to the economy experiencing the earthquake before the earthquake in terms of GDP per capita, population, population density and growth of GDP or government spending. Left panels are based on a sample of 41 earthquakes for GDP and 23 earthquakes for government spending. 90% confidence intervals shown.

Importantly, GDP is a fairly narrow measure of the economic impact of a disaster. Value-added generated in a given year includes the cost of reconstruction but leaves aside the cost of damage to physical assets or people’s health. Those costs can be large. Current estimates of the total cost of rebuilding housing, productive capacity and infrastructure after the earthquake range between $25 billion and $50 billion, or up to 5% of GDP (e.g. JP Morgan, 2023).

Evidence from the 1999 earthquake in Türkiye

We can use the same method to construct a counterfactual for Türkiye’s economy after the 1999 earthquake. In practice, this analysis is confounded by Türkiye’s weak economic performance already in the first half of 1999, as the 1999 earthquake occurred after a period significant economic volatility. The economy contracted in 1994 in the face of growing macroeconomic imbalances. The introduction of a stabilisation programme helped foster a strong recovery, which saw growth averaging over 7.5% per year between 1995 and 1997. However, by 1998 the economy was slowing sharply, as external factors – notably, the financial crises in East Asia and Russia – hit confidence in emerging markets in general, and Türkiye in particular. By 1999, quarter-on-quarter growth was negative and an IMF report published in July 1999, the month before the earthquake, projected growth to be 0.5% that year (IMF 1999). A financial crisis broke out in 2001.

The right panels of Figure 1 show that GDP (in constant prices) dropped sharply in 1999, though rebounded in 2000, boosted by a sharp rise in government spending on reconstruction activities. Our results suggest that Türkiye’s growth performance over a two-year window was 4.6 percentage points weaker than could be expected based on the counterfactual.

This estimate does not take into account the weak performance observed in the first half of 1999. Netting out that effect (as the difference between the counterfactual growth rate of the synthetic control, at 4.2%, and the forecast for Türkiye made in July 1999) would yield an estimate of economic impact of around 0.9% of GDP. This negative impact is somewhat higher than estimates in other studies, which point to a loss of 0.5 to 1% of GDP in the year the earthquake occurred followed by a boost of 1.5 percentage points in the following year (Bibbee et al. 2000).

Geography of the 1999 earthquake

The 1999 earthquake in Türkiye was of a slightly lower magnitude than the one in 2023 but occurred in the country’s industrial heartland. The four regions worst affected by the 1999 earthquake (Kocaeli, Sakarya, Bolu and Yalova) contained only about 4% of the country’s population, but were directly responsible for around 7% of GDP and 14% of industrial value added. They had significant economic linkages with the rest of the country, including Istanbul (Türkiye’s largest city) and Bursa (the fourth largest city). As a result, there was significant damage to energy, transport, and communications infrastructure in the broader region (Bibbee et al. 2000). Together, the regions that experienced major disruptions because of the earthquake accounted for 35% of GDP and half of industrial output.

The initial economic slowdown reflected disrupted supply chains, loss of physical capital, labour force, and inventories as well as lower investment in the immediate aftermath of the earthquake. Many small businesses failed because they did not have earthquake insurance. This had a knock-on effect on the banking sector, which saw a sharp increase in non-performing loans in the run-up to the 2001 financial crisis (Bibbee et al. 2000). On the other hand, reconstruction activities boosted growth in 2000.

Comparing the economic importance of affected regions in 1999 and 2023

The 2023 earthquake in Türkiye differed from the 1999 earthquake in several important respects. The wider region hit by the 2023 February earthquakes in south-east Türkiye (Kahramanmaras, Gaziantep, Malatya, Diyarbakir, Kilis, Sanliurfa, Adiyaman, Hatay, Osmaniye, Adana) experienced substantial damage to pipelines, roads, airports, and electricity infrastructure, including a major fire in Iskenderun port, Türkiye’s largest. Economic linkages of the affected areas with the rest of the country are, however, more limited than in 1999. The affected areas are home to 15% of the country’s population but only contribute approximately 9% of GDP and 10% of industrial value added. Its contribution to agricultural value added is higher, at 15%, although interruptions to agricultural production are likely mitigated by the winter timing of the earthquake (Kelly and Kóczán 2023).

Unlike in 1999, the 2023 earthquake occurred early in the year. As a result, the reconstruction impact will largely materialise in the same calendar year, offsetting the negative impact of the earthquake-related disruptions on GDP to a significant extent. In addition, as earthquake insurance has become more widespread than it was in 1999, the impact on the banking sector is expected to be more limited.

Likely effects of the 2023 earthquakes

The economic impact of the earthquake will depend to a significant extent on the fiscal response. The authorities have fiscal space to fund various support measures as the level of public debt and the cost of servicing it remain modest relative to GDP. At the time of writing, the authorities have pledged more than 100 billion lira ($5 billion) towards the recovery effort and international support can further help to finance reconstruction.

Overall, drawing on the synthetic control analysis and the comparative analysis of the 1999 and 2023 earthquakes, the net the impact on growth is likely to be less than 1 percentage point of output in 2023, against the backdrop of a significant increase in government expenditure. These estimates are, however, subject to major uncertainty as recovery efforts continued at the time of writing.

Source : VOXEu

")

")

.jpeg")

")

")

")

")

")

")