Supply chain disruptions cause large macroeconomic adjustments and challenge the effectiveness of stabilisation policies. This column provides a new index of global supply chain disruption, presents a new model to identify the causal effect of global supply chain shocks on aggregate variables, and analyses the implications for the effectiveness of monetary policy. The authors document how supply chain shocks drove inflation during 2021 but, in 2022, traditional demand and supply shocks also played an important role in explaining inflation. Monetary policy is more effective in taming inflation after a global supply chain shock than in regular circumstances.

The world economy is organised around an intricate global supply chain. Any sudden disturbance to it, such as those triggered by war, geopolitical conflicts, or the recent COVID-19 pandemic, might have large consequences for output, inflation, and unemployment (Pandalai-Nayar et al. 2020, Alessandria et al. 2023, di Giovanni et al. 2023, Clayton et al. 2024). Furthermore, global supply chain shocks might also change the trade-offs faced by stabilisation policies (Benigno and Eggertsson 2023).

Measuring the causal effect of a global supply chain shock, and designing optimal policy responses to it, is challenging. Traditional metrics based on shipping costs or information from surveys are problematic since they reflect endogenous movements in the demand for goods or expectations that might be unrelated to supply chain disruptions. Besides, even after measuring the shock, researchers need a theoretical framework to formulate compelling identification assumptions required for causal analysis. Unfortunately, there is no standard theory that encompasses the simultaneous rise in spare productive capacity – resulting from disruptions to the supply chain – along with the shortage of goods and the scarcity of supply in the retail market that exerts upward pressure on prices.

In a recent paper (Bai et al. 2024), we address those issues by developing a new index of global supply-chain disturbances using real-time satellite data of container ships at major ports worldwide collected by the Automatic Identification System (AIS) mandated by the International Maritime Organization. Together with a novel theoretical model, we link spare productive capacity with shortages in retail supplies, as well as the responses of output and prices to supply chain disturbances. Using our new data and guided by our theory, we shed light on the causal effects of supply chain disruptions on aggregate outcomes and the implications for the effectiveness of monetary policy.

Measuring global supply chain disruptions

Building on established results in maritime economics (Transportation Research Board Executive Committee 2006), we measure global supply chain disruptions by congestion at ports. Since container shipping accounts for approximately 60% of the value of seaborne trade, even minor congestion, as limited to one or two days delay, cause significant disruption (UNCTAD 2019).

The organisation of container shipping, based on fixed routes and predetermined timetables regulated by long-term contracts, 1 allows us to achieve a powerful identification of supply chain disturbances. Since the terms and timing of container ships are fixed several months in advance and independent from standard demand and supply forces, any substantial delay – and the resulting congestion at ports – is evidence of genuine shocks to the supply chain. Thus, our new measure provides an accurate measurement of supply-chain disturbances.

We quantify congestion at ports by developing a machine-learning algorithm that processes the location, speed, and heading of containers at ports. This algorithm enables us to accurately quantify the congestion and delays at different ports around the globe and construct the average congestion rate (ACR) index, our new metric for recording the scale of global supply chain disruptions.

Figure 1 shows the ACR index for the period January 2017-2024. Despite the outset of the COVID-19 pandemic in February 2020, the delays of container ships at ports increased notably only in the second half of 2020. The ACR index increased from 25% to 37% approximately, and the average duration of these delays escalated from 5.5 to 13.5 hours. Thus, contrary to several commentaries, supply chain disturbances materialised well after the outset of the COVID-19 pandemic.

Figure 1 ACR index of global supply chain disruptions

A model of congestion and spare capacity

Next, we develop a new model to study the causal effect of global supply chain disturbances and their implications for monetary policy. Our model is based on the disequilibrium models of the 1970s (Barro and Grossman 1971) but with a microfounded approach that considers the frictions between buyers and sellers of goods (Michaillat and Saez 2015, Ghassibe and Zanetti 2022). This framework helps to identify the causal effect of supply chain shocks in the data.

Our model demonstrates that supply chain disturbances, generated by either an increase in transportation costs or a decrease in the meetings between buyers and sellers, raise the spare capacity in the production markets while increasing the scarcity of goods, and therefore the prices in the retail market. Disruptions to the supply chain result in negative co-movements between output and the price of goods, like supply shocks. However, they increase spare capacity for producers due to the reduction in the shipment of goods, whereas traditional supply shocks decrease spare capacity. Hence, an increase in spare capacity, coupled with a rise in prices and a decline in output, identifies the causal effect of supply chain disturbances.

What drove US inflation since 2020?

We use our new identification scheme to constrain the responses of key macroeconomic variables to a supply-chain disturbance in a structural vector autoregression (SVAR) estimated using our ACR index and US data. Our findings reveal an immediate and significant effect of supply chain disruptions, leading to a notable decline in real GDP and an increase in unemployment and inflation. 2

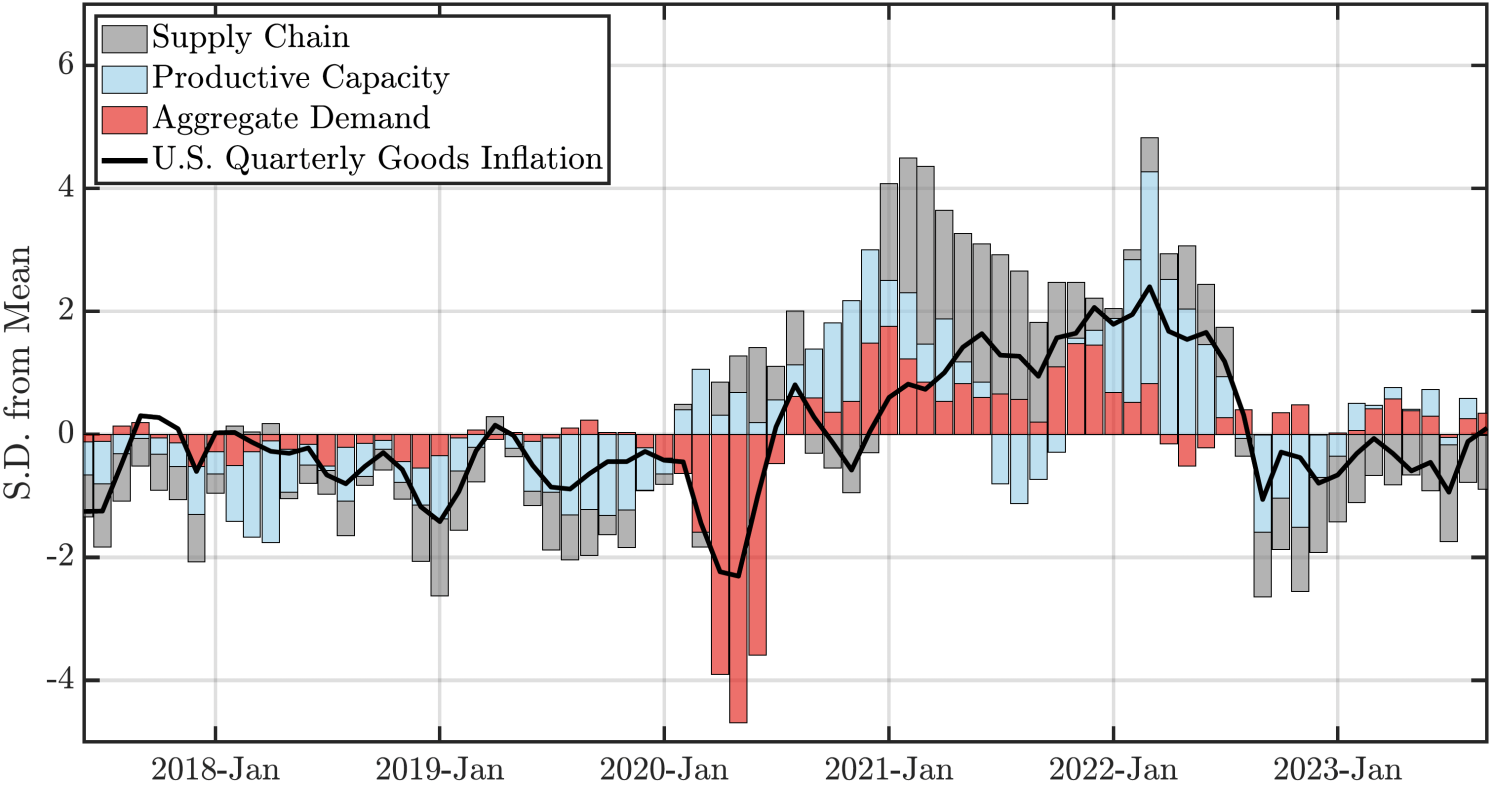

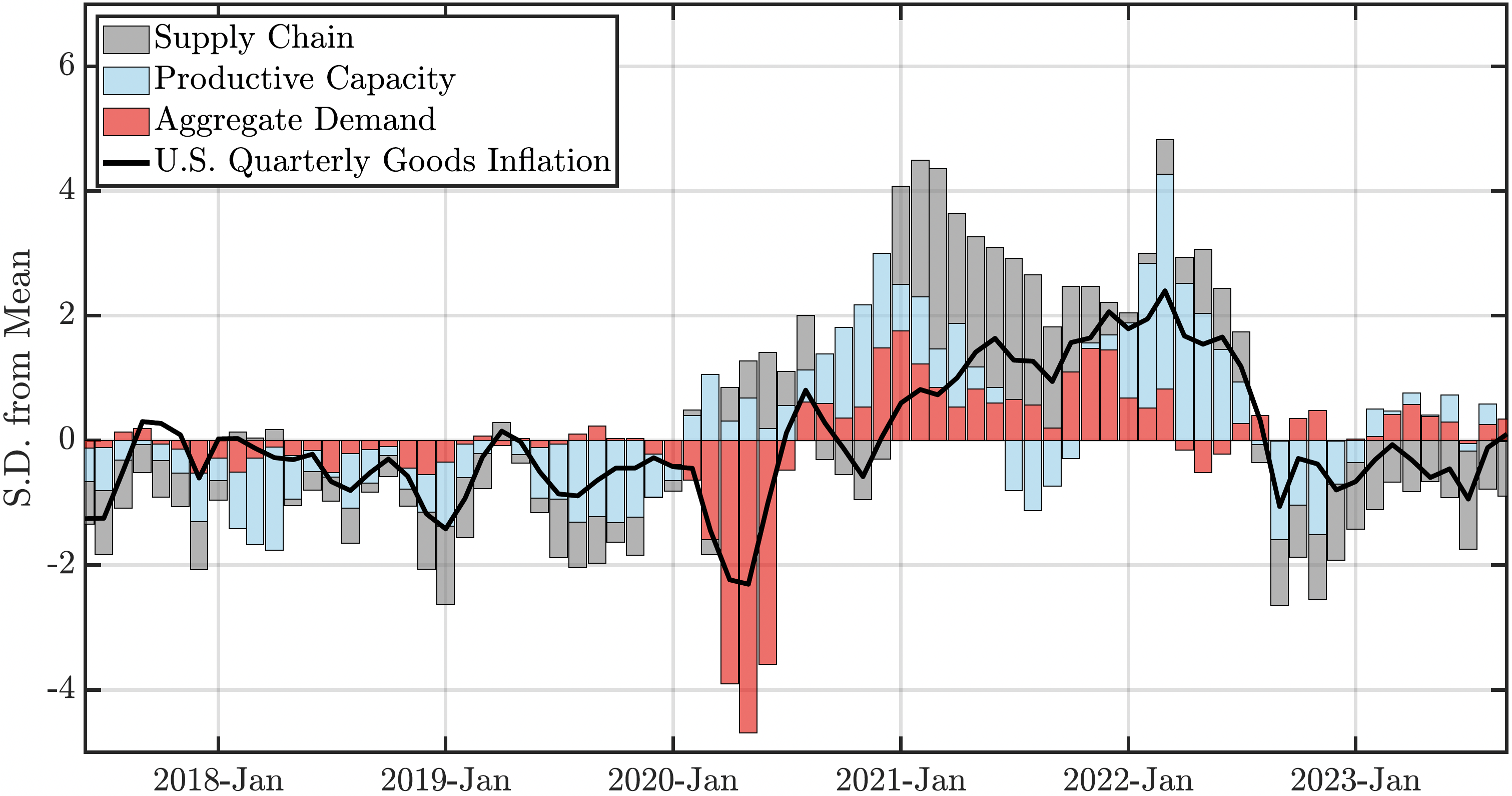

We decompose the separate contributions of the distinct shocks to the productive capacity, aggregate demand, and the supply chain to inflation. Figure 2 shows the result of the exercise. Before 2020, supply chain disturbances had a negative impact on inflation, highlighting the effectiveness of strategic supply chain improvements and infrastructure upgrades at the port of Los Angeles that eased inflationary pressures. The early 2020 drop in inflation at the onset of the COVID-19 recession primarily resulted from a sharp fall in aggregate demand, likely linked to mobility restrictions and increased uncertainty at the early phase of the pandemic. On the other hand, supply chain disturbances were the main drivers of inflation in 2021. By early 2022, shocks to the productive capacity and aggregate supply primarily contributed to the surge in inflation, likely related to the shift in preferences of workers towards flexible work arrangements and the increase of unemployment benefits brought by the CARES Act. Notably, aggregate demand played a minor role in the movements of inflation post-2022, suggesting that monetary and fiscal policies were not excessively expansionary. From mid-2022 onward, a combination of weakening demand, strengthening productive capacity, and recovering supply chains contributed to lower inflation.

Figure 2 Drivers of US goods inflation

Notes: The solid line represents the standardised US goods inflation rate, calculated as the quarter-on-quarter growth of the PCE goods price index. The shaded bars depict the corresponding standardized cumulative historical contributions of shocks to aggregate demand, productive capacity, and the supply chain to goods inflation.

A more aggressive, yet less contractionary, monetary policy tightening

Finally, our model allows us to study the implications for the effectiveness of monetary policy. Our theory shows that supply chain disruptions generate stagflation while increasing producers’ spare capacity, generating scarcity of goods in the retail market, and increasing prices. In this situation, prices become highly sensitive to changes in demand, while output remains relatively inelastic. In other words, disruptions to the supply chain enhance the effectiveness of contractionary monetary policy in taming inflation while reducing the sensitivity of output to the policy.

We empirically test this theoretical prediction using a threshold vector autoregression model. We find that an exogenous tightening of monetary policy leads to a significantly larger and more persistent decline in inflation for a given decrease in output during periods of supply chain disruptions. Our results support a more aggressive, yet less contractionary, approach to tightening monetary policy in response to the elevated inflation consequent to supply chain disturbances.

Our study provides an initial step toward a full understanding of the macroeconomic consequences and policy responses to supply chain disturbances, which will remain critical to the modern economy, which revolves around an intricate global supply chain.

Source : VOXeu

")

")

.jpeg")

")

")

")

")

")

")