Many commentators argue that quantitative easing played a significant role in the post-pandemic rise in inflation across advanced economies. Would the inflation consequences have been different if central banks had used conventional monetary policy instead? This column uses eight measures of quantitative easing to examine its inflation effects relative to those of conventional monetary for the euro area, the UK, and the US. The findings suggest that quantitative easing has a stronger inflation effect than conventional monetary policy. This has important implications for the debate on how much conventional monetary policy tightening is required to return pandemic-era, quantitative easing-generated inflation back to target.

Many commentators argue that quantitative easing (QE) had a significant role to play in the post-pandemic rise in inflation across advanced economies. However, central banks had to ease policy in response to the demand weakness during the pandemic. Would the inflation consequences have been different if central banks had used conventional monetary policy instead?

Although central banks will likely continue to use QE and short-term interest rates as complementary policy tools, the relative inflation effects of these two tools have only been examined in a few studies for the US. The conclusion depends on the study and the method used. Several of these studies find that conventional monetary policy and QE have roughly the same effect on inflation. Wu and Xia (2016) use a shadow rate approach and conclude that conventional and unconventional monetary policy have a similar effect on inflation. Bu et al. (2022) develop an alternative measure, which captures both unconventional and conventional monetary policy shocks, and come to the same conclusion for the US. Swanson (2023) uses factors extracted from the yield curve to find that conventional monetary policy had a bigger impact on inflation than QE. Aruoba et al. (2022) rely on a three-variable SVAR model with an occasionally binding constraint and find that inflation shows a stronger reaction to unconventional monetary policy relative to conventional policy, but upon impact only. Mavroides (2021) uses a similar approach but concludes that unconventional monetary policy is less effective than conventional monetary policy. Overall, these studies come to different conclusions on whether QE has a great impact on inflation than conventional monetary policy or not.

Unlike for conventional monetary policy, the ideal way of measuring and modelling unconventional monetary policy in a vector autoregression (VAR) continues to be debated in the literature. Previous work has proposed at least eight different ways of measuring QE in a VAR model. These include the long-term interest rate (Baumeister and Benati 2013), the central bank balance sheet (Gambacorta, Hofmann and Peersman, 2014), cumulated asset purchase announcements (Weale and Wieladek, 2016), different shadow rate series (Wu and Xia 2016, Krippner 2015), the two-year yield (Swanson and Williams 2014), high-frequency shock series (Gertler and Karadi, 2015), and monetary policy shocks extracted from across the yield with the Fama-Macbeth (1973) approach (Bu et al. 2021). None of these measures of QE is flawless, but they are likely informative collectively.

In my recent paper (Wieladek 2023), I use all of these eight measures of QE to examine the inflation effects of QE relative to those of conventional monetary for the euro area, the UK, and the US. I also study the differences in the transmission mechanisms of these policies. This holistic approach helps to better understand whether QE has greater inflation effects than conventional monetary policy, irrespective of how the policy is measured and which countries are examined. In a sense, the conclusions should be therefore more general than previous studies and less dependent on a specific methodology.

Unlike previous studies, I explore possible differences in transmission mechanisms between these two policies. Aside from the portfolio balance channel, conventional monetary policy and QE affect the economy through similar channels which are designed to ease or tighten financial conditions in response to macroeconomic shocks. The Neo-Keynesian model puts emphasis on the power of monetary policy to affect inflation expectations. The monetarist approach argues that monetary policy affects inflation via the broad money supply. Finally, exchange rate theories rely on both short-term interest rates and broad monetary aggregates as key determinants.

I estimate VAR models using these eight different measures of QE on pre-pandemic QE samples for the euro area, the UK, and the US. The sample therefore does not cover the most recent rounds of QE during the pandemic. This is by design. Including the pandemic-era data risks econometric distortions due to the very large movements in GDP data during the pandemic. Any estimates of QE inflation effects estimated on the post-pandemic sample would be significantly affected by the surge in inflation. This could be a function of the economic environment as opposed to the effects of the QE policy per se.

Estimates from these eight QE VAR models are compared to estimates from conventional monetary policy VAR models, estimated on the pre-global financial crisis decade. Credibly comparing effects in response to the same size monetary policy shock is easier in some cases than in others. A 100 basis point decline in the shadow rate during the QE period can be directly compared to a 100 basis point decline in the conventional policy rate. High-frequency shocks and the Bu et al. (2021) measure are available for both the QE and conventional monetary policy time periods. Inflation effects of QE and conventional policy shocks of the same size can therefore be compared by estimating the models on the QE and conventional monetary policy sample separately. Results from approaches which rely on asset purchases, balance sheets and long-term rates as QE measures are compared to conventional monetary policy by comparing effects in responses to the same size reaction in the long-term interest rate.

The results from this exercise suggest that the inflation effects of QE are two to four times larger than those of conventional monetary policy in the UK and the US. These are statistically significant in at least five out of the eight plausible specifications. But I do not find a difference in effects that is statistically significant for the euro area.

Adding different variables one at a time to these VAR models allows me to examine which difference in the transmission mechanism is responsible for the difference in results. I explore many different variables that previous work has used to tease out the transmission mechanism of monetary policy. For many of these variables, such as output, unemployment, financial variables, wages, or producer price indices, there is no evidence that the effects of conventional monetary policy are different to those of QE. However, I find that QE is associated with a stronger response of the exchange rate, broad monetary aggregates and household inflation expectations. It is plausible that household take a monetarist view of QE and believe that the ‘printing of money’ associated with the policy leads to stronger inflation. This difference in the expectations channel of monetary policy could be behind the results documented in my paper.

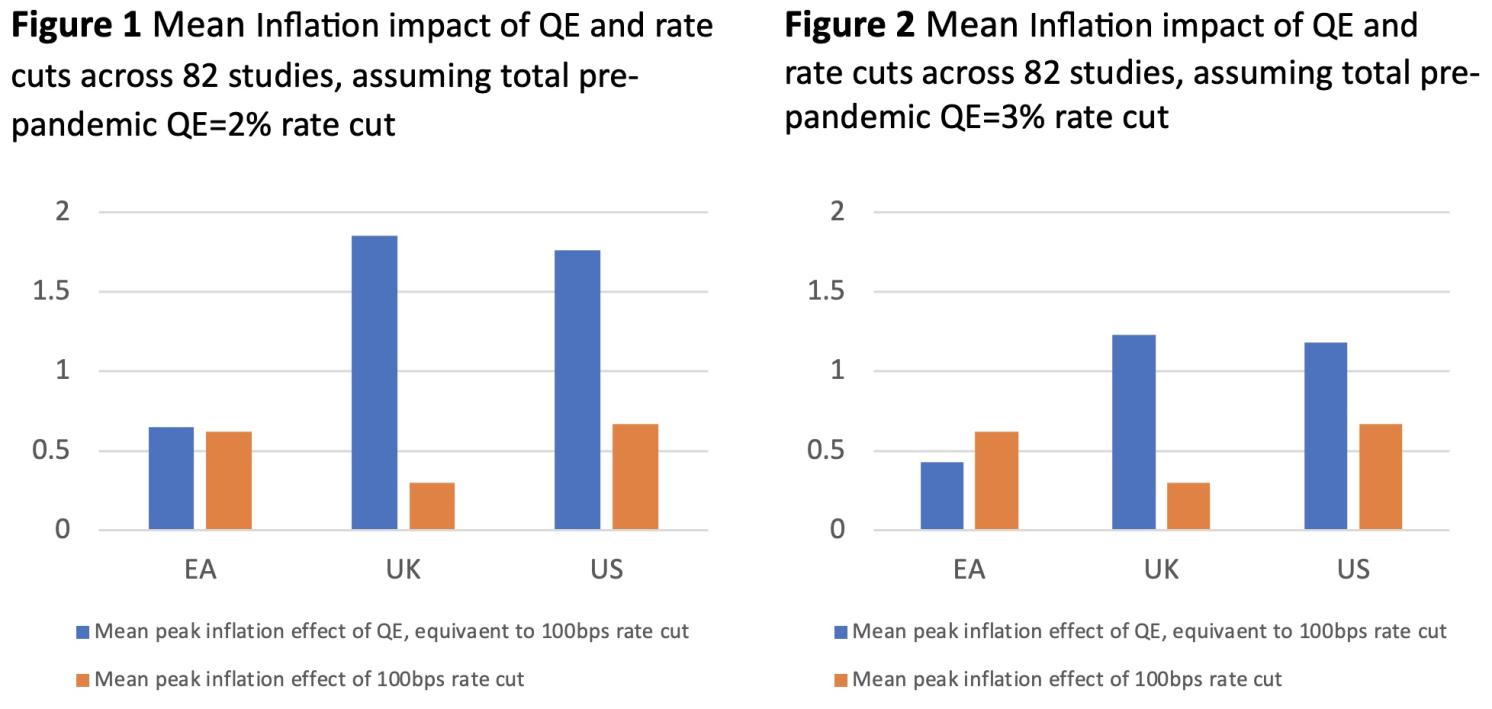

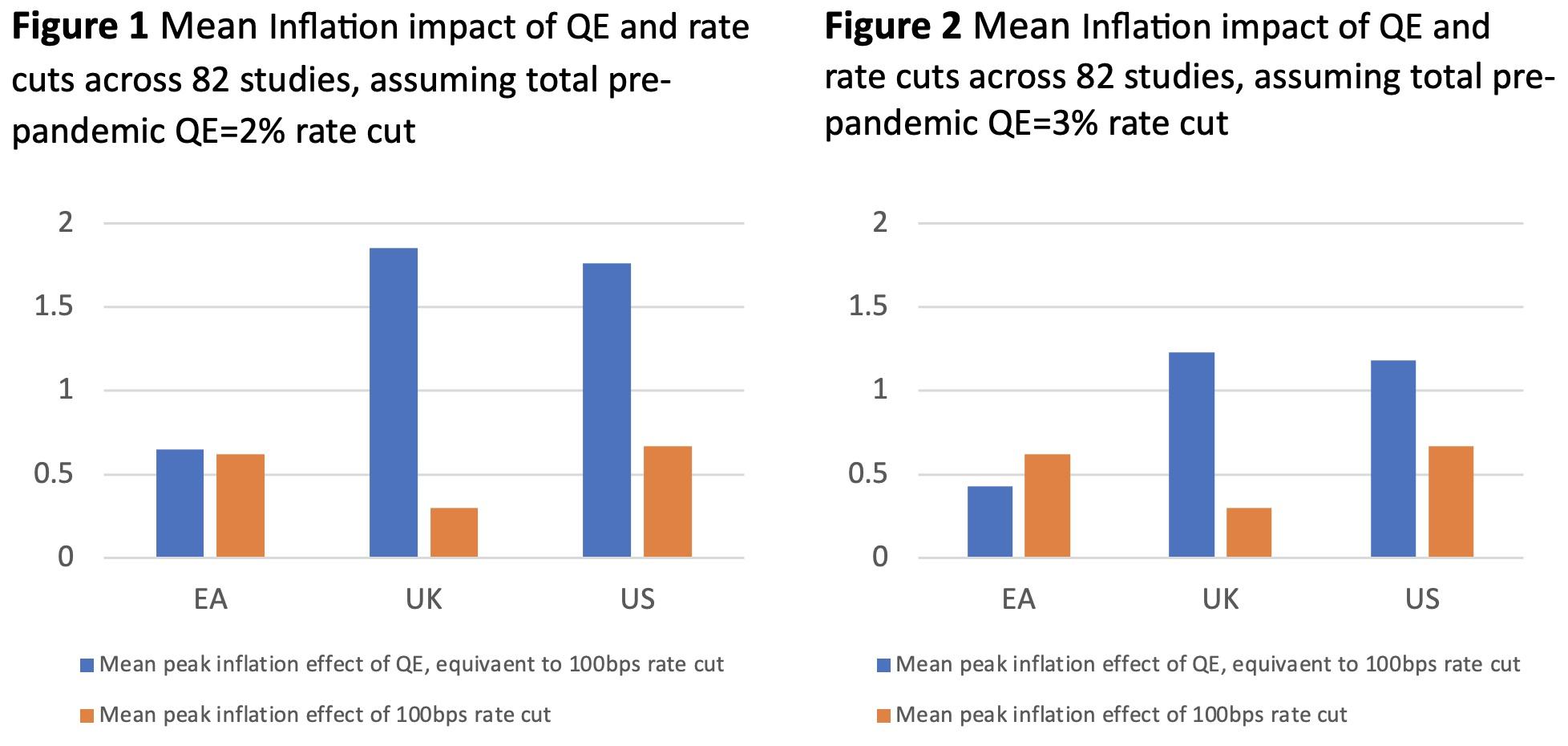

The result that QE has a stronger effect on inflation than conventional monetary policy could just be specific to this study. To investigate whether these results are more general, I undertake a meta-analysis of 82 previous VAR studies of conventional monetary policy and QE for the euro area, the UK, and the US. The conventional monetary policy inflation effects are taken from the database presented in Rusnak et al. (2013), while the QE effects are from Fabo et al. (2021). The most challenging aspect is ensuring that QE and conventional monetary policy inflation effects are compared in response to the same size monetary policy shock. For the US, Gertler and Karadi (2011, 2013) and Sims and Wu (2020) both argue that the pre-pandemic QE in the US was equivalent to a conventional monetary policy easing of 200bps. In his last speech as Bank of England Governor, Mark Carney indicated that £360 billion of QE was roughly equivalent to 300 basis points of conventional monetary policy easing. These estimates allow me to convert the inflation effects of QE into conventional monetary policy space. In total, I examine estimates from 82 previous studies of QE and conventional monetary policy. Testing for a difference in means through t-test shows that the inflation effects of QE are two to four times higher than those of conventional monetary policy in the UK and US, but not the euro area (see Figures 1 and 2). The main finding in my paper is therefore also present in all previous studies of this subject.

In conclusion, I present systematic evidence that QE has a stronger inflation effect than conventional monetary policy across countries and many different measures of QE. This has important implications for the latest policy debate on how much conventional monetary policy tightening is required to return pandemic-era QE-generated inflation back to target. Public policy should never rely on one academic study alone, although the meta-analysis suggests that the results of this study are also present in 82 previous conventional monetary policy and QE VAR studies. This is why future research may want to revisit the results presented here with alternative econometric frameworks. A second interesting question is why the euro area results are so different from those for the UK and the US. One plausible hypothesis is that the financial distress during which UK and US QE were implemented amplified the effects of those policies. Pre-pandemic euro area QE, on the other hand, was implemented when the financial system was relatively stable. Exploring whether this difference could be responsible for the results presented here remains an interesting avenue for future research.

source : Voxeu

")

")

.jpeg")

")

")

")

")

")

")