The growth of digital wallets and popular ‘buy now, pay later’ options raises concerns about social welfare and policy. This column uses data from a world-leading Chinese provider to document that ‘buy now, pay later’ dominates e-wallet transactions and expands FinTech credit to underserved consumers. It also substantially boosts consumer spending, but users – especially those relying on e-wallets as their sole credit source – carefully moderate borrowing when incurring interest charges. These findings can help policymakers tackle the challenges arising from the expansion of digital wallets and ‘buy now, pay later’.

The past decade has witnessed a phenomenal rise of digital wallets, exemplified by the worldwide usage of PayPal, Apple Pay, the relaunched Google Pay, and super apps such as WeChat Pay and Alipay. The COVID-19 pandemic further accelerated their adoption globally. Such e-wallets provide not only a conduit to external bank accounts but also internal payment options, including the ever-popular ‘buy now, pay later’ (BNPL) characterised as a short-term FinTech credit allowing consumers to defer payments interest-free into one or a few instalments. While economists agree that the shift from cash and bank cards toward e-wallets exerts a profound influence on the real economy (Agarwal et al. 2020, 2022), little is known about how various payment options interact and compete within e-wallets and how BNPL affects consumer credit provision and spending behaviour. When users choose e-wallets’ internal payment options, e-wallets may circumvent banks, thus cutting banks off from valuable informational synergy between FinTech lending and cashless payments (Ghosh et al. 2022). This, in theory, can have an ambiguous effect on social welfare (Berg et al. 2018, Calzolari et al. 2018, Parlour et al. 2022). Moreover, it is unclear whether BNPL leads to excessive spending and indebtedness (Ponce et al. 2017, Agarwal et al. 2020, Dupas et al. 2022).

We aim to bridge the knowledge gap by opening the black box of e-wallets that contain multiple payment options using unique data from a representative e-wallet provider based in China, which is also a global leader in the sector (Bian et al. 2023). The e-wallet data sample covers 550,000 online and 550,000 on-site transactions randomly drawn from all transactions through the e-wallet in June 2020. This e-wallet with the function of BNPL was born within a large self-contained e-commerce ecosystem in China, with a userbase well-representing the population aged 16-60 and a business model that e-wallet and BNPL providers around the globe are converging to (CFPB 2022).

Buy now, pay later as the new cash

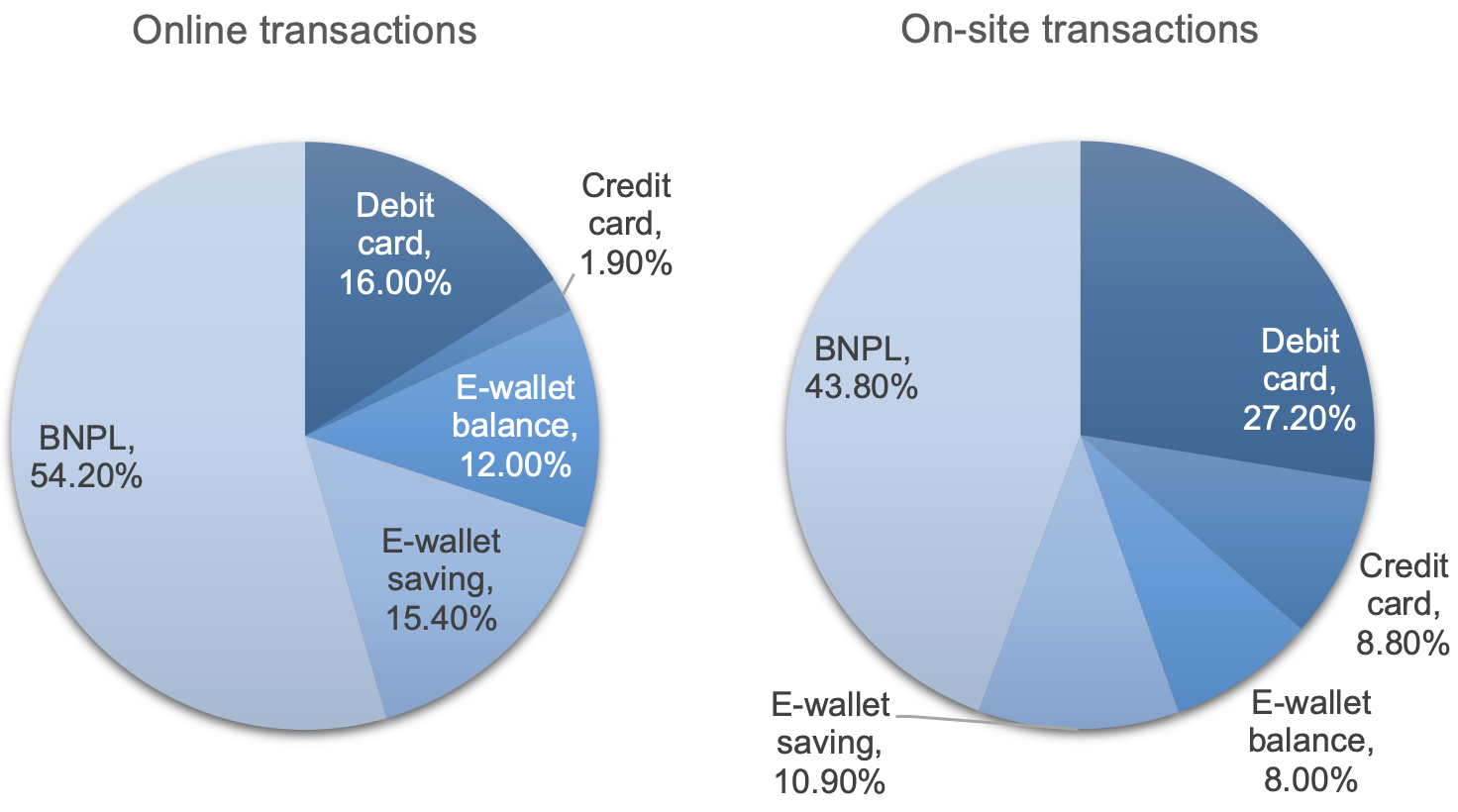

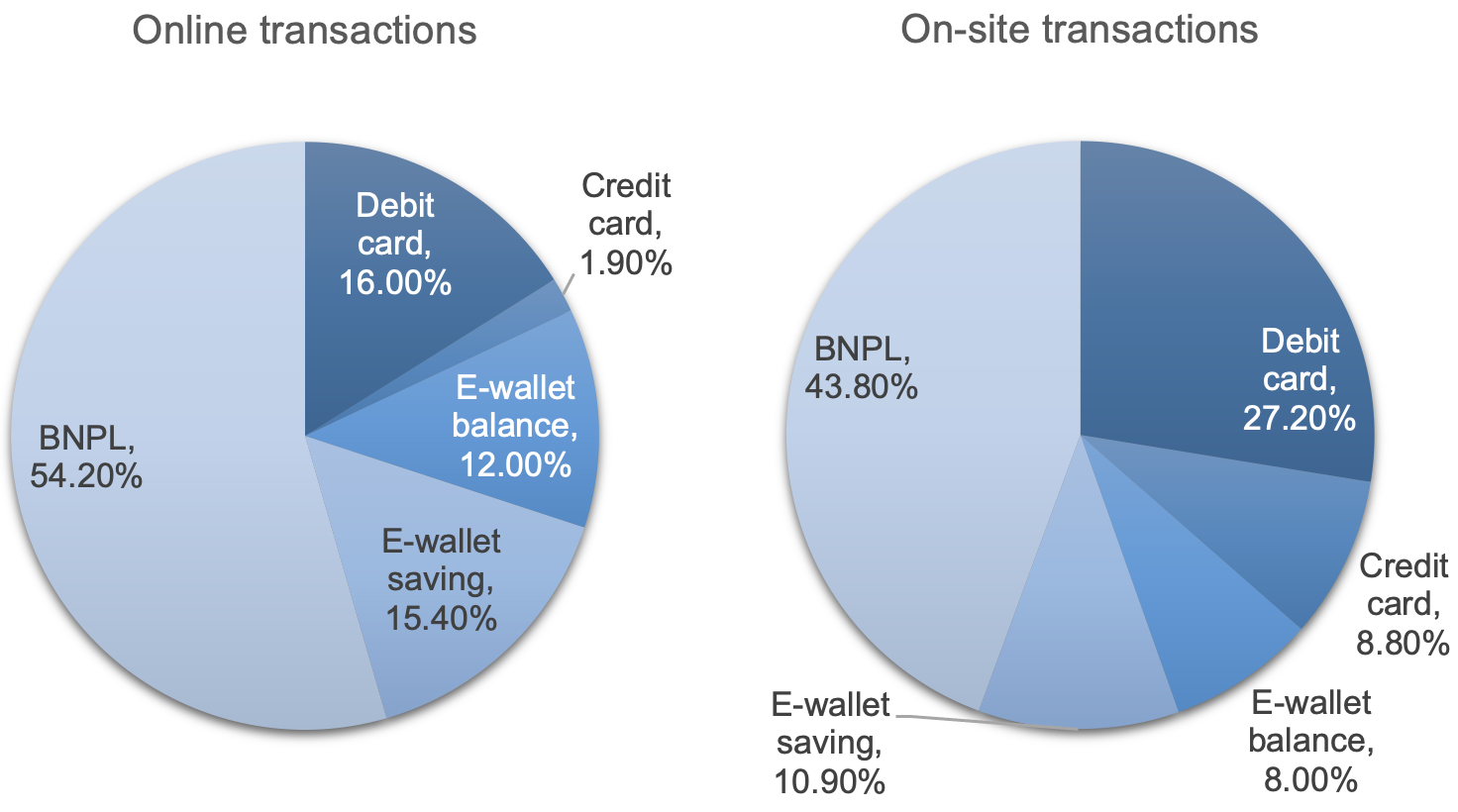

We first summarise the stylised facts regarding the distribution of e-wallet payment options. As shown in Figure 1, internal payment options – particularly BNPL – have become consumers’ predominant way to pay, accounting for more than half of all transactions in our sample, whereas the most popular external option – linked debit cards – accounts for less than one-third. As internal options dominate in e-wallet transactions, the popularity of e-wallets could disrupt traditional banks’ access to payment data (Ghosh et al. 2022). Given how important payment information and digital footprints are in lending (Berg et al. 2022), it is understandable that central banks around the world are looking into developing their own electronic payment systems (EPSs) or digital currencies to compete for payment flows with FinTech giants (Boar and Wehrli 2021).

Figure 1 Payment options in the e-wallet

We find that consumer access to e-wallet credit crowds out the usage of other payment options in both on-site and online transactions. Somewhat counterintuitively, we also find that dual-access users use e-wallet credit and credit cards in different payment scenarios, with e-wallet credit for daily, small-value transactions and credit cards for big-ticket purchases. We posit that BNPL is now the most popular payment choice in e-wallet transactions and hence serves as the new digital cash in the transition to cashless societies.

Buy now, pay later and financial inclusion

We then investigate if e-wallet credit (i.e. BNPL) expands credit provision to those with no prior credit access. We document a substantial expansion at the extensive margin. Specifically, 84.14% and 78.38% of on-site and online consumers without credit cards, respectively, can now access e-wallet credit. Moreover, 43.54% of on-site merchants who previously did not accept credit cards now accept e-wallet credit. Additionally, 44.37% of on-site and 90.21% of online transactions that could not be completed using credit cards can now be completed using e-wallet credit. The combination of demand from consumers and merchants for BNPL, and the supply by the e-wallet provider, has led to the exponential growth of BNPL usage. The impact of BNPL access on consumer credit usage also appears more pronounced in less-developed areas such as rural areas and northern regions and for women. Overall, e-wallet credit seems to provide expanded financial inclusion and benefit those disadvantaged or underserved by banks.

Buy now, pay later and consumer behaviour

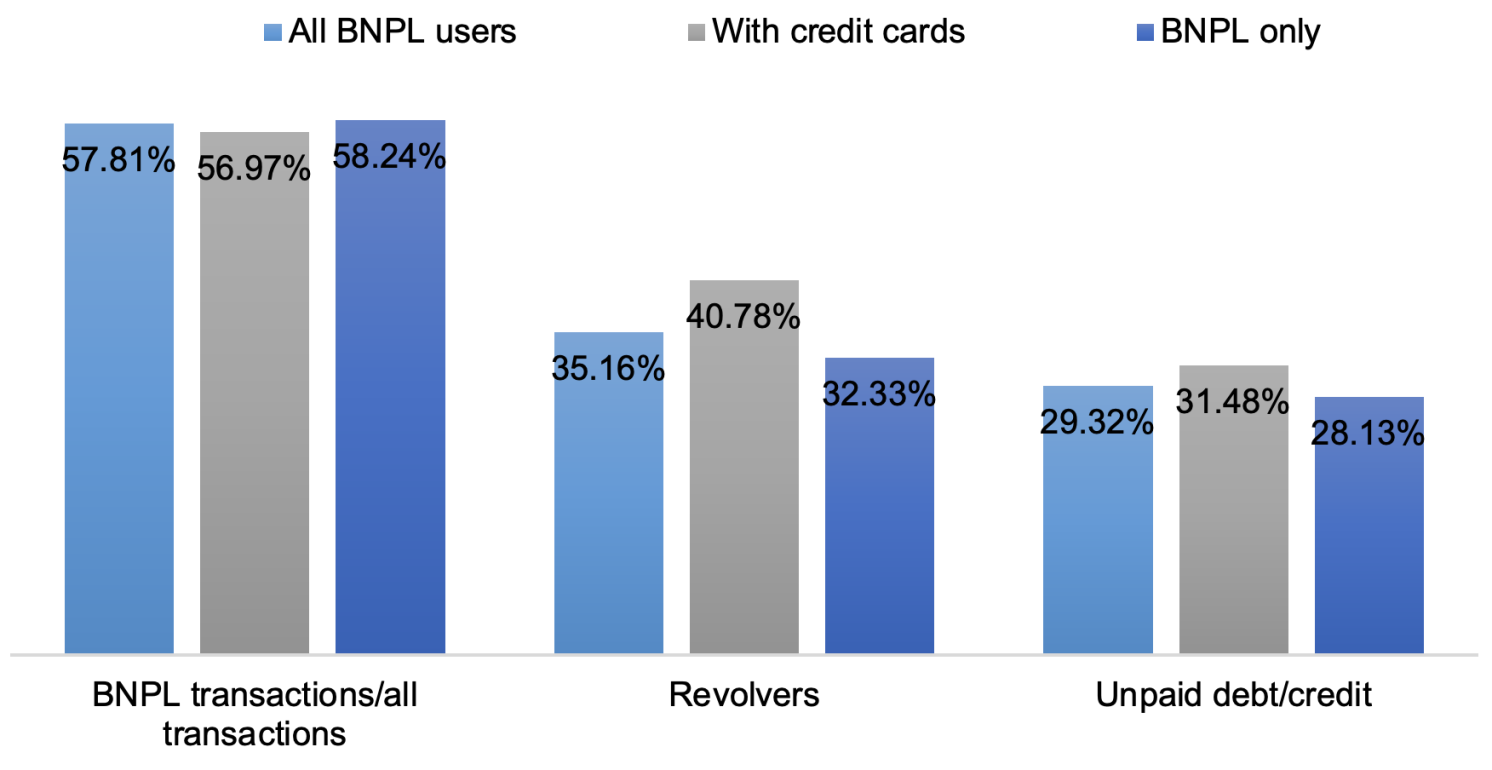

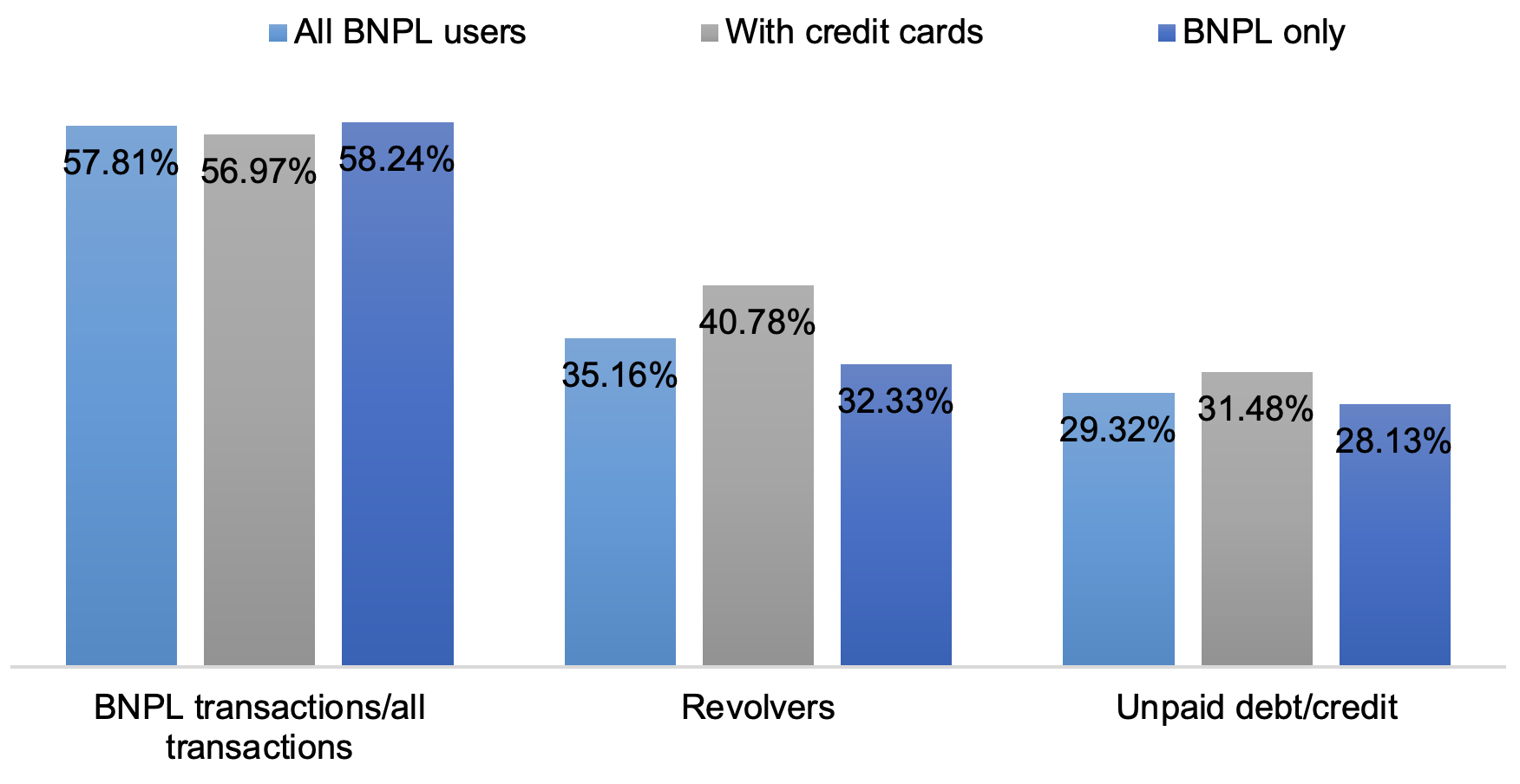

With the wide use of BNPL, a potential concern is that the ease and convenience of this FinTech-based consumer credit may induce consumers – especially unsophisticated ones who lack financial literacy and budgeting education – to overborrow and overspend (Berg et al. 2022, Bu et al. 2022). We analyse how consumers change their usage of BNPL when they have unpaid debt and incur interest expenses. We distinguish between two types of users according to their credit access: single-access users (e-wallet credit users with no linked credit card) and dual-access users (users with access to both e-wallet credit and credit cards). As demonstrated in Figure 2, while single-access users appear to use e-wallet credit more frequently, they use the credit cautiously, as the proportion of revolvers (those who incur interest charges on unpaid debt) and the unpaid-debt ratio for revolvers are lower. They also reduce BNPL usage in transactions once they incur interest expenses from late payments, likely as an attempt to improve their credit score and to pave a pathway to bank credit access (Agarwal et al. 2023). To some extent, this finding alleviates our concern that users who receive consumer credit for the first time may overuse e-wallet credit due to a lack of financial literacy and budgeting education.

Figure 2 BNPL usage comparison between single-access users and dual-access users

Our findings have broad implications. First, given that payment networks have constituted the core products of BigTech giants and FinTech startups, our investigation on the distribution of payment choices in e-wallet transactions provides an initial benchmark for understanding their role in large digital ecosystems. Second, because e-wallet providers have high-frequency and exclusive data on merchants and consumers underserved by banks, discussions on ‘open-FinTech’ – in addition to the ‘open banking’ proposal – can be timely. Third, although BNPL raises concerns about consumer indebtedness worldwide, our study suggests that BNPL users, especially those with no credit access from banks, carefully moderate credit usage in an economy transitioning from cash-heavy to cashless. Credit expansion through BNPL does not necessarily come at the expense of greater consumer indebtedness or default under inclusive, ex-ante screening and ex-post monitoring and incentive provision of the e-wallet provider.

")

")

.jpeg")

")

")

")

")

")

")