The past four decades saw a significant increase in regional housing price disparities in the US and internationally, coinciding with a consistent fall in real interest rates. This column uses a comprehensive international dataset to show that differences in housing prices have risen considerably more than differences in rents. The authors argue that this challenges current theories on the causes of regional housing price inequality, and present evidence of a new mechanism instead: the decrease in real interest rates has disproportionately inflated prices in major cities where the initial rent-to-price ratio is low, leading to a polarized housing market between cities.

The past four decades have seen a significant increase in regional housing price disparities in the US and internationally (Hilber and Mense 2021, Van Nieuwerburgh and Weill 2010), which has sparked a widespread discussion on the causes and potential policy solutions for the ongoing housing affordability crisis in the large urban centers (JCHS 2022, European Commission 2022, UN 2020).

At the same time, real interest rates consistently fell from the 1980s until recently (Del Negro et al. 2019, Rachel and Summers 2019, Blanchard and Katz 1992). Our new paper (Amaral et al. 2023), offers a mechanism that explains how these two trends are interconnected. We show that a national decline in real interest rates leads to increased regional housing price dispersion even without an increase in rent dispersion when there are spatial differences in rent-to-price ratios. We provide robust empirical evidence to support this mechanism in the paper. In a companion paper (Amaral et al. 2021), we argue that different rent-to-price ratios are a function of spatial heterogeneity in the risk of housing markets.

Polarisation of housing markets

Why have housing prices risen more in certain areas than others? In the simplest explanation, housing prices are determined by rental income: the value of a property is equal to the estimated future rental income it will generate, discounted to its present value (Poterba 1984). A key implication of this theory – and the basis for most current explanations of increasing disparities in housing prices – is that price and rent disparities should move in tandem.

For instance, Van Nieuwerburgh and Weill (2010) developed a dynamic spatial equilibrium model for metropolitan areas in the US to show how rents adjust to offset regional differences in productivity. In another study, Gyourko et al. (2013) used a model with two locations to demonstrate that in cities with limited housing supply, rents respond more to increasing national housing demand. Both models predict that rising rents will result in rising prices based on the present-value equation. However, while these models accurately predict the level of price dispersion in the data, they significantly overestimate the level of rent dispersion.

This becomes evident in a novel long-term dataset of housing prices and rents that we compiled for 27 major metropolitan areas in 15 developed countries. The same patterns in the data can also be found in long-term data for the entire cross-section of US metropolitan statistical areas (MSAs). In both data sets, housing prices across cities have diverged considerably more than rents within countries.

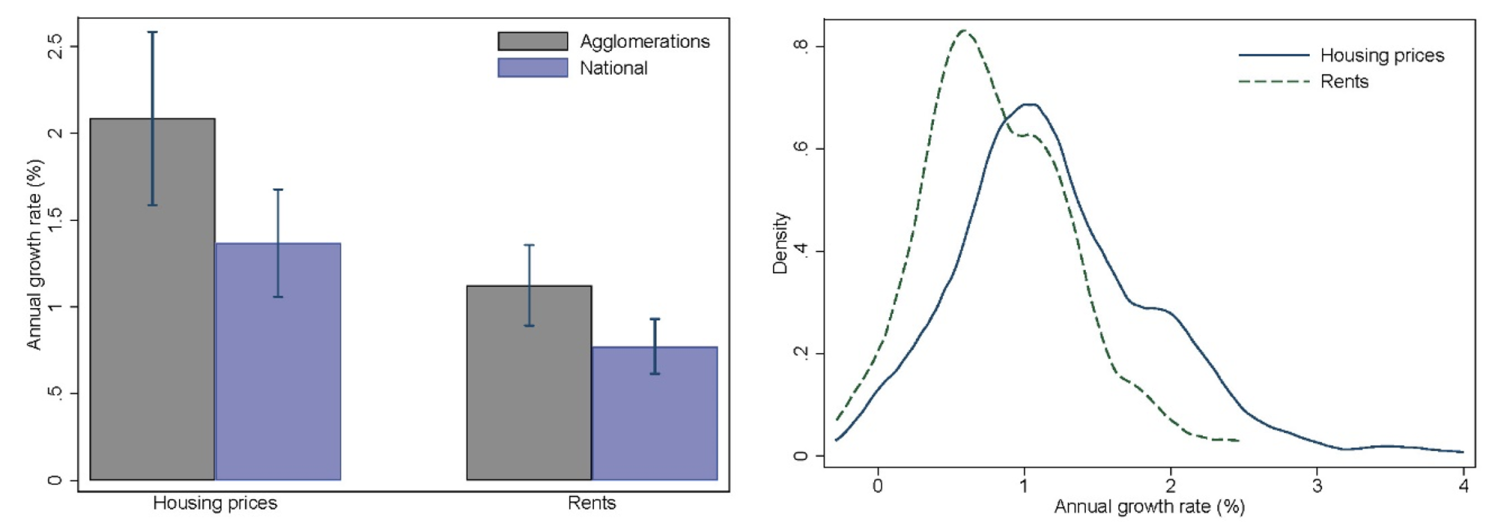

This is shown in panel (a) of Figure 1, which displays the geometric mean of real housing price and rent increases between 1980 and 2018 for the 27 major agglomerations and their respective national averages. The figure highlights two key findings. First, it is clear that housing prices have risen at a much faster pace compared to rents, both in the major metropolitan areas and on a national level. Second, it is noticeable that housing prices have grown considerably more in the major agglomerations compared to the national average, while the difference in rent growth is substantially smaller.

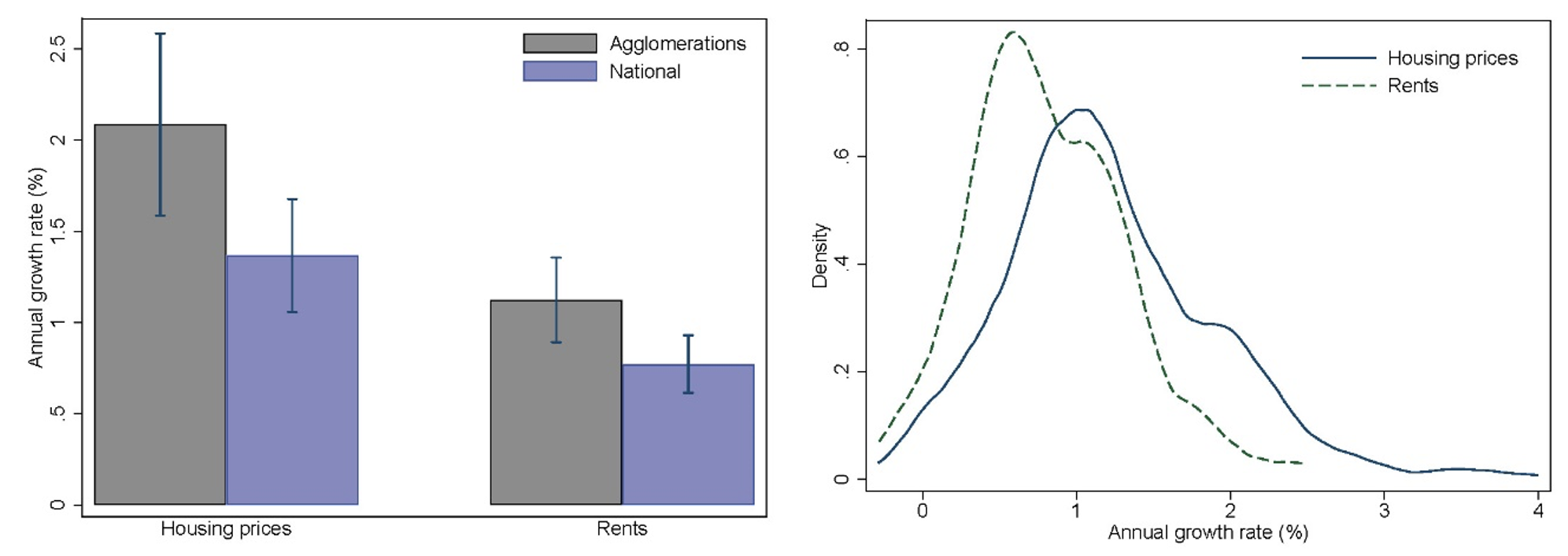

Panel (b) presents kernel densities for the geometric mean of housing price and rent growth rates between 1980 and 2018 by MSA for the full sample of US MSAs. It is evident that not only were housing price growth rates on average higher compared to rent growth rates, but they also displayed more dispersion.

Figure 1 Housing price and rent growth between 1980 and 2018

Notes: Panel (a): Geometric mean of annual housing price and rent growth rates of 27 major agglomerations (black) and the respective national averages weighted by the number of sample agglomerations in the respective country. Means and confidence intervals are calculated using log growth rates. Panel (b): Kernel density of annualized housing price and rent growth rates between 1980 and 2018 for 316 U.S. MSAs.

Falling real interest rates and housing price dispersion

We propose a new explanation that accounts for the widening gap in housing prices within a country, despite relatively modest increases in rent disparity, and even without changes in rents. Our theory posits that a decrease in real risk-free interest rates will have a varying impact on housing prices, depending on the initial variations in rent-to-price ratios across housing markets within an economy.

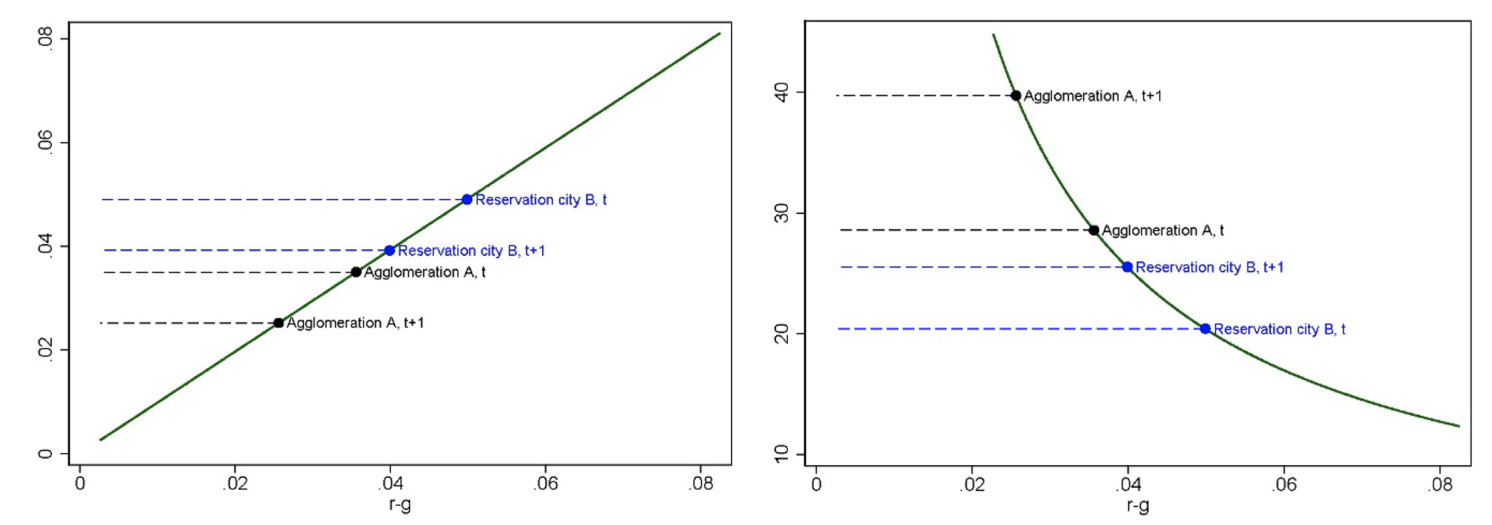

The underlying concept of the model is illustrated in Figure 2, which depicts a scenario with two cities. A general decline in real discount rates, triggered by a decrease in interest rates, results in a parallel decline in the rent-to-price ratios but a non-linear increase in the price-to-rent ratios. As a result, the price disparity between the agglomeration and the reservation city increases when the real discount rate falls, even when rents remain constant in both cities.

Figure 2 A fall in real discount rates in the model

Notes: Panel (a) plots the rent–price ratio in our model as a function of r – g, where r is the real discount rate and g is the real growth rate of rents. To calculate the points, we assumed that g = 0.0175. Panel (b) shows the corresponding price–rent ratio.

A fundamental assumption of the model is that rent-to-price ratios are lower in large urban centers. The question is, what causes the variations in rent-to-price ratios among cities? In Amaral et al. (2021), we present extensive evidence that cities with lower rent-to-price ratios also have consistently lower overall returns on housing investments. Furthermore, these cities also have lower risks associated with housing investments. Building on existing literature, we quantify two significant sources of housing risk. First, housing returns have a weaker correlation with local income growth in large urban centers. This is often the case as smaller cities tend to have less diversified local industries, making them more susceptible to industry-specific shocks. Second, sales-specific risk is substantially lower in large cities, which is supported by the fact that liquidity is much higher in these cities.

Conclusion

Using a novel long-term dataset of housing prices and rents for 27 major urban centers, we discovered a pattern of significant divergence in within-country housing prices compared to rents. This trend began in the 1980s, which coincides with the start of the decline in interest rates. Our research demonstrates that these two facts are related, and that a decrease in real interest rates can lead to an increase in housing price disparities, given initial differences in rent-to-price ratios across cities.

Previous explanations for the rise in regional housing price disparities have primarily focused on differences in housing market fundamentals, however, our study shows that macro-financial factors, such as interest rates, also play a significant role. Our research contributes to the ongoing debate by identifying a previously overlooked source of housing price dispersion: falling interest rates. The mechanism we presented also has implications for the future of the housing market in the current environment of rising interest rates. If real discount rates rise again, some of the polarization of housing prices observed over the past decades can be expected to revert.

Source : VOXEu

")

")

.jpeg")

")

")

")

")

")

")