Recently, there has been a growing interest in long-term savings institutions such as pension and insurance funds. This is due to the significant growth in their assets and the potential impact they may have on the proper functioning of markets (Liao and Zhang 2020, Borio et al. 2022). For instance, an OECD report shows that in 2020, pension funds in OECD countries held an average of 100% of assets in terms of GDP, up from 63% in 2010 (OECD 2021). As their assets grow, pension funds often invest abroad as they become large relative to their local financial markets. The report states that out of a sample of 50 countries, these pension funds invested 35% of their assets in 2020, with some countries as high as 90% of their assets.

In a recent paper (Ben Zeev and Nathan 2023), we examine the impact of the expanding investments of institutional investors abroad by introducing a novel channel of exchange rate determination. Specifically, we analyse the effect of global equity market shocks on the collective hedging of FX risk by local institutional investors. Utilising unique daily data on FX forward flows of Israeli institutional investors, we can establish a causal relationship. Our findings suggest that a rise in the MSCI ACWI index – a popular index of global equities – leads to substantial and prolonged selling of dollar forwards by institutional investors, which is likely done as a means of hedging against increased FX exposure. 1 As a result, both US dollar/New Israel shekel (USD/NIS) spot and forward rates experience a significant and prolonged decrease in value following the MSCI innovation.

The equity hedging channel of exchange rate determination

We begin by clarifying our terminology. In this column, we use the terms ‘dollar’ and ‘foreign currency’ interchangeably to refer to the USD/NIS currency pair, as 84% and 81% of Israeli institutional investors’ FX forward and spot trades, respectively, are conducted in dollars. (The remaining 16% and 19% of these trades are included in our data and converted to dollar terms.)

Investing abroad is not a free lunch. Institutional investors face FX risk and currency mismatch when investing abroad, as their liabilities are in the local currency while a portion of their assets is in foreign currency. Any potential gains from investing abroad must be hedged to avoid severe losses. For instance, consider a foreign investor that invested in the S&P 500 in 2020, which had a 16% increase in value. The same year, the value of the US dollar weakened by 3%. 2 Therefore, an investor who did not hedge his FX risk would have lost almost 20% of their investment in their local currency.

There are several ways institutional investors hedge their FX risk. One is to sell foreign equities if they appreciate and immediately convert the profits to local currency (Hau and Rey 2006). Another way – the focus of our paper and what we call the “equity hedging channel of exchange rate determination” – is selling the dollar profits and buying the local currency in the FX forward market. The selling guarantees that no losses will be suffered due to future changes in the value of the dollar. It also has an added advantage compared to simply selling an asset: when the forward contract matures, one can roll it over and not necessarily have to sell the asset. It also guarantees that you will continue to be fully hedged. 3

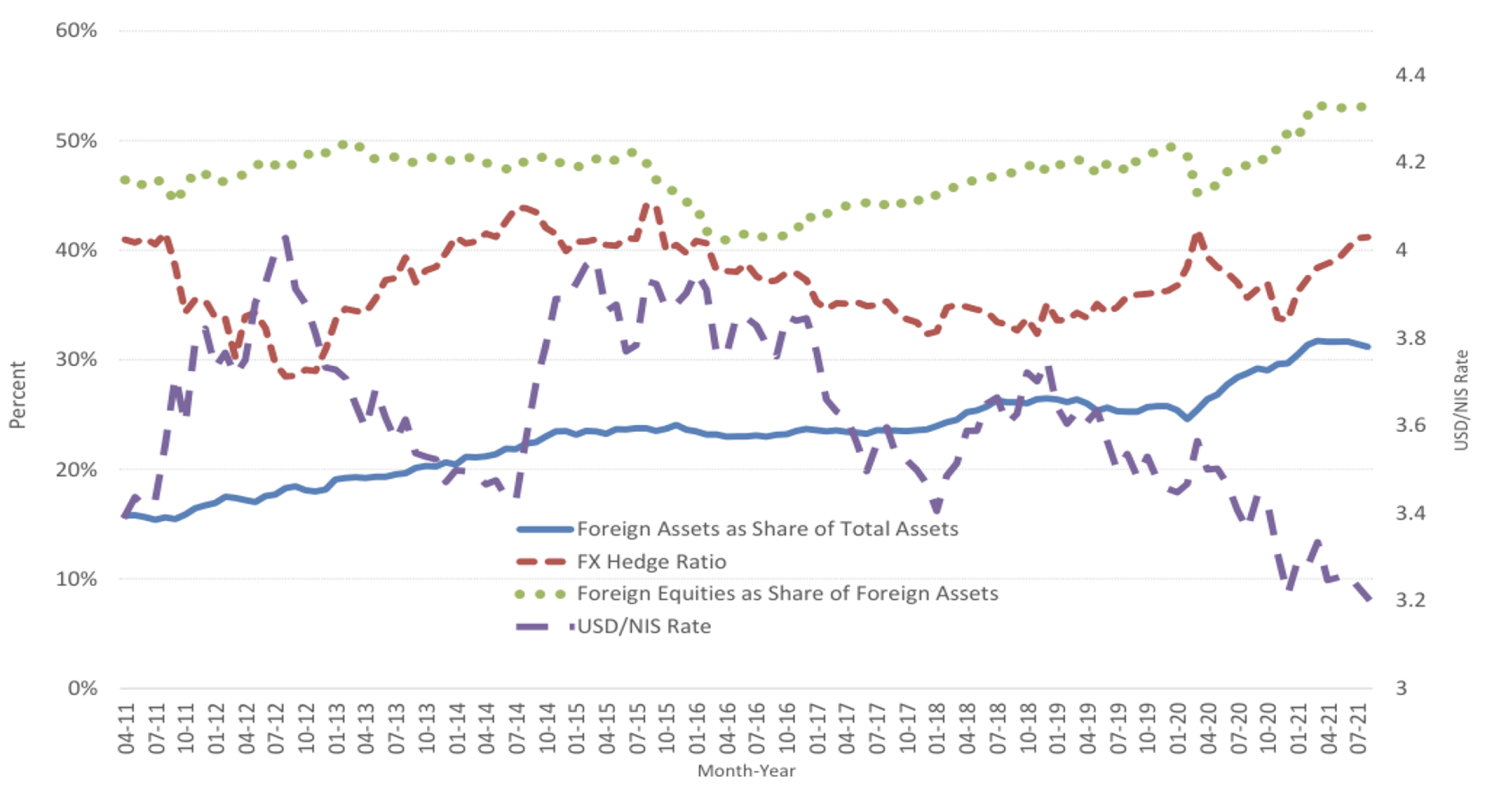

Unique monthly data from Israel illustrate that institutional investors hedge their overseas investments. Figure 1 shows the percentage of assets held abroad by Israeli institutional investors, the percentage of it in the form of equities, and their FX hedging percentage (the right axis represents the USD/NIS rate). The results (square dotted green line) show that institutional investors, on average, hedge 37% of their FX-sensitive positions, indicating a significant level of hedging activity among institutional investors.

Figure 1 Institutional investors’ assets, foreign equities, FX hedge ratio, and USD/NIS spot rate

How does our proposed mechanism impact the exchange rate? When the value of foreign equities increases, institutional investors begin selling forward foreign currency (such as dollars) and buying forward their local currency. The selling pressure created by this action leads to a decrease in the forward rate. Since the forward and spot rates are related through the covered interest rate parity, this results in a decrease in the spot rate as well. 4

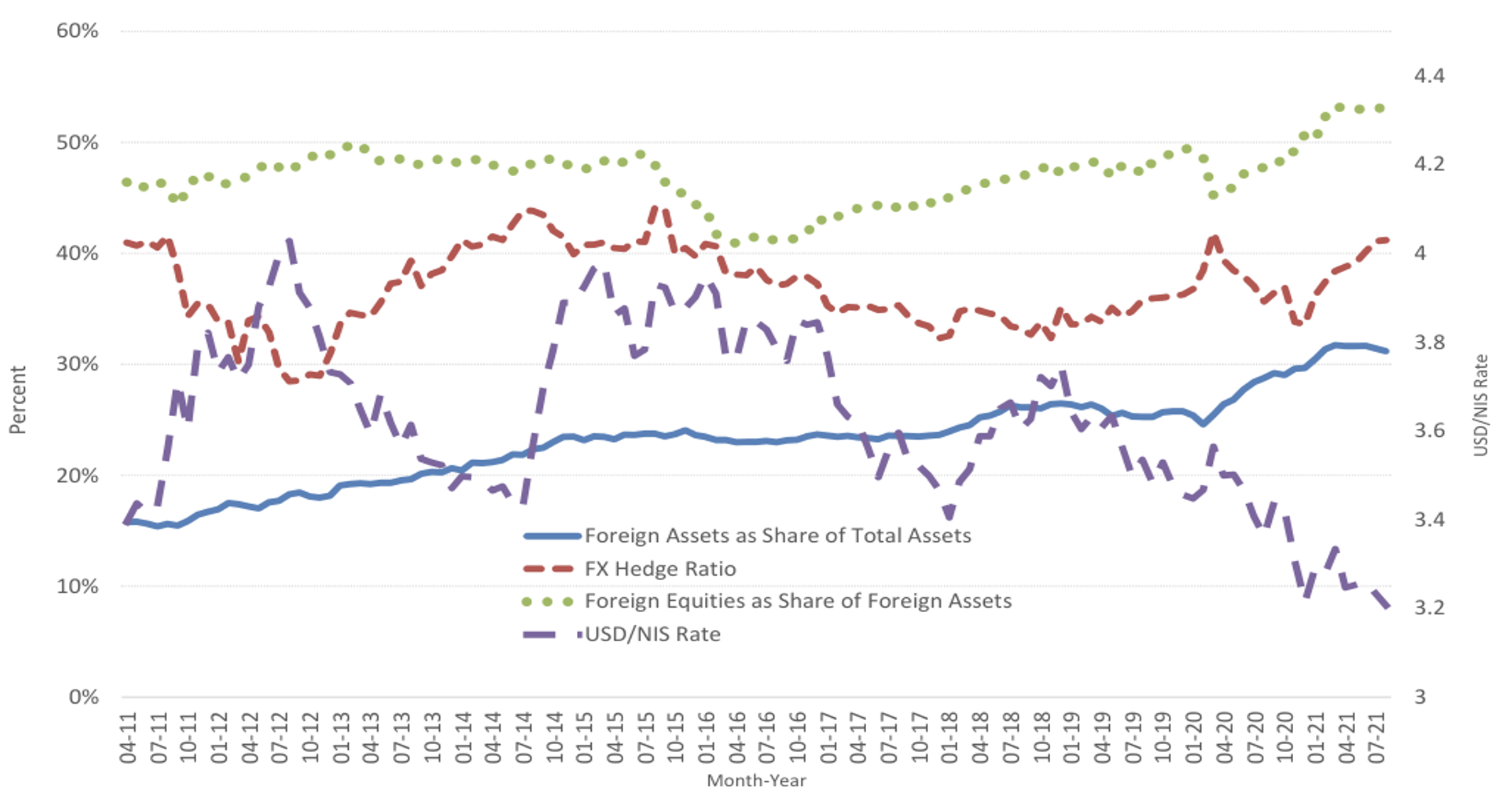

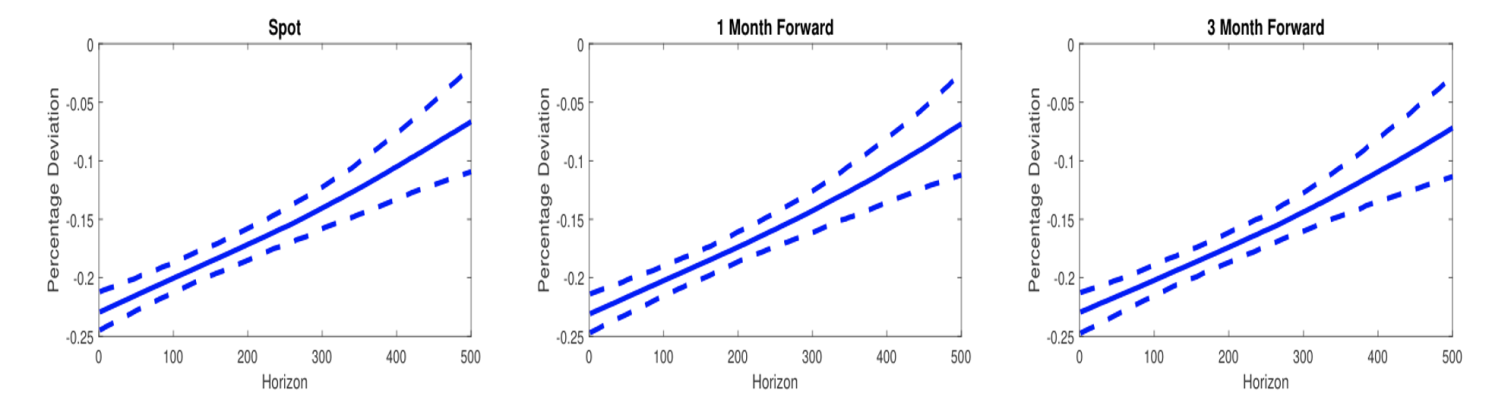

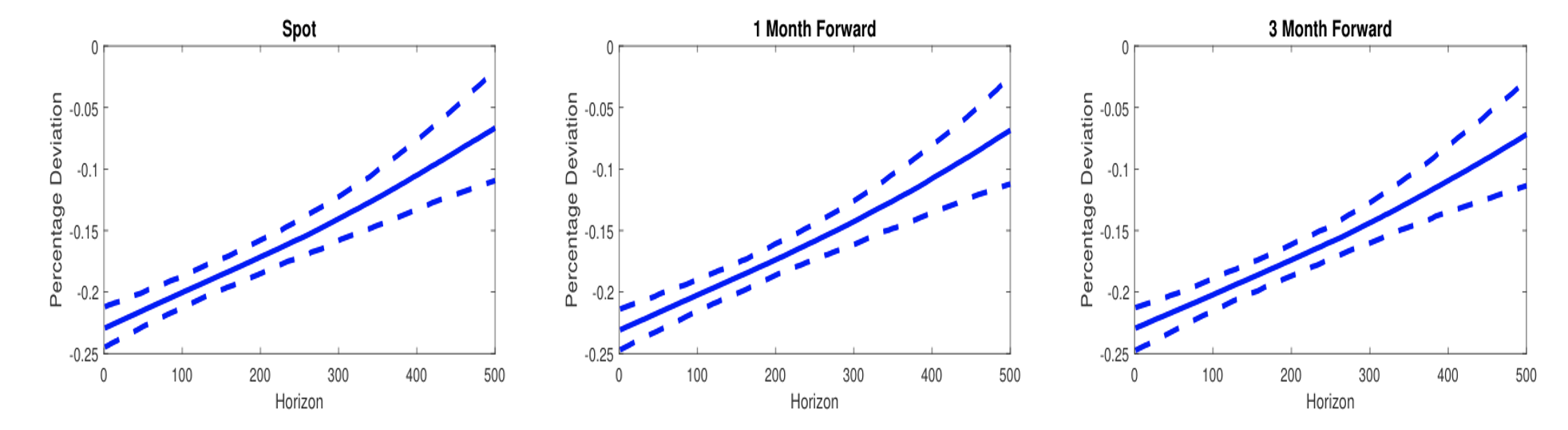

In the next part of our paper, we confirm our hypothesis empirically. Using unique daily data from Israeli institutional investors over 13 years (2008-2021), we find that a one standard deviation innovation in the MSCI index leads to significant and persistent selling of dollar forwards by institutional investors, peaking at $2.8 million on impact and accumulating to $338.8 million after around 1.1 years (Figure 2). This selling coincides with a decline in the USD/NIS spot and forward rates, which is economically and statistically significant (Figure 3). 5

Figure 2 Response of cumulative forward flows by institutional investors to a one standard deviation shock of the MSCI ACWI

Figure 3 Response of the USD/NIS spot and the one- and three-month USD/NIS forward rates to a one standard deviation MSCI-ACWI shock

Robustness

We address the concern that institutional investors’ hedging does not affect exchange rates by analysing the impact of a shock to institutional investors’ forward supply unrelated to changes in the MSCI index. The results show a weaker, but still statistically significant effect on the exchange rate compared to an MSCI shock. This is likely due to the lower persistence of forward selling after a non-MSCI shock, which suggests it represents a short-term desire to hedge rather than a response to changes in the MSCI which are long-lived.

External validity

Our research suggests that the FX hedging channel is not exclusive to the Israeli economy. As mentioned, pension funds often invest significant portions of their assets overseas. Survey data indicate that many institutional investors in countries such as Chile, Colombia, Denmark, Mexico, Norway, Sweden, and Switzerland also engage in meaningful FX hedging. A survey of 927 institutional investors in 12 countries, representing over $1.1 trillion in assets, found that 42% of surveyed investors hedge at least 60% of their FX exposure in listed equity portfolios.

Conclusion

In this column we present evidence of a significant correlation between institutional investors’ selling of dollar forwards and an innovation in the MSCI index, resulting in a decline in USD/NIS forward and spot rates. This supports the existence of a meaningful equity hedging channel, where an increase in foreign stock markets leads to a shift in institutional investors’ supply of dollar forwards, affecting exchange rate determination.

The determinants of exchange rate behavior have long eluded researchers (Schreger et al. 2020). We believe our study can shed more light on the determinants of exchange rate determination, and hope it will further our understanding of the relationship between institutional investors’ foreign equity positions, hedging, and exchange rate determination. We believe the results apply to other small economies where institutional investors have a significant foreign equity position and engage in meaningful FX hedging. The findings may also have important policy implications, suggesting that FX intervention in the forward market may be more effective in combating an exchange rate appreciation, and that limiting institutional investors’ hedging through taxation or restrictions may be a viable option for policymakers to consider.

Source : VOXeu

")

")

.jpeg")

")

")

")

")

")

")