This Policy Brief sets out why the deforestation regulation has the right objectives but needed better design and preparation for implementation

Forests are essential to regulating the climate, absorbing greenhouse gases and providing fresh water and habitats for biodiversity and indigenous peoples. If deforestation continues at current rates, large parts of the planet will become uninhabitable. The European Union has only 5.5 percent of the world’s population, but its demand drives 15 percent of the global forest destruction linked to trade. Therefore, the EU has introduced a law – the regulation on deforestation-free products, or deforestation regulation – to outlaw from its market products linked to deforestation.

The regulation has triggered protest about its impact on trade partners, leading the European Commission to propose at short notice a delay in its implementation. However, the objectives of the regulation remain valid and important. Moreover, a large majority of EU consumers want to avoid buying products that result from deforestation and find it frustratingly difficult to find information on whether products are deforestation-free. Economic actors in most of the affected sectors support the objectives of the regulation, even though they criticise the way it has been implemented.

To avoid this delay having a chilling effect on other green measures in future, the EU should learn lessons from this experience. The European Commission needs to develop a consistent and effective strategy for managing the external impact of the EU’s green policy agenda, with better diplomacy towards trade partners and specific financial assistance to help the poorer countries with compliance and the transition to more sustainable production.

This Policy Brief sets out why the deforestation regulation has the right objectives but needed better design and preparation for implementation. In particular, the EU needs to provide more flanking support for developing countries to ease their transitions and improve forest protection. Economic actors along the whole of supply chains need more consultation during the design stage, and the Commission needs to provide clearer guidance by sector and a well-functioning system for compliance.

1 Introduction

The European Union’s regulation on deforestation-free products (EUDR, Regulation (EU) 2023/1115) bans traders and operators from placing on the EU market certain commodities and products 1 that have contributed to deforestation in the EU or abroad after 31 December 2020. Operators must submit due diligence data that includes the geocoordinates of the plots of land used to cultivate the commodity that went into the product. The due diligence is made available to European competent authorities, which carry out checks to varying degrees depending on a risk categorisation by the EU of the country of origin.

The regulation is expected to have a significant impact on many countries and companies, and has provoked complaints from trade partners 2 . The European Commission proposed in September 2024 to delay its application date by a year (to 2026 for larger operators and to mid-2026 for micro and small businesses). The delay seems to have resulted from poor planning by the European Commission, particularly lack of engagement with producer countries and firms on the design of the compliance system. The EU information system was not ready and clear guidelines to operators, traders, companies and trading partners were lacking ahead of the originally planned date of application of end-2024.

There will also be new discussions on the details of the risk-categorisation approach, since the European Parliament proposed the introduction of a ‘no risk’ category, covering countries considered as having a negligible or non-existent risk of deforestation. This could exempt the EU member states and potentially other countries 3 . However, the rest of the regulation is likely to enter into force.

2 The objectives of the EUDR are valid and important

Deforestation is a major cause of environmental degradation globally, and EU consumption is responsible for a significant proportion of it. Over 90 percent of tropical deforestation is driven by agricultural expansion, mostly for just a handful of globally traded commodities (Pendrill et al, 2022).

Loss of forest has potentially irreversible effects on systems including water regulation, protection from natural hazards, reduced biodiversity and carbon storage (Lange et al, 2018). Deforestation accounts for 11 percent of greenhouse gas emissions globally. All pathways to limit warming to 1.5 degrees Celsius, as modelled by the Intergovernmental Panel on Climate Change, require major reductions in deforestation, plus reforestation and afforestation (IPCC, 2019). It is therefore essential to tackle deforestation as part of a comprehensive climate policy, especially given poor global adherence to deforestation targets 4 and the deteriorating integrity of forests, as demonstrated by the deterioration in how much carbon dioxide forests can absorb because of record warming in 2023 (Ke et al, 2024).

Beyond absorbing carbon emissions, forests also provide essential ecosystem services that cannot be substituted by human technologies, notably as habitats for many species and for indigenous peoples. Land-use change, particularly the expansion of agriculture into tropical forests, is the number one reason that species are threatened with extinction globally (see IPBES, 2019). Forests are also essential for the hydrological cycles that produce fresh water.

European old-growth forests – which are important stocks of carbon and biodiversity habitats – are rare and fragmented, and deforestation of old growth forest in the Global South in previous centuries provided exports to Europe. Just as Europe emitted a large proportion of the greenhouse gases now in the atmosphere, Europe’s historical role in the destruction of forests across several continents creates a special responsibility to preserve and repair forests globally.

The EUDR recognised the EU’s current and historical responsibility. EU trade from 2005 to 2013 was associated more than any other economy with tropical deforestation through its imports of agricultural commodities; China overtook the EU in 2014 (Richens, 2021). From 1990 to 2008, the EU was responsible for 10 percent of global deforestation, rising by 2017 to 16 percent of the deforestation associated with international trade, totalling 203,000 hectares and 116 million tonnes of CO₂ (Wedeux and Schulmeister-Olden, 2021). From 2019 to 2021, the EU was responsible for 15 percent of the global deforestation linked to international trade, ahead of India, the US and Japan (Titley, 2024). This corresponds to 190,500 hectares of deforestation every year, about three-quarters the size of Luxembourg.

Deforestation in forest habitats induced by the EU has reduced over the last seven years, but remains high (Figure 1). In 2021, deforestation embodied in the EU’s consumption of the seven commodities covered by the EUDR was responsible for over 100,000 hectares of deforestation globally.

The EUDR is well targeted in terms of commodities. The seven commodities it covers (see footnote 1) were responsible for 86.6 percent of tropical deforestation embedded in EU imports of commodities between 2005 and 2017 (Wedeux and Schulmeister-Oldenhove, 2021).

However, the regulation is less-well targeted to important ecosystems. The regulation contains a strict definition of ‘forest’. This means that products that have caused deforestation in savannahs, wetlands and other non-forest wooded lands do not fall under the scope of EUDR, even though deforestation also takes place in these eco-systems and they are significant for both carbon sequestration and biodiversity habitats. For example, in 2016, 70 percent of the deforestation and conversion associated with EU soy imports from South America took place in the Cerrado savannah region of Brazil (Wedeux and Schulmeister-Oldenhove, 2021), one of the world’s 36 biodiversity hotspots, yet this falls outside of the scope of the EUDR. An evaluation two years after the EUDR’s entry into force will assess the extension of the deforestation regulation into other commodities and ecosystems.

Moreover, a 2022 poll showed strong support for the objective of only deforestation-free products arriving on European markets, with 82 percent of European consumers believing that “companies should not be selling products that are bad for the world’s forests” and “it is frustratingly difficult to tell if a product is deforestation-free, or not, when shopping” (GlobeScan, 2022).

Figure 1: EU deforestation exposure from EUDR commodities

Source: Titley (2024). Notes: the data only includes deforestation happening in forest habitats. The data is not fully aligned with the EUDR since deforestation estimates for more processed commodities are not all included. This is particularly likely to underestimate the footprint from rubber and wood products. A panel for rubber is not shown because values are very low.

3 The EU needs to help its more vulnerable trade partners to adjust

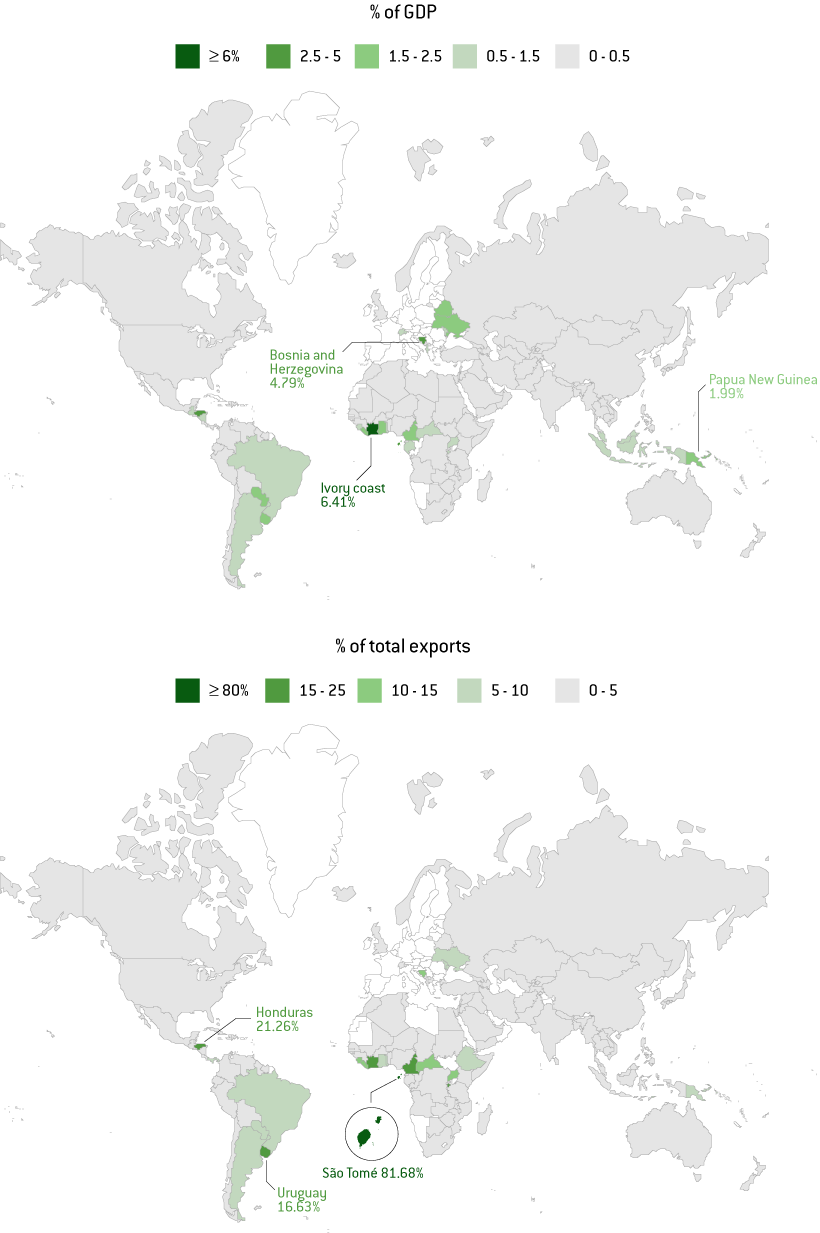

The EUDR affects a non-trivial portion of global trade. Total exports to the EU of goods that will be subject to the EUDR (henceforth EUDR exports) accounted for over 1 percent of the total exports of 57 countries from 2015 to 2023 (Figure 2). This reaches as high as 81.7 percent for São Tomé and Príncipe, one of the 20 African countries where EUDR exports are over 1 percent of total exports.

The EUDR also affects a non-trivial proportion of exporting countries’ GDP. In 31 countries, EUDR exports were over 0.5 percent of GDP during the 2015 to 2023 period. This reached as high as 6.4 percent for Côte d’Ivoire, but also affects several countries that are candidates for EU membership, including Bosnia and Herzegovina (4.8 percent), North Macedonia (1.9 percent) and Ukraine (1.6 percent).

Many developing countries rely on commodity exports as a source of government revenue and foreign exchange earnings. If the EUDR disrupts exports from poorer trading partners, then it may affect their revenue-collecting ability.

The Commission and several EU countries have announced a ‘Team Europe’ 5 initiative worth €70 million to support partner governments to minimise deforestation and help smallholders and low-income countries adjust to the EUDR. Projects are already underway in Asia, Africa and Latin America. Yet there is little published research on how an EUDR import ban on products linked to deforestation would reverberate throughout the supply chains of each of the seven commodities.

Countries that export commodities for which the EU has large global market share would likely face the most disruption from a ban. Although the EU is a relatively minor importer of soya, wood and oil palm, it is a major importer of coffee and cocoa, for which the EU’s shares of global net imports are 40.7 percent and 35.5 percent respectively (Table 1). This means that exporters of cocoa and coffee that face disruption linked to the EUDR may find it harder to find other markets that will absorb the goods banned by the EUDR. However, for commodities including soya and oil palm, there are likely to be ample trade-diversion opportunities. In some sectors, it is possible that the EUDR will lead to a two-tier export market in which, for example, EUDR palm oil is sold to the EU at a premium, while palm oil grown on deforested land is exported to other markets.

Table 1: EU imports of EUDR products as a % of global net imports of those products, 2015 – 2022 average

| Product | EU market share (%) |

| Coffee | 40.66 |

| Cocoa | 35.49 |

| Rubber | 24.40 |

| Cattle | 21.87 |

| Oil palm | 19.05 |

| Wood | 15.36 |

| Soya | 14.21 |

Source: Bruegel based on CEPII – BACI. Notes: We include all products that fall under the CN codes listed in Annex 1 to Regulation 2023/1115. We do not exclude products based on the extracts listed in the annex.

Figure 2: Average share of EUDR exports in GDP and total exports, 2015 – 2023

Source: Bruegel. Note: the Annex lists the 30 most affected countries.

The countries particularly at risk are those that have a high dependence on selling one commodity that is covered by the EUDR , so that it affects a significant share of their trade and/or GDP, and where the EU is a large market for that commodity so they cannot sell it elsewhere. Examples include Burundi, for which 99.6 percent of its EUDR exports are coffee, and Ghana and Côte d’Ivoire, for which cocoa constitutes 94.7 percent and 86.5 percent of their EUDR exports respectively.

Even if there are other opportunities to export, disruption for countries that face high GDP or trade exposure, and for which EUDR exports are concentrated in one commodity, might face high costs in the short term. For example, 98.8 percent of the Central African Republic’s EUDR exports are wood, as are 94 percent of Bosnia and Herzegovina’s, both of which have high trade and GDP exposure to the EU, and may have few alternative established trade routes.

Another consideration is those at the top of the supply chain. Ninety percent of cocoa production relies on five million to six million smallholders in developing countries (European Commission, 2021), while up to 73 percent of the global coffee market is supplied by smallholders (Panhuysen and Pierrot, 2020), as is about 40 percent of the world’s palm oil. Smallholders often depend on the crop for their livelihood, making them particularly vulnerable to disruption and making it hard for them to adapt.

Back-of-the-envelope calculations like the above are useful for getting a broad picture, but much more work is needed to identify which countries and populations are most exposed to potential disruption. There are very few detailed quantitative assessments of the impact of the EUDR, which makes it harder to target support and protect those on low incomes who depend most on EU markets.

Several technical obstacles to full implementation of the EUDR also remain. For example, the sharing of geolocation data with EU competent authorities clashes with Indonesian privacy laws 6 , so it is unclear how the EUDR can be implemented in that country. This needs urgent attention and bilateral diplomacy.

4 How the Commission should improve implementation

The EUDR implementation complications have prompted an influx of questions about how to comply 7 . The European Commission’s current approach to clarification is periodic update of its frequently asked questions 8 . This blanket approach comes at the cost of industry-specific guidance, even though the seven sectors targeted by the EUDR (cattle, cocoa, coffee, palm oil, rubber, soya and wood) vary widely in terms of supply-chain complexity, source countries and experience with administrative compliance. Sector-tailored guidance will be important for filling this gap, as the Commission is providing in the preparations for implementation of the EU carbon border adjustment mechanism (to equalise the carbon price applied to domestically produced and imported goods).

To prepare for harvest seasons in 2025, the Commission should provide sector-specific support rapidly. For example, the cocoa harvest in September 2025 will produce cocoa beans and cocoa products that will arrive on the EU market in 2026. In the case of rubber, it can take six months 9 for natural rubber to reach the EU market from its production in Southeast Asia. This means that due diligence must already be carried out in 2025 in preparation for the product’s placement on the market in 2026. The first six months of 2025 are a crucial window for the Commission to ensure operators have all the information they need to comply with EUDR.

Many easy and necessary clarifications and suggestions have been made in good faith by economic actors in the supply chains affected. The most salient of these is calls is for improvement of the information system to which due-diligence statements must be uploaded. Industry has called for a larger file size, and for the system to be made available earlier so that companies can test the system and train staff. This is an uncontroversial fix that would have high returns in terms of facilitating the implementation of EUDR.

5 Lessons for future environmental legislation

The delayed implementation of the EUDR comes at a sensitive time politically, at the start of the 2024-2029 EU institutional cycle and following campaigning against climate and environmental policies by radical right and some centre-right parties in recent elections. More climate and environment regulation will be needed in the rest of the 2020s to meet the EU’s already-agreed targets. In preparation for that, the European Commission in particular should learn a number of lessons.

Signal the EU’s intentions consistently

The delay to the EUDR risks being interpreted both inside the EU and externally as a signal that the 2024-2029 European Commission will focus on decarbonisation and the broader energy transition, with much less effort on biodiversity and nature degradation. There is a major risk that trade partners and EU stakeholders will have the impression of waning commitment to targets and green legislation passed during 2019-2024. If unaddressed, this impression will raise questions about whether other legislation, such as the carbon border adjustment mechanism (Regulation (EU) 2023/956), might be similarly delayed. Speculation about other postponements should be quelled while adjustments that improve implementation should be made, given how much EU green measures rely on credibility for their effects. The ultimate goal is not to punish trade partners and companies, but to set expectations of market access that create incentives to make production methods more sustainable.

Above all, firms need certainty. Although delay may help some sectors, firms and trading partners, which were underprepared, many have already invested time and money to comply with the EUDR. Several large companies in affected sectors – chocolate, rubber, supermarkets – have warned against weakening the EUDR 10 . Whilst postponement is a common method to manage the politics around legislation, the delay was announced unilaterally just one day after the Commission stated at an international meeting in Geneva that there would be no extension of the EUDR 11 . This does not set a good precedent for reliable implementation of future regulation that may prove controversial.

Tailor regulation to sectors

The seven sectors covered by the EUDR have in common that they contribute to deforestation. Beyond this, the sectors have different characteristics when it comes to cultivation, supply chain, trading partners and product use. Yet the EUDR is a blanket regulation that takes little account of these differences. For example, re-treaded rubber tyres are also subject to the EUDR, which will impede the re-use of tyre carcasses that were on the EU market before the EUDR deadline, inhibiting the circular economy 12 .

Design the information system taking into account the needs of users

Compliance systems need to be ready to receive more data and should take account of the legal and technical limitations on geo-location in supplier countries.

Design an adaptation period for transformative regulation

The EUDR requires major adaptation of production and marketing practices, yet it was foreseen to apply overnight. Such transformative regulation would benefit from a grace period or transitional phase, similarly to CBAM, rather than a hard introduction, as foreseen for the EUDR. A year-long transitional period would have avoided the delay. This is especially true for legislation that affects small suppliers in developing countries. The EU needs to provide earlier and more comprehensive financial and technical assistance during an adequate preparation period. Low-income countries need support that is well-coordinated between the Team Europe initiative, partner governments and multilateral donors.

Improve external and internal communication

Companies working in affected sectors generally support the objectives of the regulation and want to eliminate deforestation and human-rights abuses from their supply chains. However, they complain frequently about how the Commission conducts consultations and about lack of sector-specific engagement that would have improved multiple aspects, from the design of the compliance system to industry’s understanding of how to implement EUDR.

EU consumers may be worried about the impact on prices of everyday goods such as coffee and chocolate. Even if the impact on retail prices may be small, it is important to address such concerns to forestall speculation.

Externally, the EU needs to use its diplomatic network and contacts with ministers in affected countries more actively and much earlier in the process of creating new legislation. This is not easy for the Commission in the EU legislative process because major changes may be made by the European Parliament or Council of the EU; indeed, the Parliament added products to the EUDR. Nevertheless, better updating of relevant ministers in partner countries could prevent problems rising up to the level of prime ministers’ conversations with the Commission president.

Ensure greater agency by the countries owning the forests

The legislation is rigid in that it relies on due diligence by the operators and enforcement by the competent authorities. This is burdensome, gives no agency to authorities in the exporting countries, nor any flexibility for third-party certification schemes, such as those offered by NGOs that provide rainforest certification schemes. Future regulation could introduce such flexibilities.

Design policy to tackle root causes

A ban on products is not by itself always the most effective approach, as it can lead to trade diversion and neglect issues that require active engagement, such as child labour. The ultimate aim of measures such as the EUDR is to change the incentives for production and reward responsible producers that use methods that preserve nature. To do that, the EU could help producer countries to develop their own national traceability systems, as trade facilitation tools, and reward those with better national forest protection. In the longer run, policies that aim to give more agency to the countries managing the forests to build their own capacity will be more effective. Ultimately, pricing products according to their environmental impact would incentivise forest-friendly production better than a ban.

The experience of the introduction of the EUDR offers important lessons for future regulation, yet the rationale for the regulation is valid (and its substance should not be re-opened, for example by introducing a ‘no-risk’ category of exporting countries; see section 1), both to protect forests and to give economic actors the certainty they need.

Crucially for its global green reach in future, the EU must communicate with trading partners and reduce the impact on them by providing targeted assistance to the most vulnerable smallholders and countries that are struggling to comply in time. Stakeholders have sought in good faith to reduce deforestation and they emphasise the need for a consistent regulation. The EU should now stay the course because forest protection is too important to become a point of controversy in global cooperation on climate and nature.

Source : Bruegel

")

")

.jpeg")

")

")

")

")

")

")