Household debt dynamics are widely recognised as an important driver of boom-bust cycles, but corporate debt has received less attention. This column studies the role of firm debt in macroeconomic fluctuations using a large historical cross-country dataset. The authors show that corporate debt plays a crucial role in boom-bust cycles, financial crises, and sluggish macroeconomic recoveries. Furthermore, real estate collateral and credit dispersion across sectors are important predictors of crises. Thus, corporate debt has important implications for models of macro-financial linkages and the design of macroprudential policy.

Since the global crisis of 2007-08, household debt has been regarded as a major driver of financial crises. This has prompted macroprudential policy in many countries to focus on tightening borrowing constraints in this sector. A large body of evidence shows that household debt played a key role in the boom-bust cycle of the 2000s in the US (e.g. Mian and Sufi 2009, 2010, Keys et al. 2010). Internationally, increases in household debt have been found to predict business cycle downturns and financial crises (e.g. Buyukkarabacak and Valev 2010, Jordà et al. 2016, Mian et al. 2017) and slow recoveries after such crises (e.g. Jordà et al. 2015, Jordà et al. 2022).

However, the macroeconomic effects of firm debt are inconclusive and have received much less attention. Although there exists firm-level evidence that excessive leverage can harm firm investment and employment (e.g. Giroud and Mueller 2016, Kalemli-Ozcan et al. 2022), Mian et al. (2017), using international data, find that corporate debt dynamics do not generate boom-bust growth cycles and have only weak predictive power for subsequent GDP growth. Similarly, Jordà et al. (2022) conclude that corporate credit booms leave a lasting imprint on the macroeconomy after financial crises only in countries with particularly inefficient corporate bankruptcy regimes.

In a recent paper (Ivashina et al. 2024), we revisit the role of firm debt in macroeconomic fluctuations using a large historical cross-country panel dataset on credit markets from the Global Credit Project (Muller and Verner 2023). This dataset is unique in the sense that it allows us to decompose corporate credit by industry. In total, the dataset covers 115 advanced and emerging economies from 1940 to 2014. We also construct new time series on credit to non-bank financial institutions, which has been missing in previous work. This dataset is unprecedented in its breadth and scope, overlapping with 87 episodes of systemic financial crisis.

Using this more granular dataset, we find that corporate debt plays a crucial role in boom-bust cycles, financial crises, and sluggish macroeconomic recoveries. Firm debt accounts for about two-thirds of the aggregate credit growth in the three years preceding financial crises. After a crisis hits, the ensuing credit crunch is entirely concentrated in credit to firms, as is the vast majority of loans that become nonperforming. In terms of predictive power, we find that an expansion in firm debt can be just as significant as household debt for predicting crises, if not more so, and it also predicts the depth of the post-crisis recession.

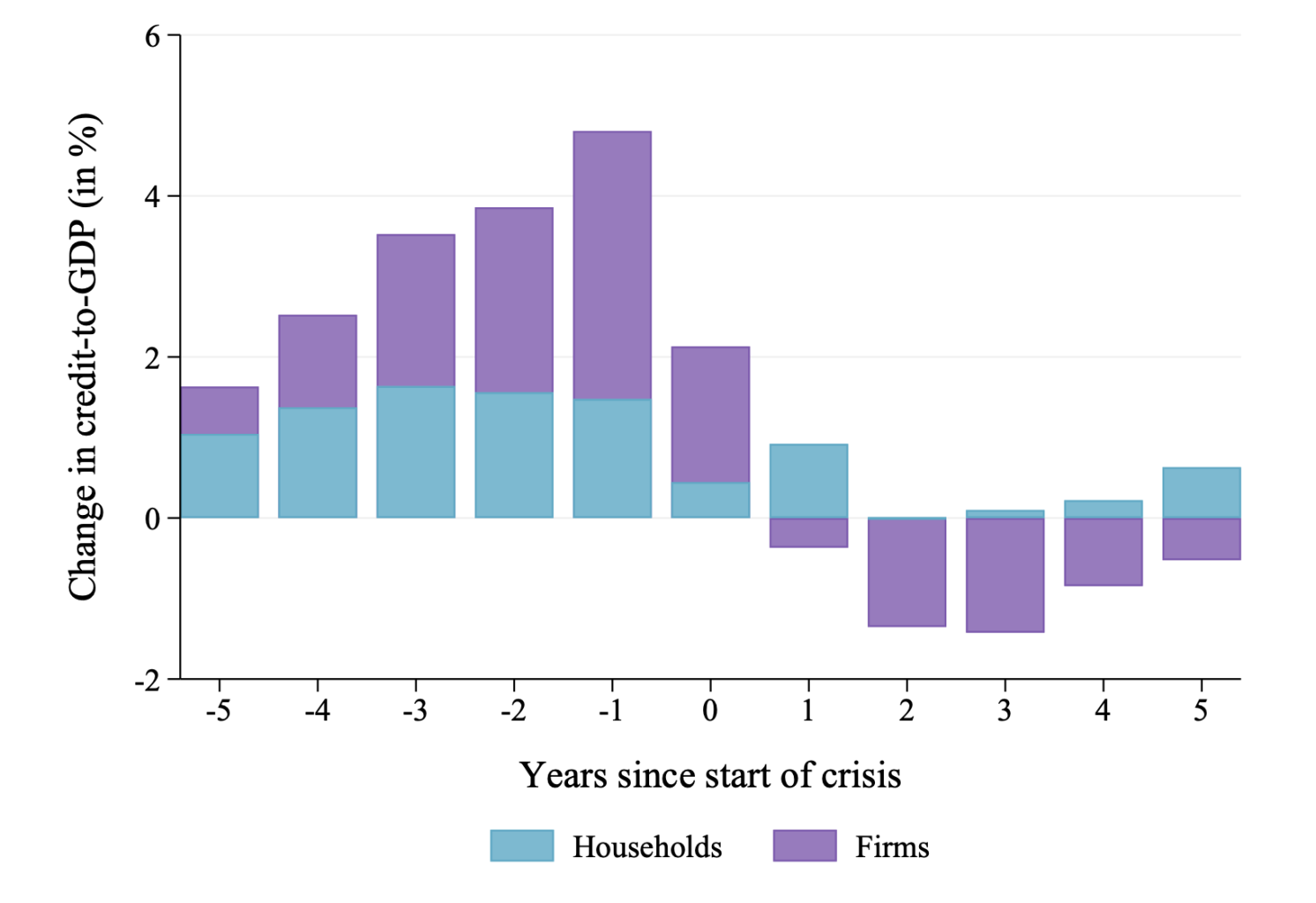

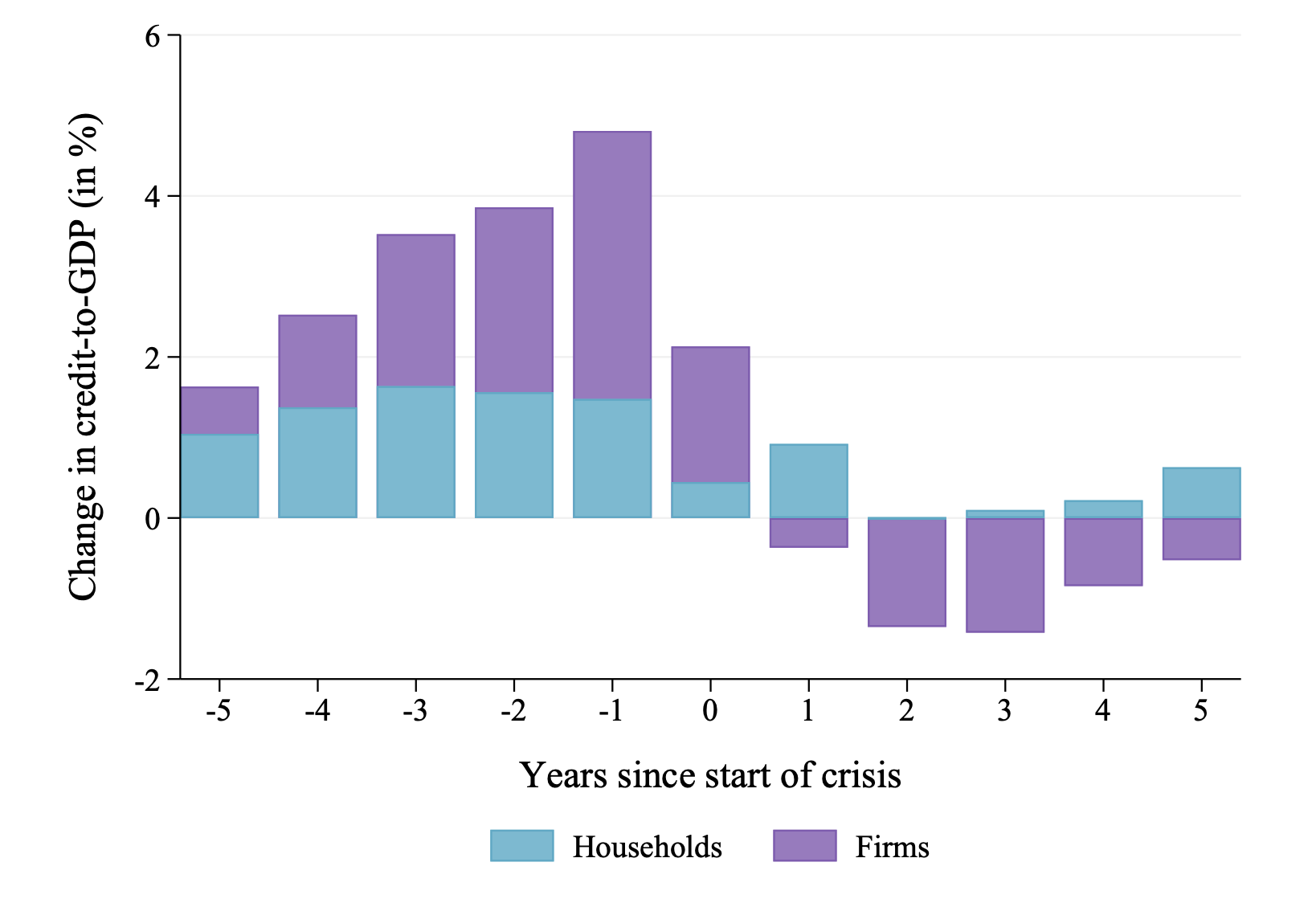

The main result of the paper is summarised in Figure 1. The figure clearly shows that, although household and firm credit each contribute to credit growth in the years leading up to the crisis, the decline in credit growth following the crisis is entirely concentrated in the firm sector. These results contrast sharply with the patterns for household debt, which continues to grow relative to GDP even after a financial crisis has started, and tends to account for only a small fraction of nonperforming loans after crises.

Figure 1 Decomposing credit growth around financial crises

Notes: This figure decomposes changes in total credit-to-GDP around the onset of 87 systemic financial crises, where we identify the first year of a crisis based on the chronologies in Baron et al. (2020) and Laeven and Valencia (2020). We plot the average change in credit-to-GDP for each sector (households or firms) in a five-year window around crises. By definition, the sum of the sectors is equal to total credit.

To understand the underlying mechanisms linking firm debt and crises, we make use of the sectoral variation in our data and exploit the fact that sectors vary in their dependence on different types of collateral. Consistent with the existing literature linking real estate collateral values to firm behaviour (e.g. Chaney et al. 2012, Bahaj et al. 2020), we find that lending to firms relying on real estate as collateral, such as those in the construction sector, has a relatively stronger association with crises. A one standard deviation increase in real estate-backed firm credit relative to GDP over the past three years is associated with a 3.7 percentage point increase in the probability of a financial crisis within the next three years. We find a similar result for credit to the non-bank financial sector, which, as we show, tends to lend to non-financial firms. These findings suggest that corporate debt expansions contain important information about future economic crash risk.

The sectoral variation of our data also allows us to examine whether bad credit booms are times when some sectors grow ‘out of whack’. We show that the dispersion of credit across sectors systematically increases during credit expansions. This stylised fact, which suggests heterogeneous easing and tightening of financial constraints across sectors, mirrors the role of heterogenous credit constraints documented in firm-level data (e.g. Ottonello and Winberry 2018, Caglio et al. 2021). Our proposed measure of dispersion predicts crises over and above the size of the credit expansion, as measured by changes in the credit-to-GDP ratio. In our benchmark specification, a one standard deviation increase in dispersion predicts a 3.6 percentage point increase in the probability of a crisis. Our interpretation is that, even in the case of two credit booms of the same magnitude, disproportionate growth in credit flowing to some industries signals heightened risk-taking in certain sectors, with potential implications for the overall stability of the financial system.

We also examine whether firm debt matters for sluggish post-crisis recoveries using local projections (Jordà 2005). In particular, we study how the path of real GDP per capita depends on the type of credit extended before the downturn. Again, we find that corporate debt is important for macroeconomic dynamics. Corporate debt not only makes financial crises more likely; it also prolongs the recovery from the recessions that usually follow, and this result is particularly strong for corporate debt backed by real estate collateral.

We link this sluggish recovery to deterioration in asset quality. Using newly collected data on nonperforming loans (NPLs) by sector, we show that firms, rather than households, account for three-quarters of total NPLs on bank balance sheets after crises. We also find that firm defaults in sectors using real estate collateral are particularly likely to spike during banking crises. Finally, we show that corporate debt booms are particularly predictive of post-crisis increases in aggregate NPLs, especially when backed by real estate collateral, while we find a more muted role for household debt expansions.

Why do our results differ from existing work that finds a limited role for firm debt (relative to household debt) in economic fluctuations? The main reason is that we use a more comprehensive dataset covering a broader set of countries, giving us around three times the country-year observations compared to previous work. Moreover, exploiting data disaggregated by industry allows us to document a more granular and robust link between firm credit and financial crises.

Taken together, our findings suggest an important role for corporate debt in understanding credit cycles, with implications for models of macro-financial linkages and the design of macroprudential policy, which thus far has focused almost exclusively on banks and households.

Source : VOXeu

.jpg")

")

")

.jpeg")

")

")

")

")

")

")