The WTO has noted that trade scepticism among policymakers and trade policy tensions over supply chains are manifesting themselves in even more fragmented and concentrated supply chains. This column develops a model to show how trade policy uncertainty deters the investment needed to facilitate integration into global value chains, and demonstrates how WTO agreements, by acting as a commitment device, lower this uncertainty and thus encourage investment and integration. Any erosion of the WTO’s credibility or destabilistion in the global trading environment can have long-term implications for global supply chains.

US-China trade tensions, the COVID-19 pandemic, and national security concerns have exposed several risks in current global supply chains (Freeman and Baldwin 2022, Alfaro and Chor 2023). The response from governments and firms worldwide has focused on investments to make these supply chains more ‘resilient.’ 1 Another approach is directly targeting the policy shocks, for example by renewing cooperation in trade policy and mitigating systemic uncertainty about future policies.

Cooperation via the WTO has, until recently, successfully reduced trade policy uncertainty (TPU), which has been an important source of export growth (Handley and Limão 2022). However, the credibility and enforcement of commitments in the WTO are currently diminished (see, for example, Wolff 2022 on dispute settlement). The WTO itself notes that trade scepticism among policymakers and trade policy tensions over supply chains are manifesting themselves in even more fragmented and concentrated supply chains (WTO 2023). Before abandoning hope of renewed cooperation in this area we must answer the following. What is the value of WTO commitments along the global supply chain?

In a new paper (Handley et al. forthcoming), we start to address this question. Specifically, we model and estimate firm input sourcing decisions under TPU and use the framework to estimate the value of WTO commitments made by China upon accession. The reduction in TPU increased investments in new imported inputs within firms and made them more responsive to future trade liberalisation. This translated into higher final sales. These impacts from lower TPU – a more responsive demand for prices and diversified supplier portfolio – are in line with the rhetoric of policymakers and firms but undermined by the tensions in the WTO and in some regional agreements.

China’s WTO accession and imports of intermediate inputs

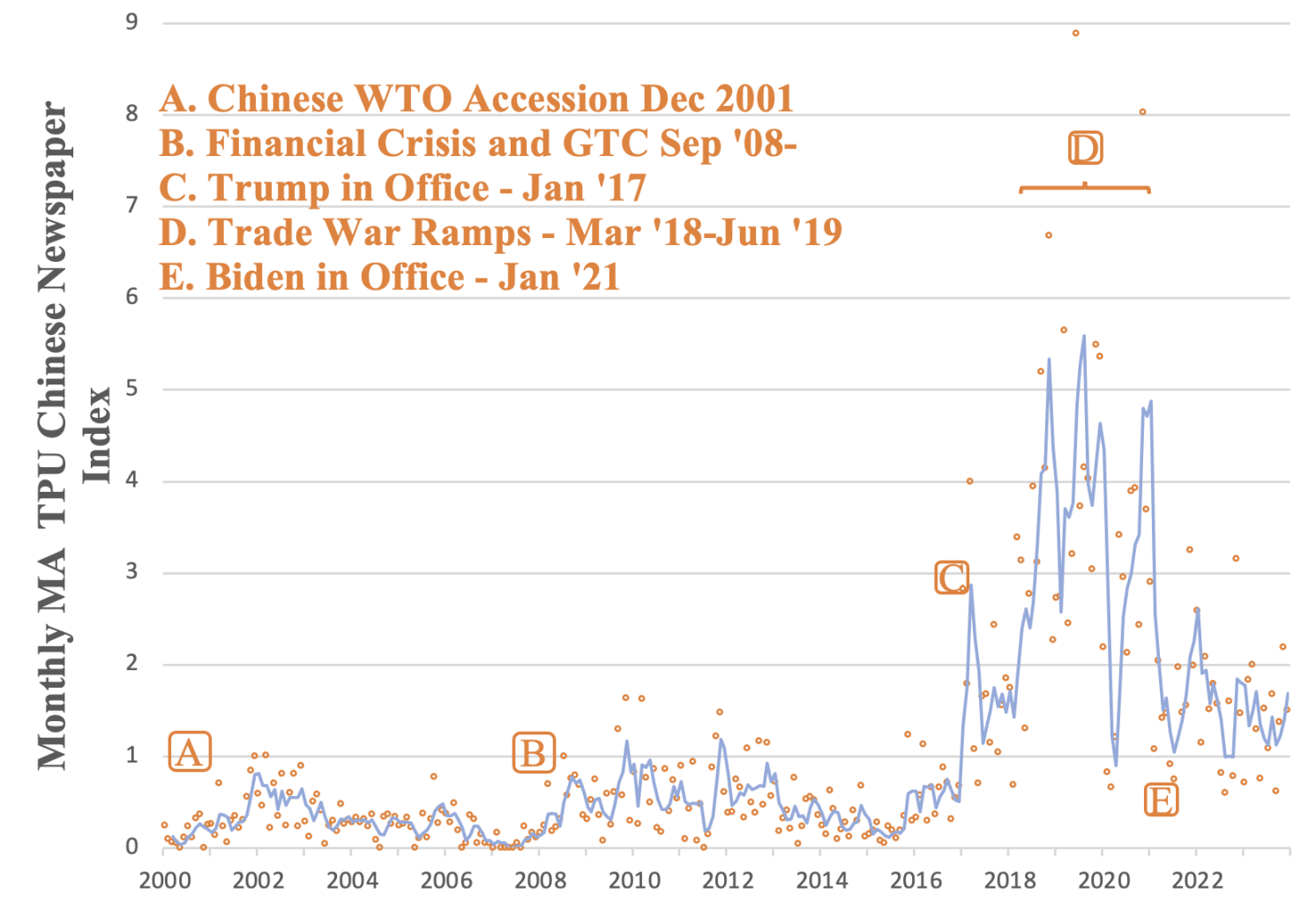

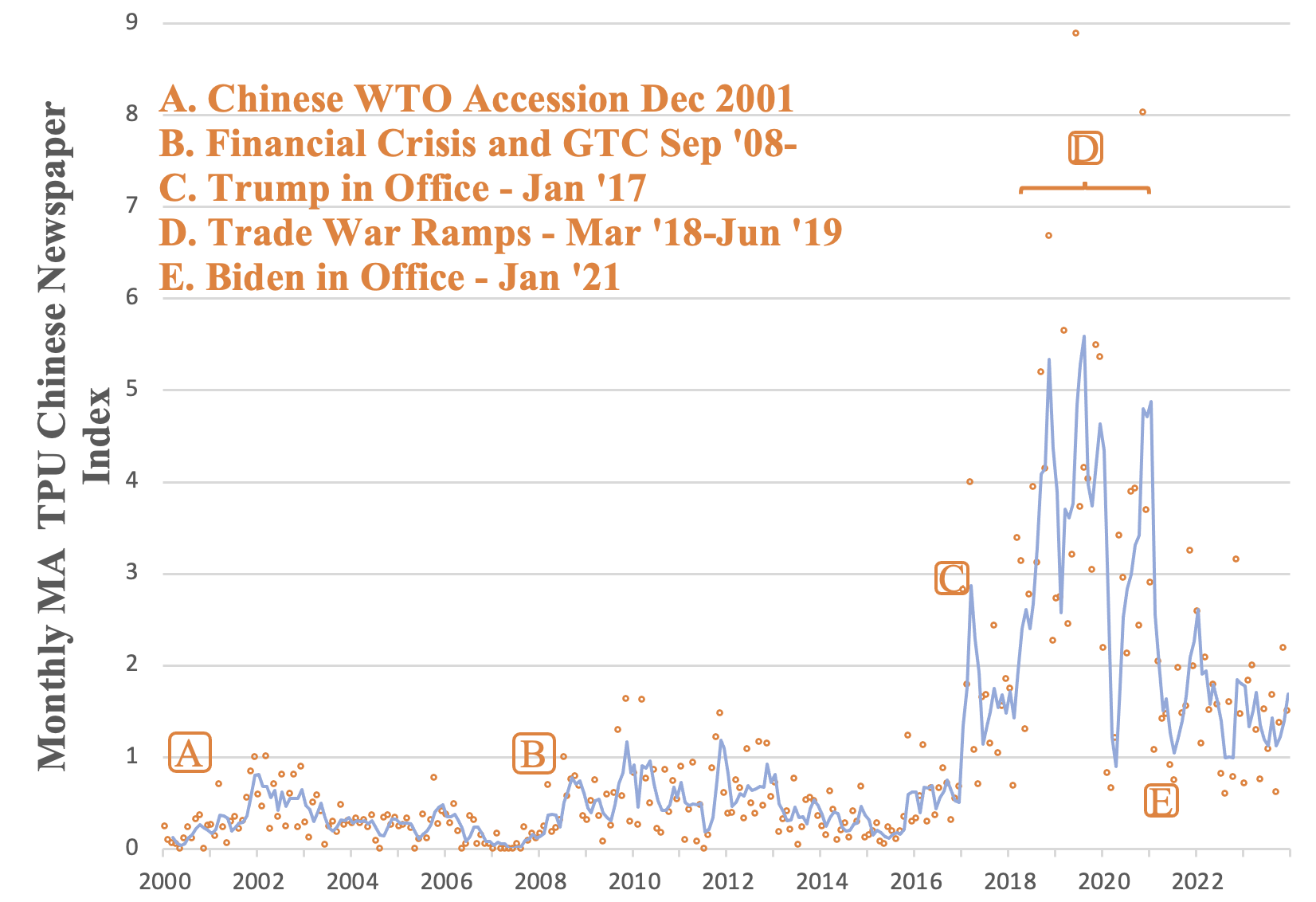

TPU can be challenging to measure systematically over long periods. A useful descriptive tool is an index such as the one in Figure 1, constructed with the measure by Davis et al. (2019) of the frequency of Chinese language newspapers about TPU. We note a couple of features to provide context and illustrate the current importance of TPU. First, there is a reduction in this index after China’s WTO accession, which included its commitment to previous tariff reductions. Second, there is an increase in the 2008 crisis, which eventually subsided but at a higher level than before. The index rises again during Donald Trump’s presidential campaign and spikes with his entry into office and successive threats and implementation of tariffs on Chinese intermediates and subsequent retaliation. Since 2021, TPU has subsided relative to those peaks but remains elevated.

Figure 1 China’s TPU News Index, 2000-2022

Source: Authors based on data from Davis et al. (2019).

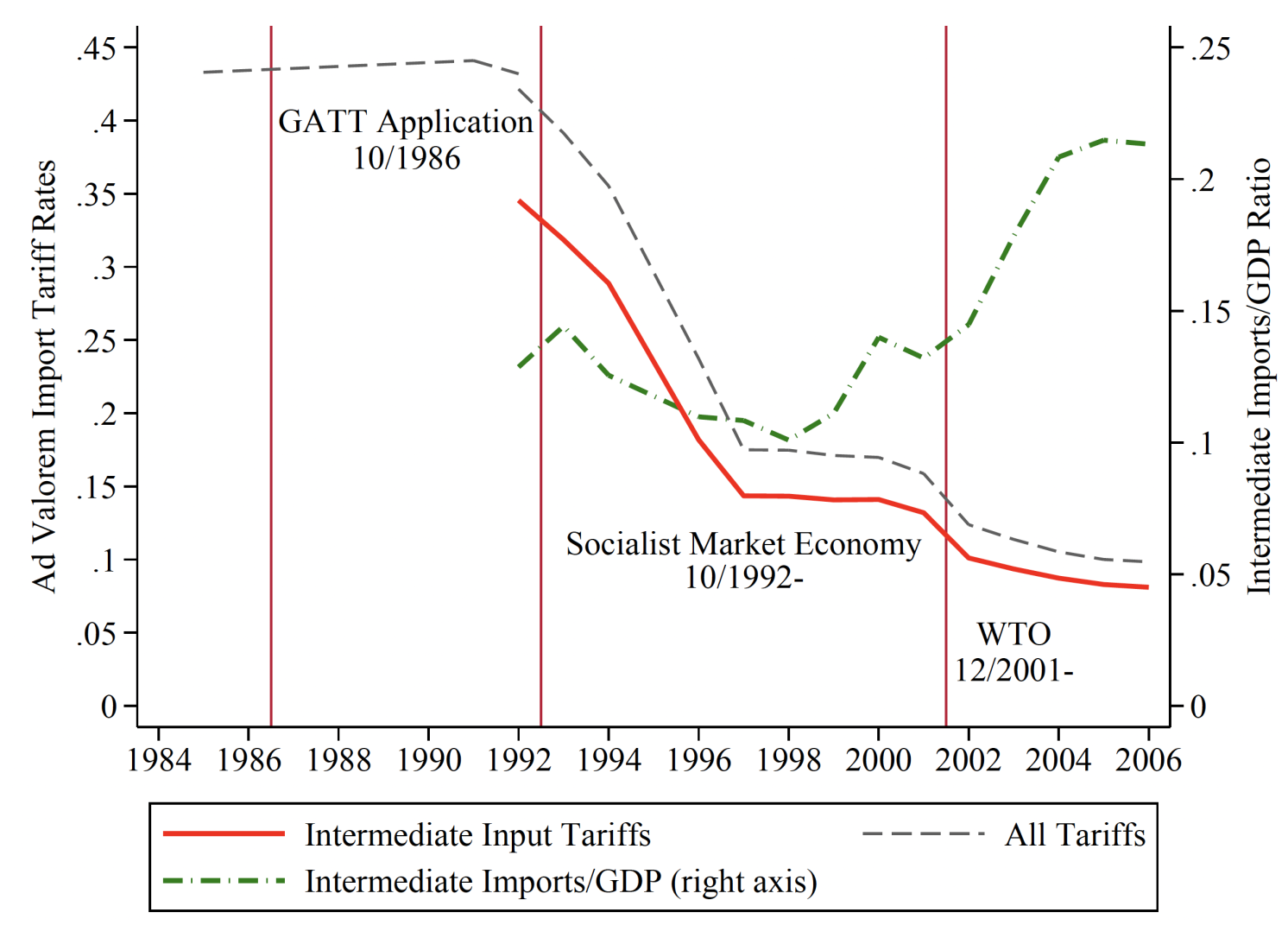

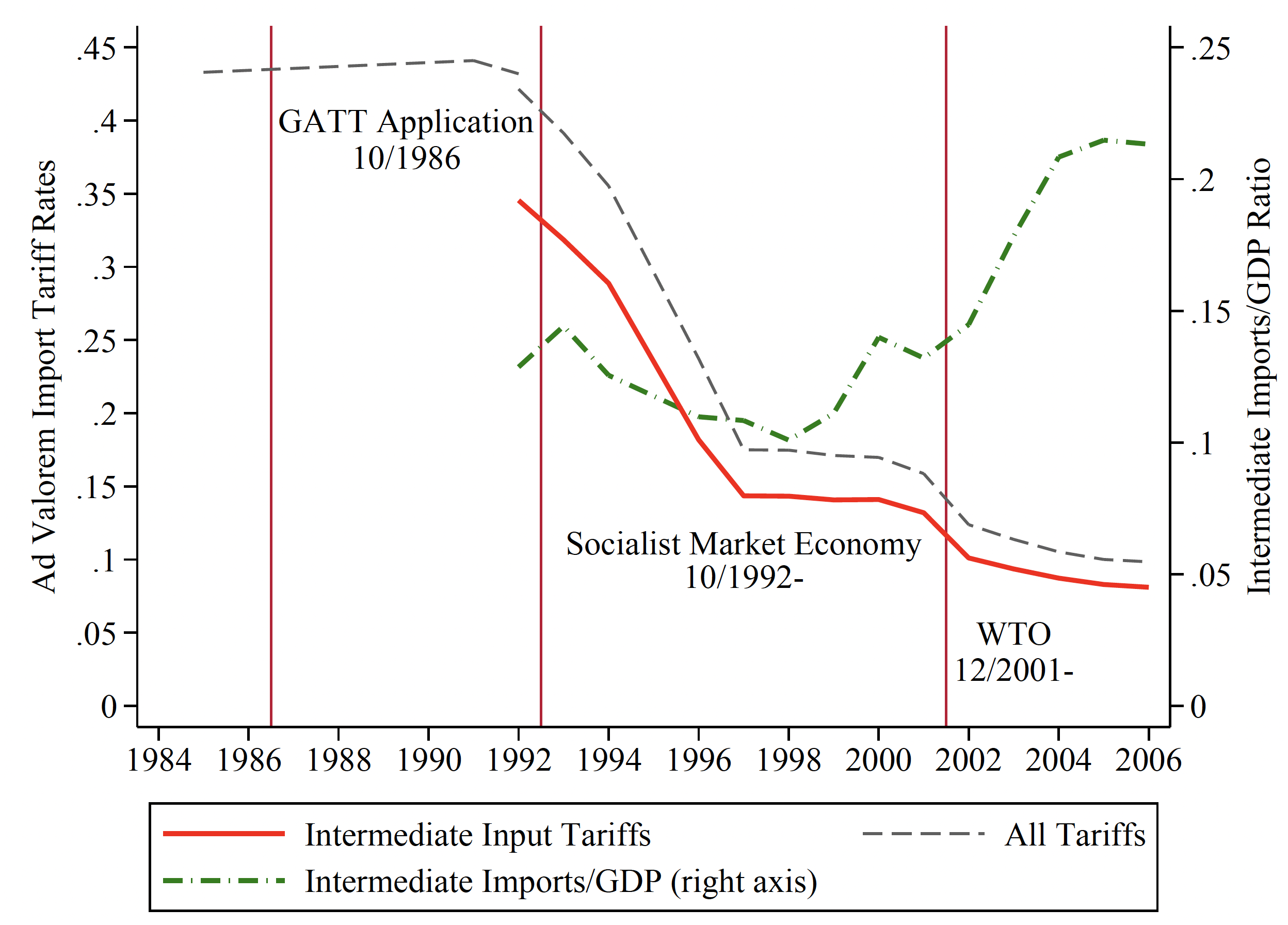

China started its process of trade liberalisation in 1992 with the introduction of the ‘Social Market Economy’ concept and the signing of the US-China memorandum of understanding on market access. Tariffs placed by China on intermediate goods quickly fell following these events. Figure 2 shows China’s average most favoured nation (MFN) rate declined from 35% in 1992 to around 12% in December 2001, when it entered the WTO, and was below 10% in 2006. The substantial liberalisation pre-WTO was not reflected in higher intermediate import shares relative to GDP, which fell between 1992 and 1998. This share did increase in a significant and sustained form after WTO entry, even though the tariff cuts were smaller in that period.

One hypothesis for these facts is that Chinese importers believed the tariffs between 1992-1998 could be changed in the future without commitment through an agreement such as the WTO. The resulting tariff uncertainty lowered their investment in imported inputs. Under this hypothesis, the WTO accession lent credibility to the earlier liberalisation and thus spurred Chinese firm imports. We find that a significant fraction of the WTO impact on Chinese imports is due to this commitment mechanism, rather than the reduction of Chinese tariffs between 2000-2006, which many other studies emphasise.

Figure 2 China’s average applied import tariffs and intermediate imports/GDP

Source: Handley et al. (forthcoming).

Why would Chinese import decisions depend on uncertainty about future tariffs? Firms require investments to adopt a new intermediate import; if the future tariff and thus the price of that product are uncertain, then the firm may wait and see (i.e. we would observe lower investments in inputs facing higher TPU). Our model predicts that the firm’s imported input values and its operating profits decrease in applied tariffs and tariff uncertainty. We decompose the TPU effect into a substitution channel (reductions in import tariff risk of an input raises international sourcing vis-a-vis domestic) and a scale channel (increasing profits and thus adopting other imported inputs).

Testing the model

To test the model’s predictions, we employ Chinese transaction-level firm data for 2000-2006 and MFN statutory tariffs for 1992-2006. While aggregate time-series measures of TPU like the one plotted in Figure 1 are important for understanding broader levels of uncertainty for the whole economy, our approach uses more detailed cross-section variation from the difference of applied MFN and the historical tariffs from the mid-1990s before China began the process of liberalisation. If China’s bid to join the WTO had failed, firms may have placed some weight on the possibility of reversion to these higher tariffs. Therefore, we measure tariff risk in a given year by the ratio of the average Chinese MFN historical tariffs before joining the WTO relative to the applied tariffs in each product and year.

Our key empirical findings are as follows:

- Chinese tariff decreases on an intermediate input increase a firm’s imports; that tariff elasticity is stronger in the post-WTO period, as previous reductions gain credibility.

- Tariff risk reduced firms’ imports before accession but much less afterwards, as firms placed lower probability on a tariff reversal.

- We find applied tariff and risk effects operate via the substitution and scale channel and are stronger for more productive firms in any industry.

- The probability of imported input adoption after the accession is higher for products previously facing higher tariff risk.

These results are robust to different firm samples, risk measures, sources of TPU, and alternative explanations.

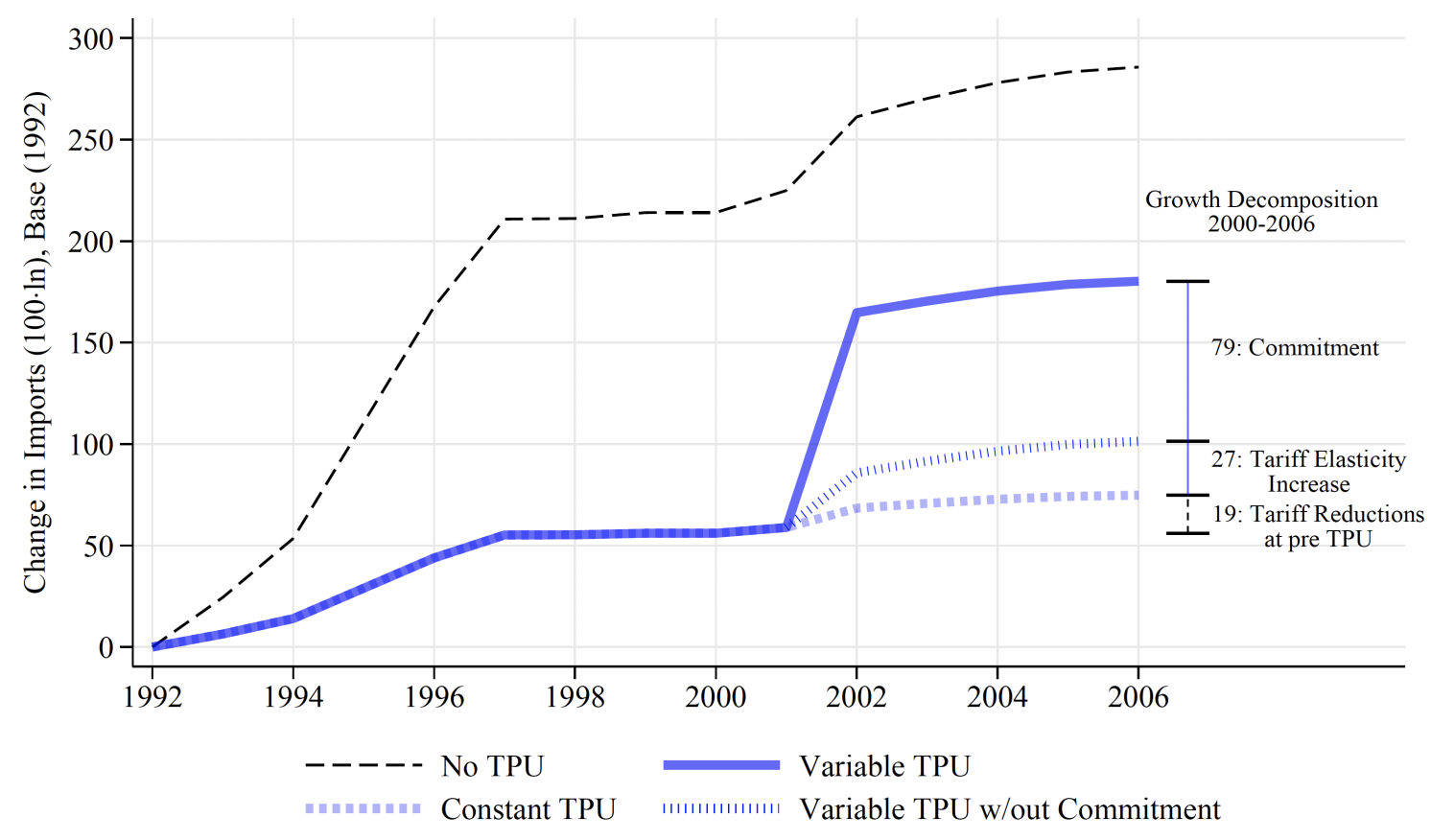

Counterfactual effect of WTO accession on firm’s imports and performance

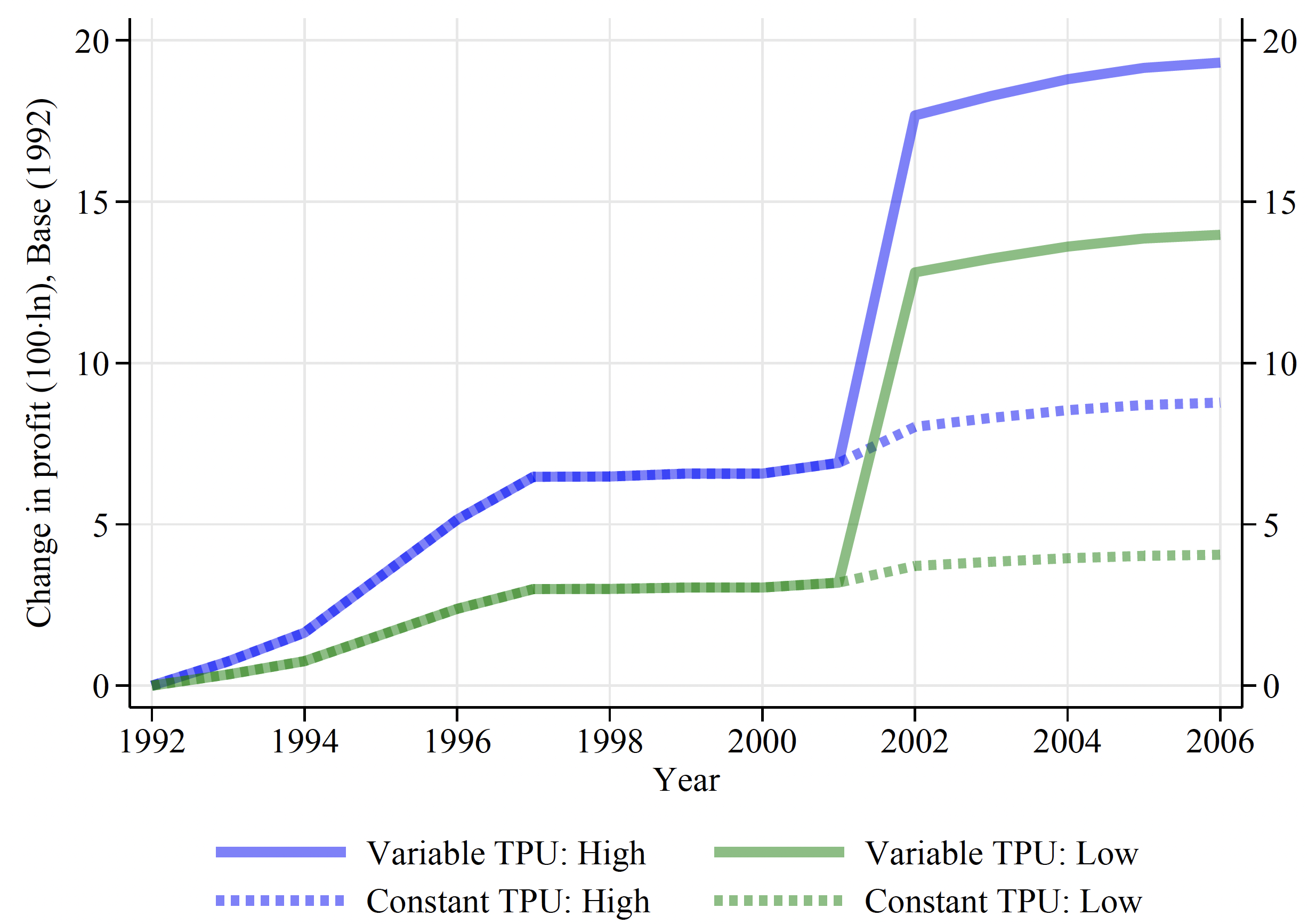

To quantify the role of WTO commitments, we use the empirical elasticities and compute three policy counterfactuals: (1) no TPU over all years, (2) constant TPU at estimated pre-accession level, and (3) lower TPU after accession.

Figure 3 Counterfactual intermediate input growth and decomposition

Source: Handley et al. (forthcoming)

The results of the counterfactuals are illustrated in Figure 3. We found that the tariff reductions between 1992 and 2000 would have increased imports by an additional 158 log points had there been no TPU. If TPU had remained constant after the WTO accession, then the 5% tariff reduction in 2000-2006 would have grown imports by only 19 log points. Under the last scenario, where TPU also falls, the tariff reductions in 2000-2006 have a stronger impact, an additional 27 log points. The commitment effect accounts for the remaining gap of 79 log points.

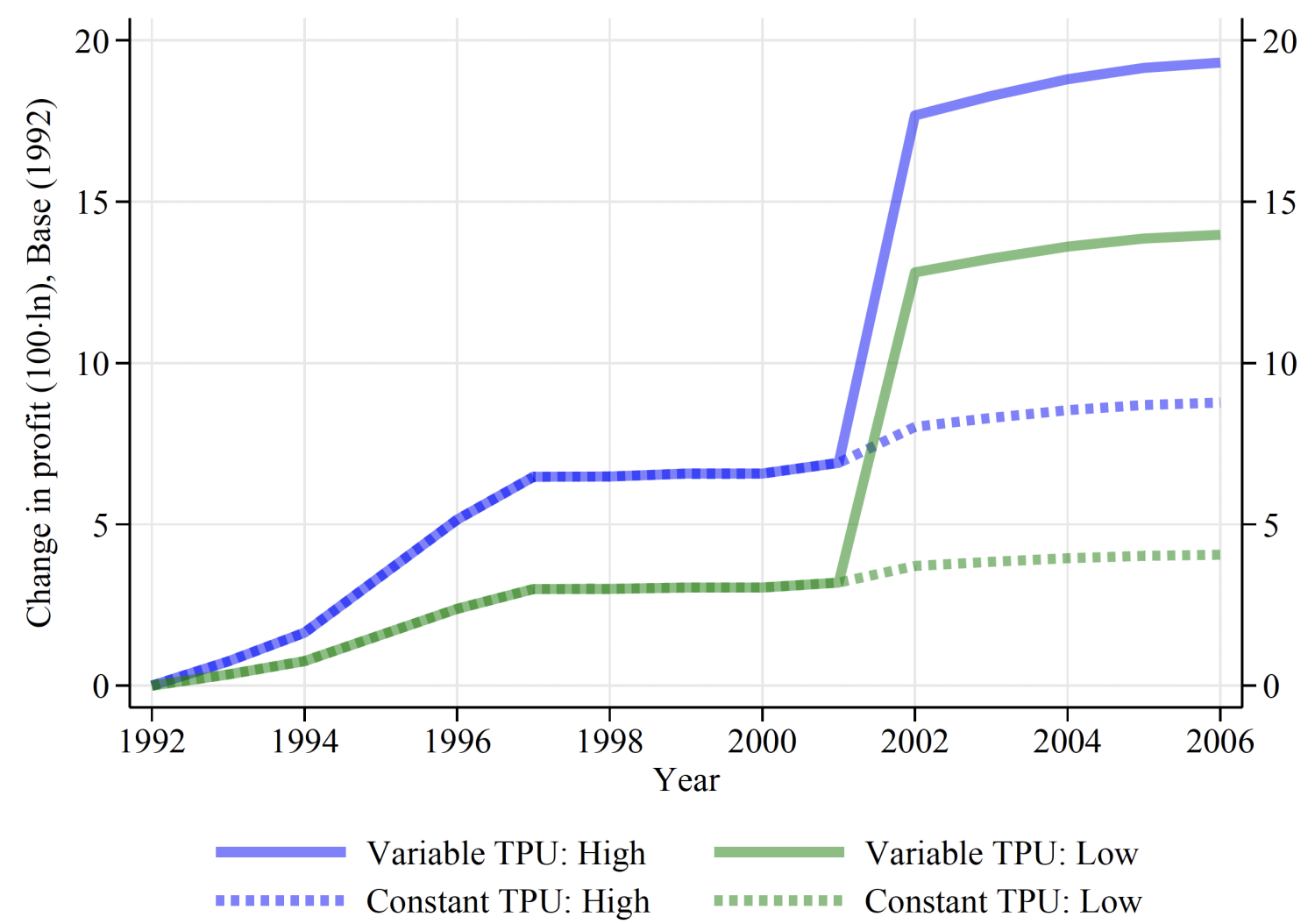

Our model also predicts that more productive firms are more responsive to tariff and TPU shocks. We verify this empirically, and in Figure 4, we illustrate how it translates into sales (or, equivalently, operating profit in this model). As in Figure 3, we show the outcome if TPU was unchanged using dots. The liberalisation had a more significant impact on high-productivity firms (purple) than others (green). More importantly, the growth in profits via intermediate imports was driven mainly by TPU reductions, as shown by the gap between the solid and dotted lines after 2001.

Figure 4 Counterfactual profit and sales growth by firm profit

Source: Handley et al. (forthcoming).

Conclusion

In summary, this research provides a theoretical framework and empirical evidence that capture the value of WTO commitments on tariffs to firms’ decisions to adopt and import intermediate inputs.

Although China’s accession happened more than 20 years ago, our findings shed light on the impact of more recent trade tensions, such as the US-China trade war, Brexit, and the hand-wringing of policymakers over national security and critical supply chain inputs. Our results suggest that the reduced credibility of regional and multilateral trade agreements may have a depressing effect on investment in new intermediate input sourcing decisions. These effects may persist even after the threats are reduced or resolved if firms believe future trading environments are less stable and unpredictable.

Source : VOXeu

.jpg")

")

")

.jpeg")

")

")

")

")

")

")