The design of monetary policy has traditionally considered aggregate total factor productivity as an exogenous variable over which the central bank has no control. This column argues that monetary policy can affect aggregate productivity through the allocation of capital. In the face of an expansionary monetary policy shock, firms with a high marginal product of capital increase their investment relatively more than firms with a low marginal product of capital, leading to better overall allocation of capital, and thus productivity. This finding suggests that central banks should take account of the broader implications of their decisions for the supply side of the economy.

The design of monetary policy has traditionally considered aggregate total factor productivity (TFP) – the efficiency with which inputs are combined to produce output – as an exogenous variable over which the central bank has no control. From this perspective, the role of the central bank is to take the supply side as given and manage the demand side of the economy to achieve its mandate.

At the same time, it has been widely documented that the allocation of resources among firms is an important determinant of aggregate TFP (e.g. Restuccia and Rogerson 2017). Ideally, resources such as capital should be employed in those firms where these resources add most value. Deviations from this ideal allocation reduce TFP and are referred to as misallocation. The allocation of capital is determined by the investment choices of individual firms. Those choices in turn are influenced by monetary policy. If changes in monetary policy differently impact investment decisions across firms, then – in contrast to the traditional view – monetary policy affects the allocation of capital and TFP. This potentially creates new trade-offs for central banks, suggesting central banks should take account of the broader implications of their decisions for the supply side of the economy, particularly during periods of active monetary policy such as the recent inflationary episode.

The capital misallocation channel of monetary policy

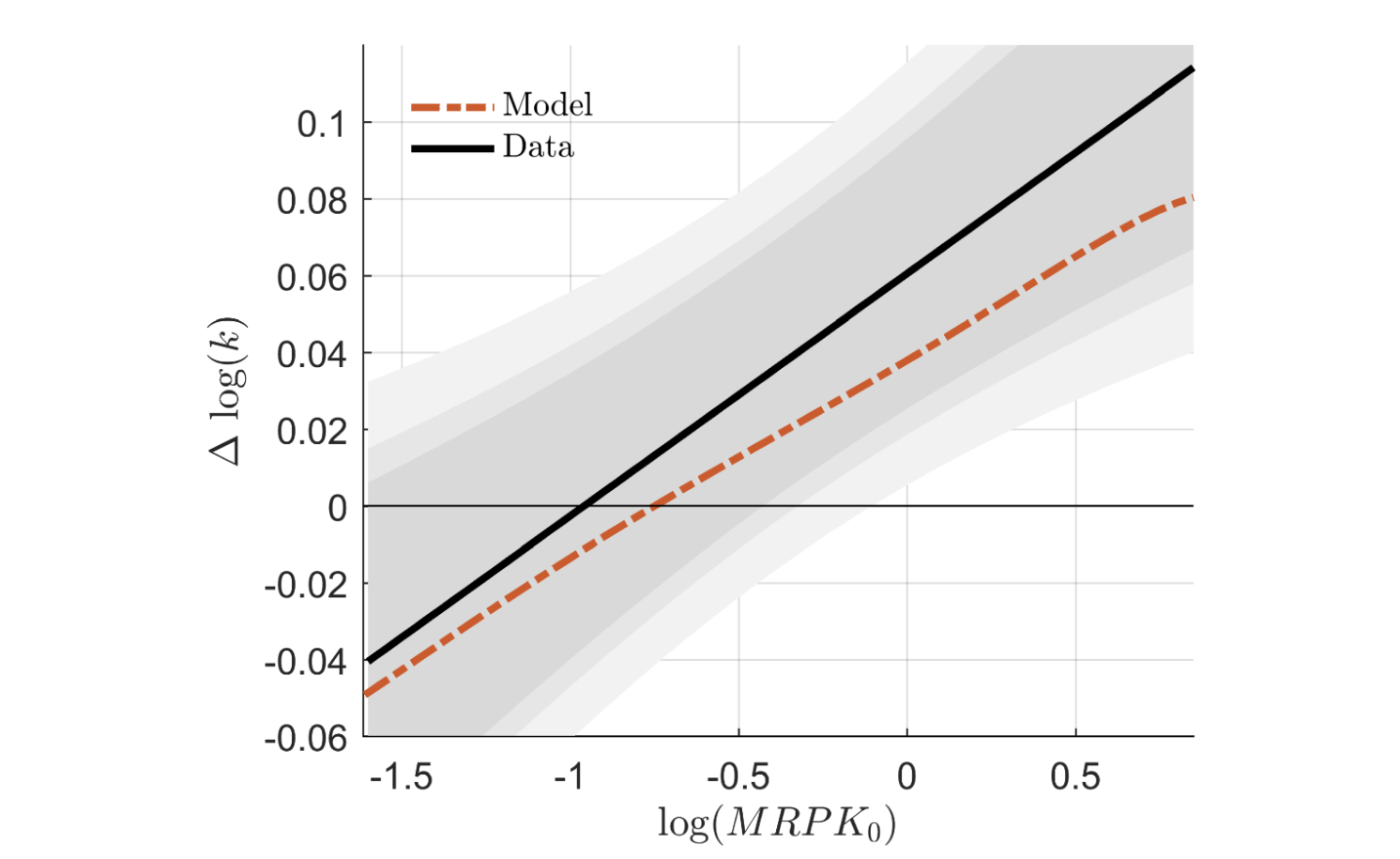

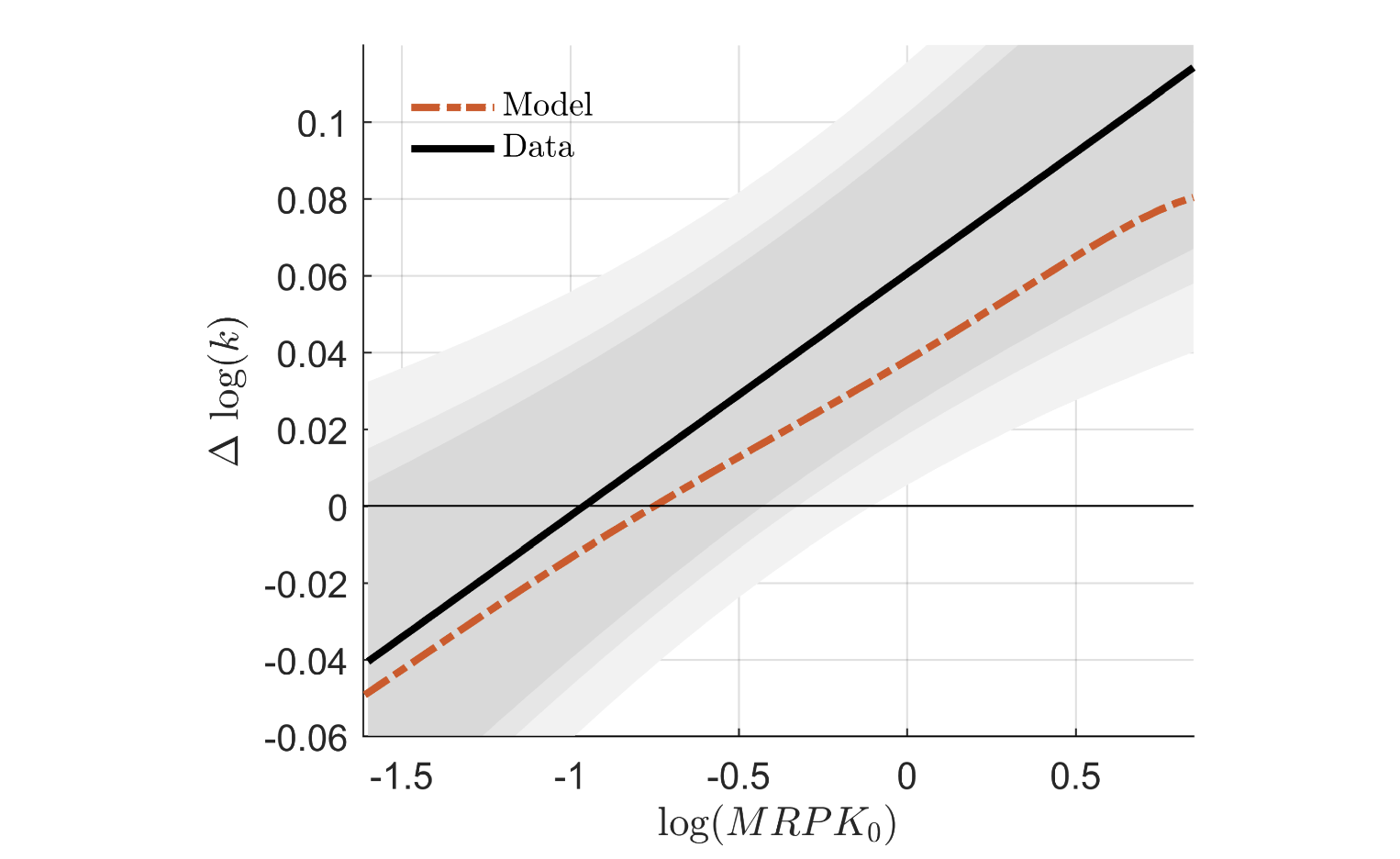

In a recent paper (González et al. 2024), we explore the relationship between monetary policy and capital misallocation, putting forward a new mechanism through which the central bank can affect TFP, and studying its implications for optimal monetary policy. We combine data on Spanish firms with monetary policy shocks identified using the high-frequency approach of Jarociński and Karadi (2020). We document that in response to an expansionary monetary policy shock, firms with a high marginal product of capital (i.e. those firms where an extra unit of investment creates most additional value) increase their investment relatively more than firms with a low marginal product of capital (Figure 1). Combining the individual firm responses into a new measure of aggregate misallocation, we find that the allocation of capital improves in the face of an expansionary monetary policy shock. We call this result ‘the capital misallocation channel of monetary policy’.

Figure 1 Response of investment to an expansionary monetary policy

Notes: The figure displays the average effect of a 1-percentage-point expansionary monetary policy shock on the growth rate of the capital stock in the year after the shock, as a function of the firms’ logarithm of the marginal product of capital (log(MRPK)) before the shock. We compare the model prediction (dashed orange line) with the estimated relationship in the data (solid black line). The shaded areas mark the 90%, 95%, and 99% confidence intervals.

A theoretical framework

To understand this result, we propose a model that combines the workhorse New Keynesian model with a model of firm heterogeneity, where financial frictions lead to a suboptimal allocation of capital among firms with differing levels of productivity (see, for example, Moll 2014). These financial frictions limit the borrowing capacity of firms, preventing the most productive firms from growing to their optimal size.

This economy resembles the standard New Keynesian model with capital, except that in this case, TFP is endogenous. The dynamics of TFP are determined by the evolution of the distribution of capital among firms, which in turn depends on the evolution of wages, prices, and interest rates.

We calibrate the model to replicate key firm-level statistics of Spanish firms. The allocation of capital in the model economy improves following an expansionary monetary policy shock. This is because the policy expansion creates a temporary economic boom that increases corporate profits, favouring in particular the most productive firms. The increase in profits helps to overcome financial frictions, allowing high-productivity firms to increase their investment more than low-productivity firms. As a result, high-productivity firms use a larger share of the aggregate capital stock, reducing misallocation and pushing up TFP over the medium term. The model can thus rationalise the empirical evidence discussed above.

Optimal monetary policy

If the central bank can affect aggregate productivity, this introduces an additional trade-off alongside the standard trade-off between inflation and economic activity. How should monetary policy operate in this case? To answer this question, we analyse optimal monetary policy.

We first show that the capital misallocation channel introduces a new source of time inconsistency: if a central bank is not bound by any previous commitment, such as to the objective of price stability, it could be tempted to engineer a temporary economic boom through expansionary monetary policy to increase aggregate productivity in the medium run, before returning to the pursuit of price stability in the long run. Such a policy appears attractive in the short run, but it fails if economic agents anticipate it, in which case it would only lead to more inflation but none of the intended benefits for productivity.

We then analyse optimal monetary policy from a ‘timeless perspective’ (Woodford 2003). That is, we consider a central bank that sticks to an optimal policy rule and does not give in to time-inconsistent temptations of the type described above. In this case, the central bank optimally sticks to price stability even in the face of economic disturbances such as demand shocks, financial shocks, or TFP shocks. There is thus no meaningful trade-off between price stability and managing capital misallocation, just as the standard New Keynesian model features no trade-off between price stability and aggregate demand management (this is commonly known as the ‘divine coincidence’).

However, the implementation of the optimal policy differs from the standard New Keynesian model: greater changes in policy rates are now needed to stabilise inflation. This is because the endogenous response of TFP amplifies the volatility of natural interest rates, that is the level of the interest rates consistent with price stability. In this respect, there are significant implications when interest rates are near the zero lower bound, as the standard policy of keeping interest rates ‘low for longer’ (Eggertsson and Woodford 2004) becomes a ‘low for even longer’ policy.

Conclusions

Our analysis shows that monetary policy may affect aggregate productivity through the allocation of capital. In this respect, our mechanism is complementary to others such as innovation (Benigno and Fornaro 2018, and Grimm et al. 2021) or differences in price mark-ups (Farhi et al. 2021, and Meier and Reinelt 2022). Recent empirical studies support this positive link between monetary policy and TFP (see, for example, Jordà et al. 2023). Our study of optimal monetary policy in the presence of substantial differences across firms enriches the emerging literature that is moving away from the representative agent paradigm and towards heterogenous agent models for formulating optimal policies (for example Bhandari et al. 2021, and Dávila and Schaab 2023).

Source : Voxeu

")

")

.jpeg")

")

")

")

")

")

")