Japan produces and exports a sophisticated basket of machinery and capital goods. Following the global crisis, it offshored manufacturing of parts and components to Asian countries. This column studies the impact of exchange rate fluctuations on Japanese exports since 1990. It finds a strong effect between 1990 and 2010, when an appreciation of the yen by 10% would reduce machinery exports by 6%. However, since 2010, total machinery exports are less sensitive to exchange rates, particularly exports to Asian countries. However, a depreciating yen boosts the profitability of Japanese manufacturers and their exports to non-Asian countries.

Japan produces and exports high-quality machinery and capital goods. These include excavators, machine tools, turbines, robots, machinery to manufacture semiconductors and textiles, and other capital goods. Japan has traditionally played an important role in exporting these goods to downstream Asian countries. Kwan (2004) noted that if Asian firms are unable to obtain capital goods from Japan, they are frequently unable to obtain them at all. What factors influence the ability of downstream firms to obtain these vital inputs?

Sophisticated exports and exchange rate elasticities

Japan’s exports are sophisticated. Using Hidalgo and Hausmann (2009) complexity measures, Japan’s export basket has been rated as the world’s most sophisticated in every year between 2000 and 2021. The Japanese machinery export basket is also more sophisticated according to the Hidalgo and Hausmann measure than the machinery exports of other leading exporters such as China, the US, and Germany.

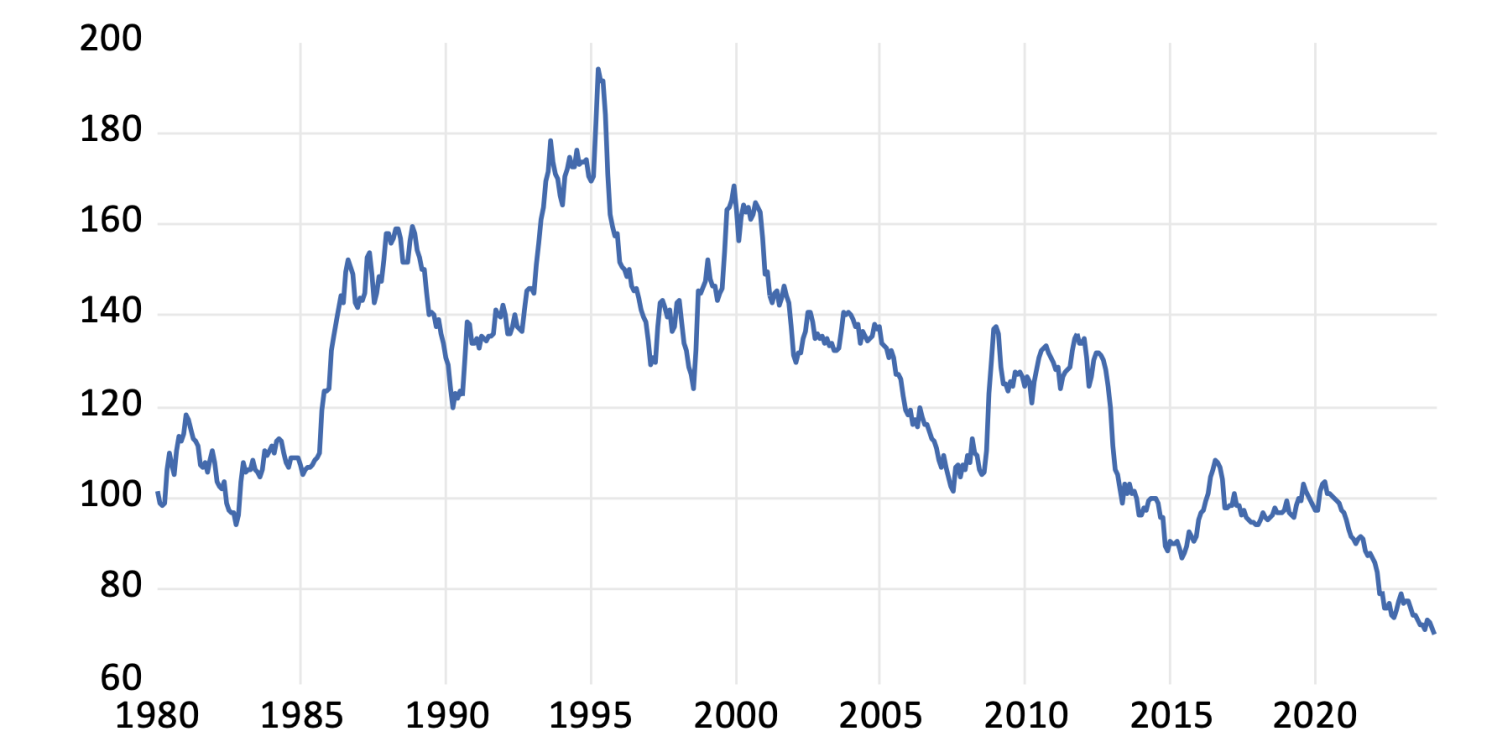

Are these sophisticated exports sensitive to exchange rates? This question is relevant as the Japanese real effective exchange rate in 2024 is at its lowest level over the 44-year period for which the Bank of Japan provides data (see Figure 1). Abiad et al. (2018) noted that more complex goods are harder to produce and thus have fewer substitutes. Because of this, they reasoned that the price elasticity of demand should be lower for more complex products and thus that exports of these goods should be less sensitive to exchange rates.

Figure 1 Japanese real effective exchange rate

Source: Bank of Japan.

Previous evidence has been mixed. Baek (2013), employing an autoregressive distributed lag model and quarterly data over the 1991-2010 period, reported that Japan’s machinery exports to South Korea are not affected by exchange rates in the long run. He argued that this was because South Korea relied on machinery from Japan. Sato et al. (2013), using impulse-response functions from a monthly vector autoregression over the 2001-2013 period, found that a yen appreciation decreased Japanese exports of office machinery, electrical apparatuses, and communication equipment. Thorbecke (2015), using annual data and dynamic ordinary least squares estimation over the 1982-2009 period, reported that a yen appreciation reduced Japanese capital and equipment goods exports.

Yen appreciations and the slicing up of the value chain

The period after 1982 was eventful for the Japanese economy. In 1985, to reduce the US trade deficit, Japan, France, West Germany, and the UK agreed in the Plaza Accord to let their currencies appreciate against the US dollar. From the time the accord was signed in September 1985 until the middle of 1995, the yen appreciated from 240 to the US dollar to below 88 to the dollar.

Japanese exporters lost price competitiveness. To cut costs, they relocated labour-intensive tasks to factories in the Association of Southeast Asian Nations (ASEAN) and China. Japanese final goods exports fell from 20% of world final goods exports in 1985 to 10% in 1995. Japanese outward foreign direct investment (FDI) increased from 0.5% of Japanese GDP in 1985 to more than 2.5% by the end of the decade. Asia was a dominant recipient of this FDI (Urata and Kawai 1999). Japanese exports of intermediate and capital goods (ICG) to China and ASEAN increased from 28% of Japanese intermediate and capital goods exports in 1985 to 40% in 1995. China and ASEAN’s exports of final goods increased from 3% of world final goods exports in 1985 to above 10% in 1995.

Bayoumi and Lipworth (1998) found that the motive for Japanese FDI at this time was vertical integration, where subsidiaries in other countries became part of the production process. Yoshitomi (2007) described the trade that accompanies this vertical FDI as vertical intra-industry trade (VIIT). Under vertical intra-industry trade, firms slice the value chain across developed, emerging, and developing countries based on comparative advantage. Each region’s comparative advantage is determined by its endowment of capital and skilled and unskilled labour and by its physical and institutional infrastructure.

Sasaki et al. (2022) observed that when the yen appreciated during the 2008-2009 Global Crisis, Japanese multinational corporations (MNCs) continued to relocate manufacturing overseas. This helped to offset the loss of price competitiveness from the appreciating yen. Then, as the yen began depreciating in 2012, rather than reshoring production, Japanese firms continued to produce abroad. Sato and Shimizu (2015) noted that for several decades Japanese firms increased overseas production. Their production networks were centred in Asian countries. As the yen appreciated during the global crisis, these firms accelerated the division of labour by relocating even more production to Asia. Because of this, Sato and Shimizu noted that a weaker yen no longer stimulates machinery exports to the same degree, because an increase in exports increases imports of parts and components from overseas subsidiaries in Asia.

If production of parts and components has been relocated to Asian countries, then the yen exchange rate would have less of an impact on Japanese exports to these countries. A depreciation of the yen against the currency of an Asian country that provides parts and components to Japan would increase the yen costs of these imported inputs. This increase in costs would mitigate the increase in price competitiveness arising from the impact of a weaker yen on Japanese value-added exported back to that country. Thus, if Japan has offshored more production to Asian countries after the global crisis, a yen depreciation against an Asian country’s currency would have less of a stimulative effect on exports to that country after 2009.

Investigating how exchange rates impact machinery exports after the global crisis

I investigated whether the influence of exchange rates on Japan’s machinery exports has declined since the global crisis (Thorbecke 2024). The results indicate that for the 1990-2000 and 2000-2010 sample periods, a 10% yen appreciation would reduce machinery exports by 6%. Many individual subcategories of machinery and equipment exports also fall in response to appreciations. However, over the 2010-2020 sample period, appreciations no longer decreased total machinery exports nor exports of most of the important subcategories.

In terms of individual categories, specialised machinery and commercial vehicle exports are not affected by exchange rates during the 2010-2020 period but telecommunications equipment exports are. The fact that exchange rates do not impact specialised machinery exports after 2000 is consistent with Baek’s (2013) observation that downstream countries such as South Korea depend on machinery exports from Japan. It is also consistent with the Abiad et al. (2018) observation that price elasticities for advanced goods such as robots and semiconductor manufacturing machines should be small.

The finding that commercial vehicle exports ceased responding to exchange rate changes after 2010 reflects Nguyen and Sato’s (2019) finding that Japanese transportation equipment exporters responded to a weaker yen during the yen depreciation period that began in 2012 by pricing-to-market. This meant that, rather than lowering prices in the importing country’s currency, they chose to keep foreign prices close to constant. Thus, as the yen depreciated, they chose to increase profit margins instead of export volumes.

Telecommunications equipment exports were very sensitive to exchange rates over the 2010-2020 period. Before the global crisis, Japan was a leading producer of cellphones. However, as Sato et al. (2013) discussed, the sharp appreciation of the yen that started with the global crisis combined with the sharp depreciation of the Korean won caused Japan’s communication equipment exports to plummet and Korean communications exports to soar. Thorbecke (2023) reported that, by 2012, South Korea’s Samsung had become the largest phone manufacturer by sales. It continued to hold this position over the next ten years.

When Japanese exports are separated into those to Asian countries and non-Asian countries, exchange rate depreciations after the global crisis do not stimulate exports to Asia for all machinery exports and for most subcategories. Depreciations do, however, increase exports to non-Asian countries. For total machinery exports, a 10% depreciation increases exports to non-Asian countries by almost 6%. There is also a statistically significant relationship between exchange rate depreciations and rising exports for several subcategories. These findings are consistent with Sato and Shimizu’s (2015) hypothesis that the relocation of production to Asian countries has weakened the link between exchange rate depreciations and Japanese machinery exports to Asia.

Conclusion

Ito et al. (2023) found that Japan has moved upstream in global value chains. This involves exporting not only capital goods to firms in downstream countries but also parts and components. The research discussed in this column investigates the changing impact of exchange rates on Japanese capital goods exports. Future research should investigate how exchange rates impact Japanese exports of parts and components. Thorbecke (2008) found that during the surge of Japanese FDI to Asia after the Plaza Accord, Japanese parts and components exports to Asia continued to respond as expected to exchange rate changes. It would be interesting to investigate if this was the case during the surge in Japanese FDI after the global crisis. Future research should also investigate whether the knowledge spillovers from Japanese exports to downstream firms outside of Asia is comparable to the knowledge diffusion from Japanese trade with downstream Asian firms that authors such as Hirano (2016) documented. Finally, the extent to which Japanese machinery exporters compete with firms in other countries that produce similar goods and the extent to which they cooperate by providing vital inputs should also be investigated.

Source : Voxeu

.jpg")

")

")

.jpeg")

")

")

")

")

")

")