A successful green transition will require a major reallocation of resources away from emissions-intensive to emissions-light activities. This column assesses whether climate transition risk is priced in Europe’s equity market by analysing relative equity returns of high versus low CO2-emitting firms over the period 2005 to 2019. The authors employ several econometric models to assess the carbon risk premium both at the individual firm level and portfolio level and find that carbon intensity is negatively related to stock returns. They also find evidence, however, of increased pricing of climate transition risk after the Paris Agreement.

Climate action hiatus is considered a key threat to our global economy (WEF 2023). Record land and ocean temperatures, forest fires, and other extreme weather events brought greater attention to the risks of climate change over the last year. At the same time, investments in fossil fuels are being renewed amid a global energy crisis, while the window to limit global warming to 1.5º Celsius above pre-industrial levels is closing rapidly (IPCC 2023).

For the green transition to succeed, we need a major reallocation of resources – a shift from emission-intensive to emission-light activities. The financial sector has a role to play in supporting the green transition, but it cannot drive the required reallocation in the absence of strong government intervention (Claessens et al. 2022, Millischer et al. 2023). Long term and adequate policy making is necessary for proper externality pricing in financial markets. Carbon pricing mechanisms can be an effective form of government intervention, as long as they help to curtail carbon emissions, while preventing carbon leakage and sustaining green investments (Bustamante and Zucchi 2023, Parry et al. 2022, Trinks and Hille 2023). It is increasingly likely that such carbon pricing mechanisms will be more widely adopted. As a consequence, firms that differ in current carbon emission intensity face different exposure to climate policy risks.

The carbon risk premium puzzle

Ambitious climate policies disproportionately impact asset valuations of emission-intensive companies, because these companies would have to make costly adjustments to alter their production processes to reduce emissions or could even end up having to discontinue operations. If investors are rational and demand to be compensated for bearing additional risk in their portfolios, emission-intensive companies have to generate higher expected returns as a result of growing climate policy risk, feeding into a carbon risk premium.

Empirical evidence of the existence of such a carbon risk premium is however highly mixed. Studies that look at the effects of policy announcements often find that stock prices of carbon-intensive firms react to the expectation of stricter climate policies (Hengge et al. 2023). Furthermore, some studies also find evidence of a carbon risk premium (including Bolton and Kacperczyk 2019, Alessi et al. 2021, Hsu et al. 2022, Pastor et al. 2022). Results are not robust however, as studies focusing on diversified long-short portfolios generally find no evidence of markets structurally pricing climate policy risk (including Choi et al. 2018, In et al. 2017, Rohleder et al. 2022, Gimeno and Gonzalez 2022).

In a recent paper (Loyson et al. 2023), we assess whether the mixed empirical results so far point to insufficient pricing of climate policy risk in financial markets, or whether they can be traced back to specific methodological choices. We account for inconsistencies in existing carbon data and employ several econometric models to assess the carbon risk premium both at an individual firm level as well as at a portfolio level. Finally, we also compare the period pre- and post-2015 Paris Agreement, to determine whether the agreement has impacted asset returns to reflect heightened policy risk. We find that financial sector agents fail to structurally reflect climate policy risks in stock valuations. Equity investors do not require extra compensation for their exposure to European companies with emission-intensive activities.

Carbon data and its inconsistencies

Consider first how to assess a company’s exposure to climate policy risk. We look at carbon intensity, which expresses a firm’s total emissions relative to its revenues. This relative metric provides information on a company’s carbon dependency when generating revenues and allows for comparing firms from various industries and sizes. Data on corporate emissions, however, suffers from three main issues that we account for in our analysis.

First, carbon data is inconsistent across providers, especially when a large number of values is estimated. A distinction is often made between emissions from owned or controlled sources (scope 1), indirect emissions associated with the purchase of electricity, steam, heat, or cooling (scope 2), and from upstream and downstream activities along the value chain (scope 3). Since scope 1 and 2 emissions are often reported by companies, this data are relatively comparable. Scope 3 data, however, is mostly estimated, and noisy across data providers (Klaassen 2021). We only look at scope 1 and 2 emissions. These data are relatively consistent between providers, especially for reported (as opposed to estimated) values. We use data from Trucost as they provide long timeseries and have high coverage of reported data.

Second, carbon data for corporates is generally published with a lag of approximately six months. As a result, information on a firm’s emissions is fed into market prices with a lag of six months to one year, depending on the exact time of publication. To avoid relating current year returns to emissions data that at the time of estimation was not published yet, we include a lagged variable of carbon intensity in our econometric models, similar to Bauer et al. (2023), Ardia et al. (2022), and Ilhan et al. (2021).

Third, inflation and exchange rate effects influence relative carbon metrics, especially when assessing developments over time. When price levels rise, uncorrected measures of carbon intensity increasingly overestimate real activity and thus increasingly underestimate ‘real’ carbon intensity (see Janssen et al. 2021). In our paper we use carbon intensity, which is generally reported in tCO2/$M, while we focus only on European companies. As a result, we have to correct our carbon intensity metric not only by deflating the values to 2005 equivalents (starting point of the data set), but also by converting the deflated values to their corresponding currency.

Short-run relationship between carbon emissions and stock returns

After having accounted for carbon data issues, we try to capture evidence of a carbon risk premium. Specifically, we analyse the effect of carbon intensity on excess stock returns of 1,555 European companies in ten different sectors between 2005 and 2019.

We first perform a straightforward Fama-French (FF) style panel regression, whereby we add carbon intensity as an additional variable to the three well-known Fama-French factors (market, size, and value) explaining excess returns of individual firms. We find that the level of carbon intensity does not have a significant impact on a firm’s excess return. This suggests that investors, at least between 2005 and 2019, did not yet require additional compensation for their exposure to emission-intensive companies.

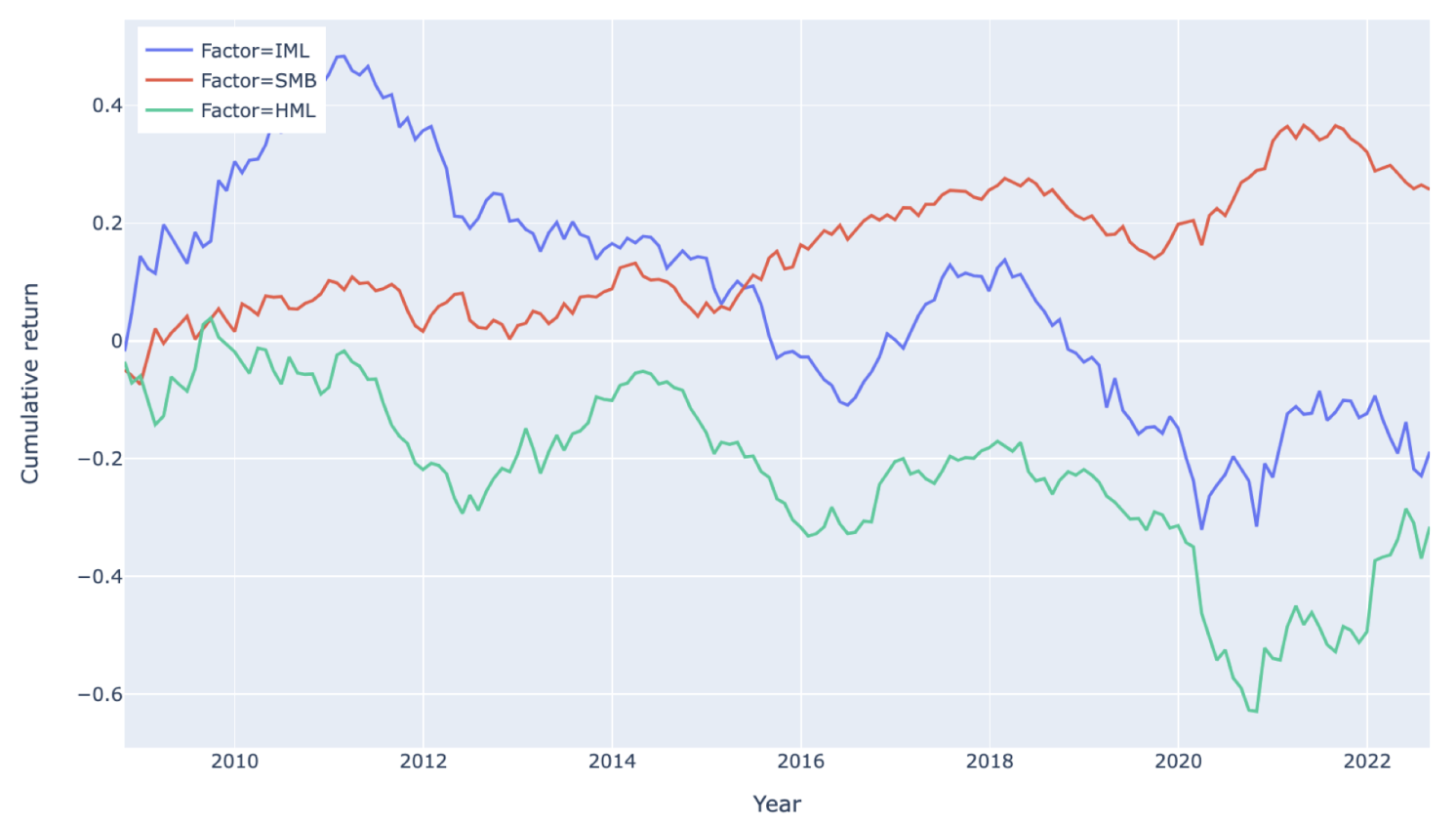

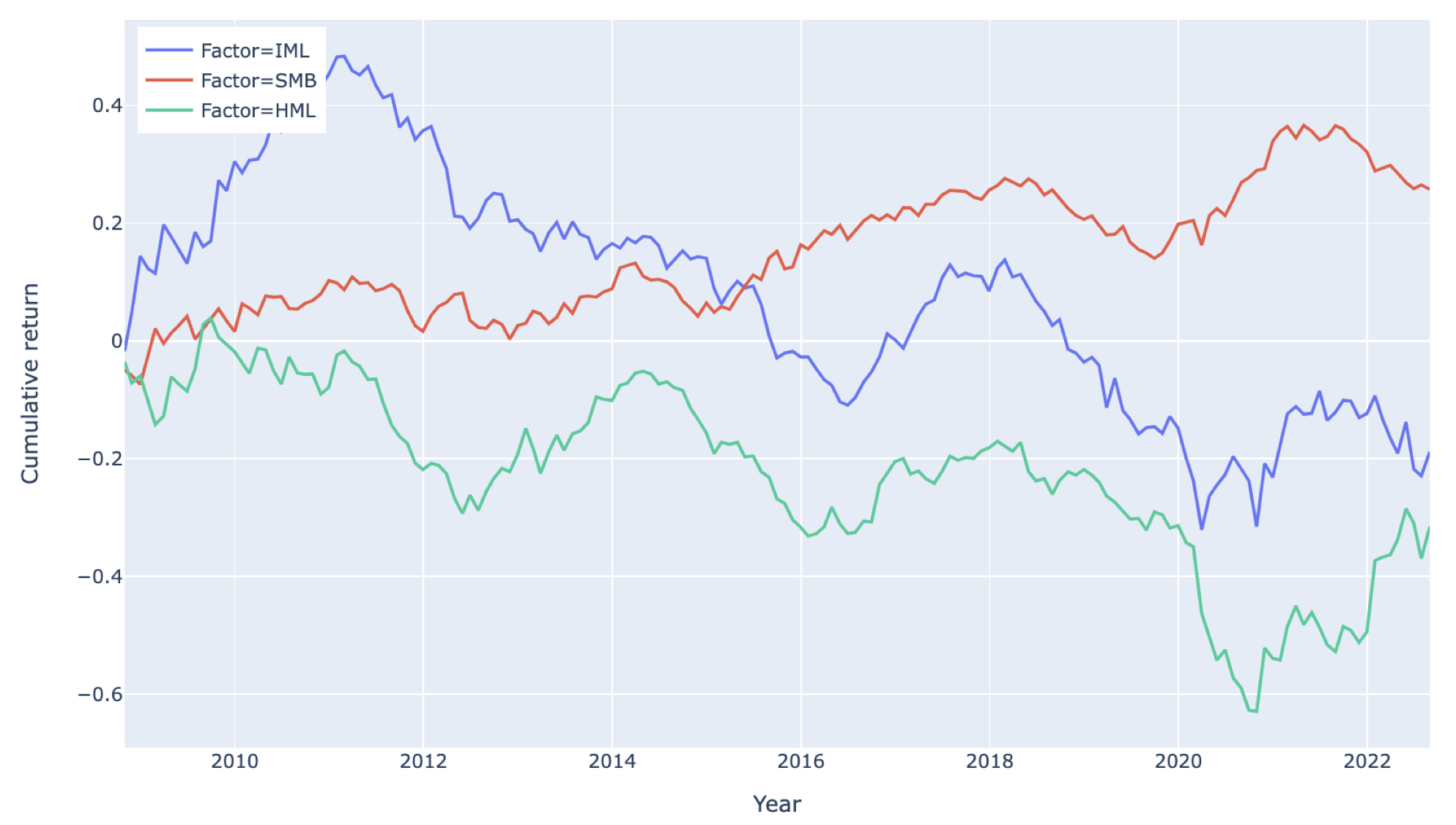

We then construct a carbon factor to assess whether there is a systemic return from investing in a portfolio with low climate policy risk exposure. By ranking companies on their sector, size, value, and carbon intensity, we develop a highly diversified carbon risk-mimicking portfolio. The ‘Intense-Minus-Less intense’ (IML) portfolio is an equally-weighted portfolio that is long in emission-intensive companies and short in emission-light companies. As carbon data are reported annually and the ranking of the companies by carbon intensity does not change much over the time horizon, there is no need for constant re-calibrating of the portfolios. Figure 1 plots the cumulative returns of the IML factor, as well as the cumulative returns on the other well-known Fama French factors SMB (Small-Minus-Big) and HML (High-Minus-Low). From 2019 onwards, it appears that companies with high carbon intensity performed worse than companies with low carbon intensity.

Figure 1 Intense-minus-less intense (IML) performance compared to small-minus-big (SMB) and high-minus-low (HML)

The Fama-Macbeth two-step procedure is used to assess whether carbon risk is priced in (Fama and MacBeth 1973). The first step of this procedure assesses whether the traditional Fama-French factors (market, size, value) plus our just developed carbon factor significantly affect a company’s excess return in each time period and in this way estimate a firm’s factor exposure. In the second step we directly assess whether the factor exposures obtained as the coefficients of the regression in the first step are significantly priced in. Notably, we find that the carbon factor is not significant: it apparently does not contribute significantly to an explanation of the cross-section variation in excess returns. This suggests that investors do not structurally require additional compensation for their exposure to climate policy risk. The question subsequently arises whether the Paris Agreement, which firmed up emission targets and thereby made carbon policy risk possibly more of an issue for investors, brought any change in that respect.

The effect of the Paris Agreement on the pricing of climate transition risk

The Paris Climate Agreement was adopted by 196 parties in 2015 and is the first binding agreement bringing nations together to combat climate change. The commitment heightened the possibility of governments setting more ambitious climate policies, presumably feeding into higher climate policy risk and, one would expect, a corresponding shift in carbon risk premia. To assess the effect of the Paris Agreement on European company’s excess returns, we compare the period pre and post 2015 by means of two treatment models.

First, we use the difference-in-differences (DID) approach pioneered by Wooldridge (2010), and perform this procedure for three different classifications of the treatment and control groups. For all three classifications, we find that the Paris Agreement had a positive but insignificant effect on stock returns. The positive estimate for the difference-in-differences coefficient suggests that the Paris Agreement had a positive effect on the yearly excess returns for emission-intensive companies, pointing to a gradual pricing in of climate policy risk. But the evidence is not significant.

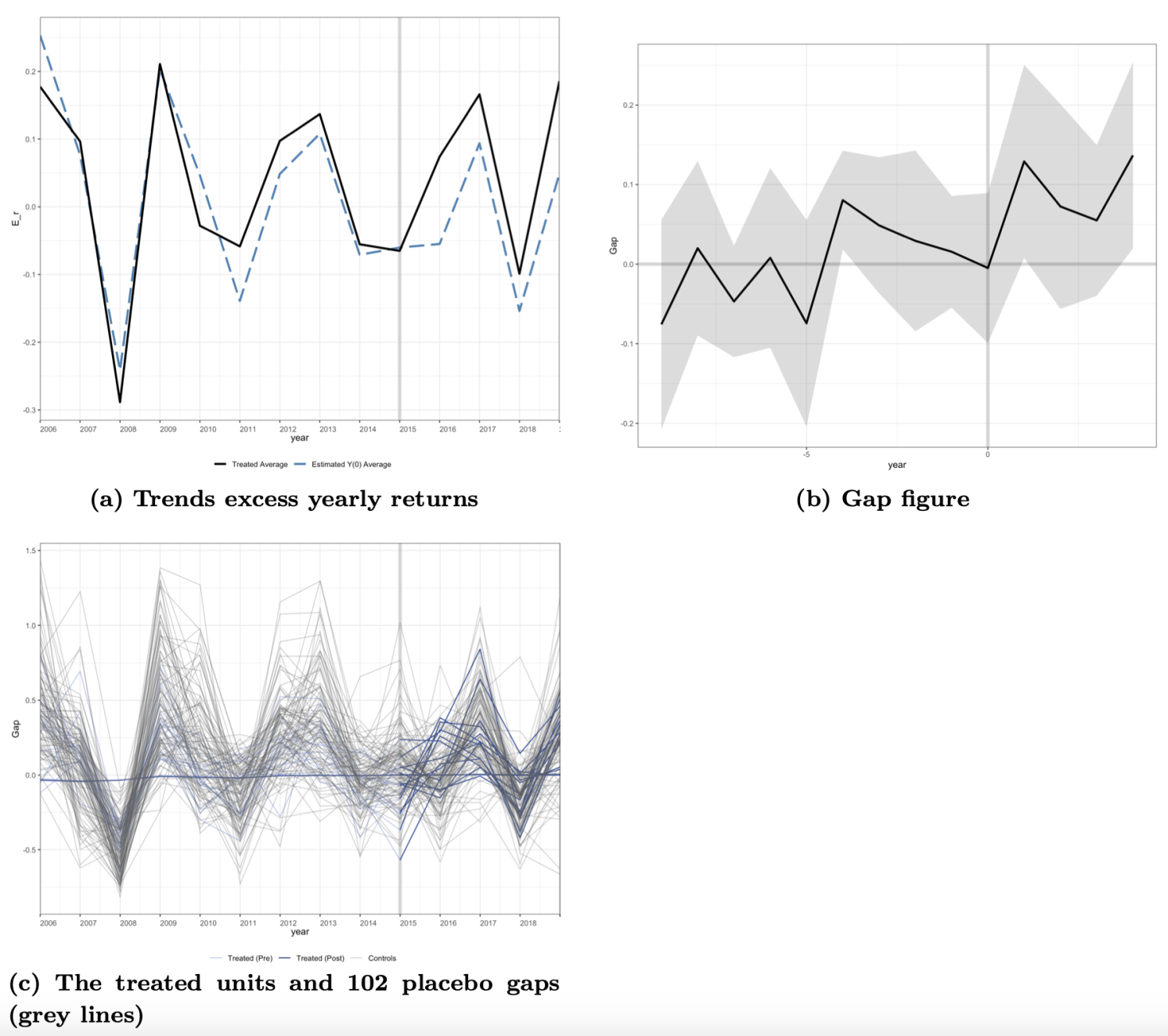

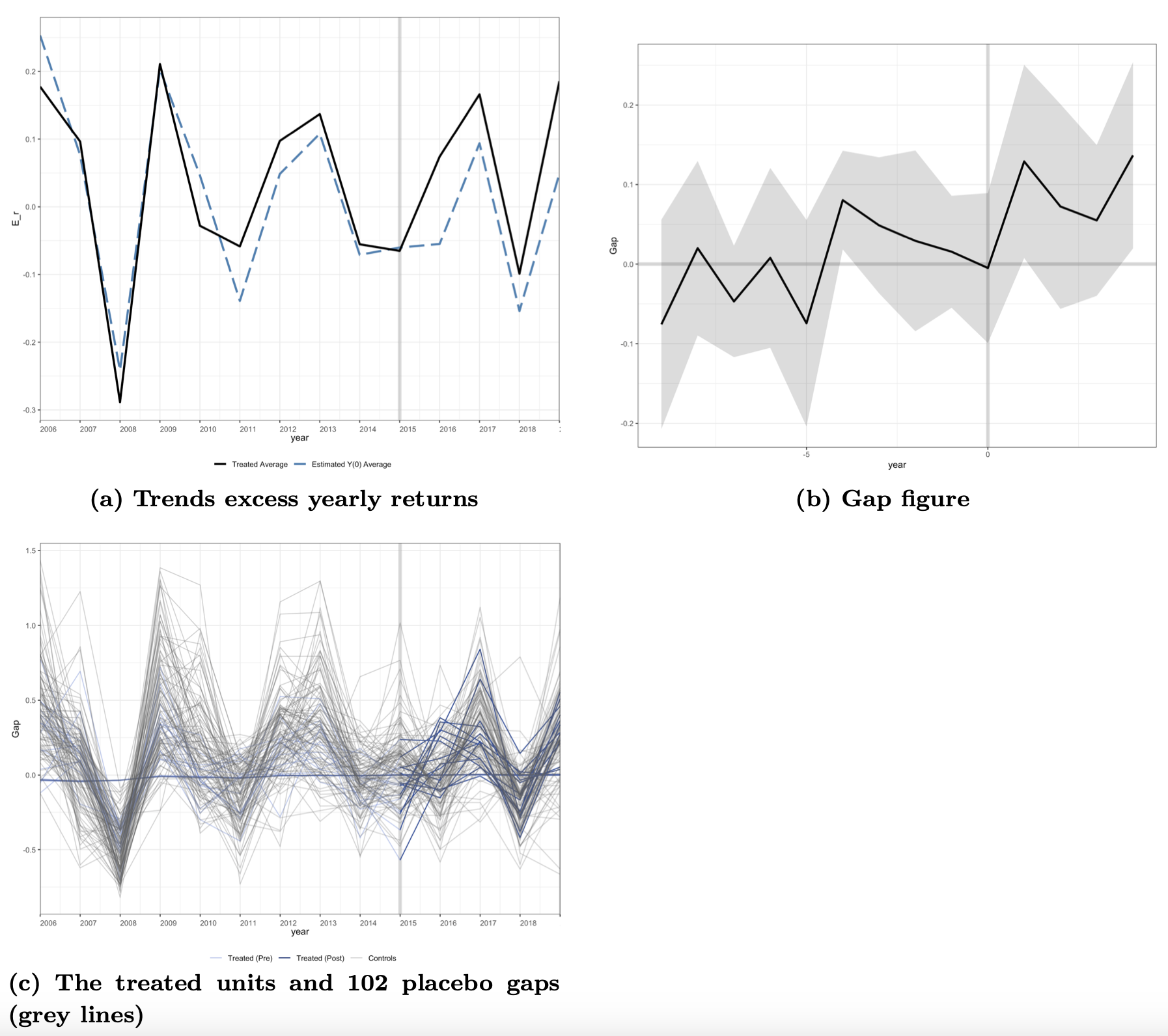

Second, we use the synthetic control method (SCM) by Abadie and Gardeazabal (2003) and Abadie et al. (2010) because the SCM objectively sets the control group. Moreover, the synthetic control method allows for the unobserved differences to vary over time, unlike the difference-in-differences method which requires that unobserved differences remain constant over time. We extend the original synthetic control method proposed by Abadie et al. (2010) to incorporate multiple treated units.

Figure 2a shows that the synthetic control group yields lower returns after 2015, implying that emission-intensive companies would have had lower returns in absence of the Paris Agreement. Figure 2b displays the gap between the predicted outcomes of the synthetic control group and the treated units. The gap after 2015 indicates the average effect on the treated companies (ATT): 0.098. This suggests that the Paris Agreement had a positive effect on the excess returns of the treated companies, pointing to the emergence of a carbon risk premium. Figure 2c however suggests that the estimated treatment effects are not extreme compared to the 102 placebo companies. When looking at the placebo effects using multiple treated units, however, the Paris Agreement did not have significant effects on the returns of emission-intense companies. All in all, and despite insignificant results, the treatment effect models do provide some preliminary evidence that the Paris Agreement had a positive impact on stock returns of emissions-intensive companies, suggesting a gradual shift to market pricing of climate policy risk.

Figure 2 Synthetic control method graphical analysis

The absence of a clear priced-in carbon factor suggests the need for more ambitious climate policies, so that investors will start to allocate more capital to emissions-light firms. Inability to reflect climate policy risk in asset prices may threaten financial stability once carbon policy does materialise and is necessary for efficient capital reallocation away from polluting firms towards clean firms.

Source : VOXeu

.jpg")

")

")

.jpeg")

")

")

")

")

")

")