Countries’ monetary policies have addressed the current inflation crisis with a strict national focus. As global spillovers from these policies are significant and create the risk of turmoil in the international debt market, there could be a case for cross-border policy cooperation. This column draws on theory to gain insight into why we do not see cooperation during disinflation episodes. There are reasons why it may well be in the cards in the coming quarters.

The rapid pace at which central banks across the world have been increasing policy rates in response to rising inflation has raised concerns about the disruptive effects of cross-border spillovers. Everything else equal, a monetary contraction in a country tends to raise inflation and reduce activity abroad. When the contraction originates in a systemically important country like the US, it drives risk premia and deteriorates borrowing conditions in global markets. This magnifies the risk of turmoil in sovereign and external debt markets, especially, but not exclusively, in emerging market economies and less developed economies. The main concern is that if central banks fail to internalise cross-border spillovers, their actions may result in excessive contraction worldwide and create debt crises (Jimenez et al. 2023) – a risk that could be moderated, if not avoided altogether, by coordinating the anti-inflationary stance.

Yet, domestic monetary policies have been implemented with a strict national focus (van der Cruijsen et al. 2023). Admittedly, some of the most dreaded consequences of the monetary contraction – for example, a widespread debt crisis – have not materialised, at least not yet. The question is whether, looking forward, some form of coordination in stabilisation policy would be necessary to reduce major risks that still weigh on our immediate future (Corsetti et al. 2023).

Global spillovers in perspective

To put into perspective global spillovers in the disinflation process, it is essential to recognise that while inflation has risen almost everywhere – even in Japan, but with the notable exception of Switzerland – the underlying factors and the timing are by no means uniform.

At the root of early price hikes, especially in the US, was the sharp rise in demand for (durable) goods in the aftermath of COVID-19 at a time in which global value chain problems were disrupting supply. Goods, relative to services, are to a large extent internationally tradable and their production is more intensive in energy and commodities. As a result, the early inflationary impulse is transmitted globally. Over time, price pressures started to spill over to other sectors (mostly services), driving up core inflation – fed by fiscal expansion and a relatively accommodating monetary policy, as well as by the imbalances in the labour market.

When energy prices shot up after the Russian invasion of Ukraine, the impact was profoundly asymmetric. The energy crisis imparted a strong stagflationary impulse in Europe (partially offset by countercyclical fiscal policies) and other regions in the world but affected the US much less. Throughout 2022, Europe faced strong terms-of-trade deterioration, which affected incomes and its productive sector competitiveness. Meanwhile, the US could keep implementing its deflationary policy in a much more favourable cyclical environment.

Monetary policy fights inflation by raising rates, by keeping ‘financial conditions’ sufficiently tight, and via an appreciation of currency, all of which tend to reduce imported inflation. In recent months, these three components, interrelated and endogenous to each other, have been carefully managed via communication and forward guidance – in the case of currency, sometimes reiterating ‘benign neglect’.

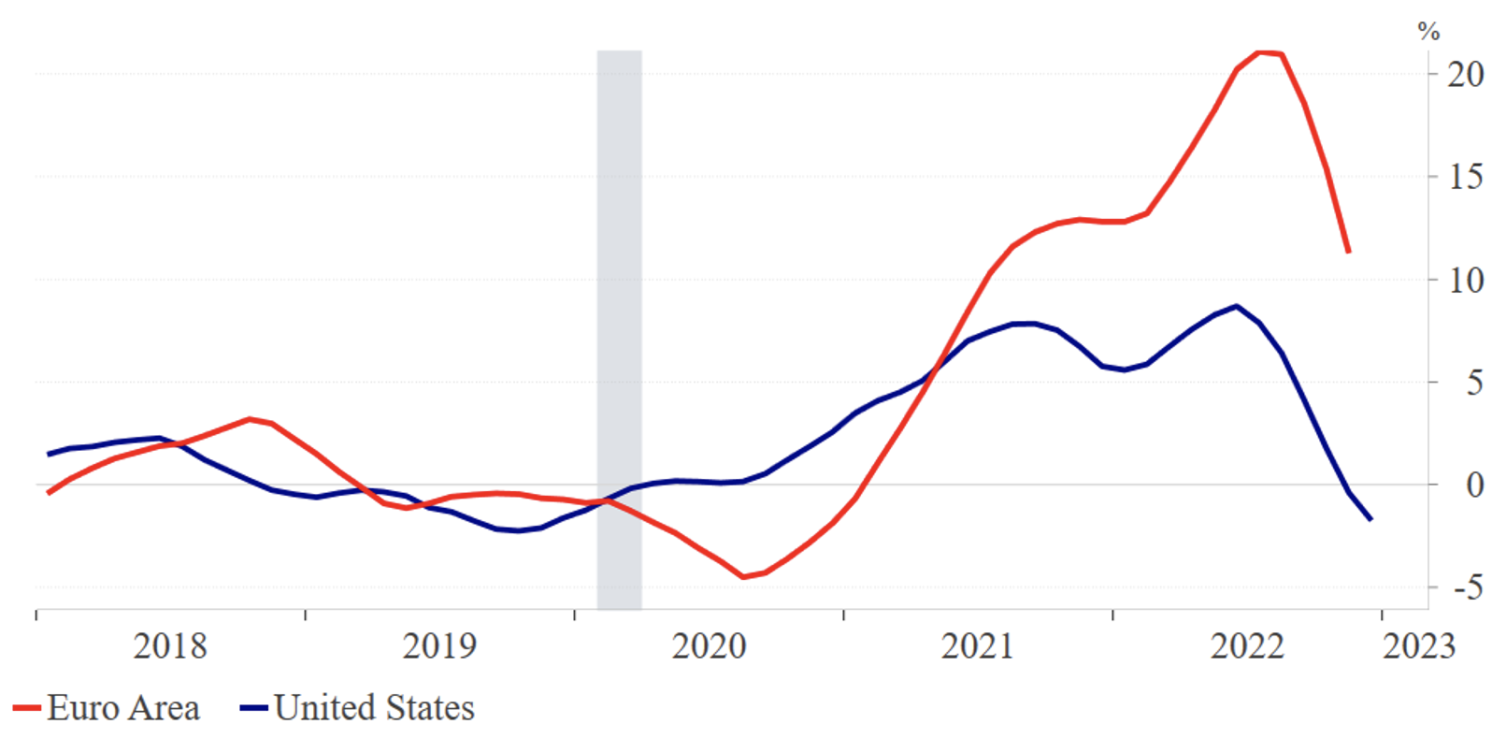

At the start of 2023, the anti-inflationary stance of the Federal Reserve Board seems to be working well in the US. Imported inflation fell rapidly from its peak in March 2022, partly because of improvements in global production networks in the post-COVID-19 reopening of the economy, which made supply bottlenecks less likely – but also because of the strong dollar. Figure 1 compares the fall in imported (manufacturing) inflation in the US and Europe since the beginning of 2023. The relative contribution of the exchange rate in the two areas is apparent.

Figure 1 Import prices inflation excluding petroleum products (6-month-over-6-month at annual rate)

Notes: The figure shows the inflation rate in imported manufactured goods, 6-month-over-6-month at annual rate. The levels of the series are expressed in US dollars and euros, respectively. The 6m/6m changes are calculated following the BEA national accounts procedure. The source of the raw data is BLS for the US and Eurostat for the Euro area. The shadowed areas indicate NBER recessions.

US core inflation measures net of rents have risen at a pace close to target in the final months of 2022. Most strikingly, real economic activity is holding up quite well despite the disinflationary environment. The US Fed has been quite vocal in its warnings that relaxing financial conditions is still premature. However, while there could be negative surprises in the coming months, the US monetary stance is working in the eyes of market participants: market-based expectations remain anchored and long-term rates appear to have peaked. Other regions in the world, especially Europe, are not as far along in the disinflation process.

Coordination is no panacea

There is no strong intellectual support for international policy cooperation in economics in general. Looking back to the 1970s, this was arguably the period in which academic work was most sympathetic, on the ground that jointly managing the macroeconomic effects of large global shocks (to oil prices) would have helped reduce their impact on economic activity. Even so, a number of critical views rapidly came to dominate the debate.

One view took issue with the fact that negotiating a coordinated response typically takes too long for this response to be timely. A second view stressed that each government would be tempted to free ride the (costly) measures undertaken by the others. Provided all countries agree on undertaking, say, a costly fiscal expansion to support global demand, a country could gain by delivering less than negotiated and still benefitting from the global demand generated by the others.

A third criticism is more relevant today. To the extent that cooperation effectively internalises cross-border demand spillovers, it reduces the credibility of the monetary authorities’ anti-inflationary stance vis-à-vis their domestic firms, unions, and investors. This classical argument, formalised by Rogoff (1985), provides a key insight into why it is hard to find historical examples of cooperation during disinflation. Especially in these circumstances, coordination ends up being counterproductive in that it frustrates disinflation efforts. Central banks may well steer away from it consciously.

Additional insight comes from a fourth and more recent criticism, rooted in modern dynamic macro models predicting that, from a welfare perspective, the gains from cross-border cooperation tend to be negligible. While this may not hold in general (as demonstrated in Bodenstein et al. 2020), it has lent significant theoretical support to the idea that ‘keeping one’s house in order’ is the best way to ensure global macroeconomic stability.

The idea is especially compelling today: the major risk facing central banks is that of losing control over inflation expectations and entering a destabilising regime of high and variable price dynamics. The experience of the 1980s is brought to bear on this risk. Once inflation dynamics feed on themselves, stabilisation is very costly in terms of employment. Today, in the US at least, the cyclical cost is not as large as back in the 1980s. Restoring price stability smoothly but quickly is the key priority.

A dollar case for coordination

History and practical considerations nonetheless invite caution in dismissing the case for cooperation. In the mid-1980s, in the aftermath of the US clampdown on inflation, governments did need to act together and correct the over-appreciation of the dollar – at the time also reflecting a mix of tight monetary and loose fiscal policy in the US. A strong dollar systematically worsens borrowing and financial conditions throughout the world, with inflationary and contractionary consequences in emerging market economies and less developed economies, on top of and above the effects of rate hikes in the US. There is indeed some evidence of a specific ‘dollar cycle’, which reflects not only monetary policy but also fluctuations in the risk appetite of investors and/or flight-to-safety in response to uncertainty shocks.

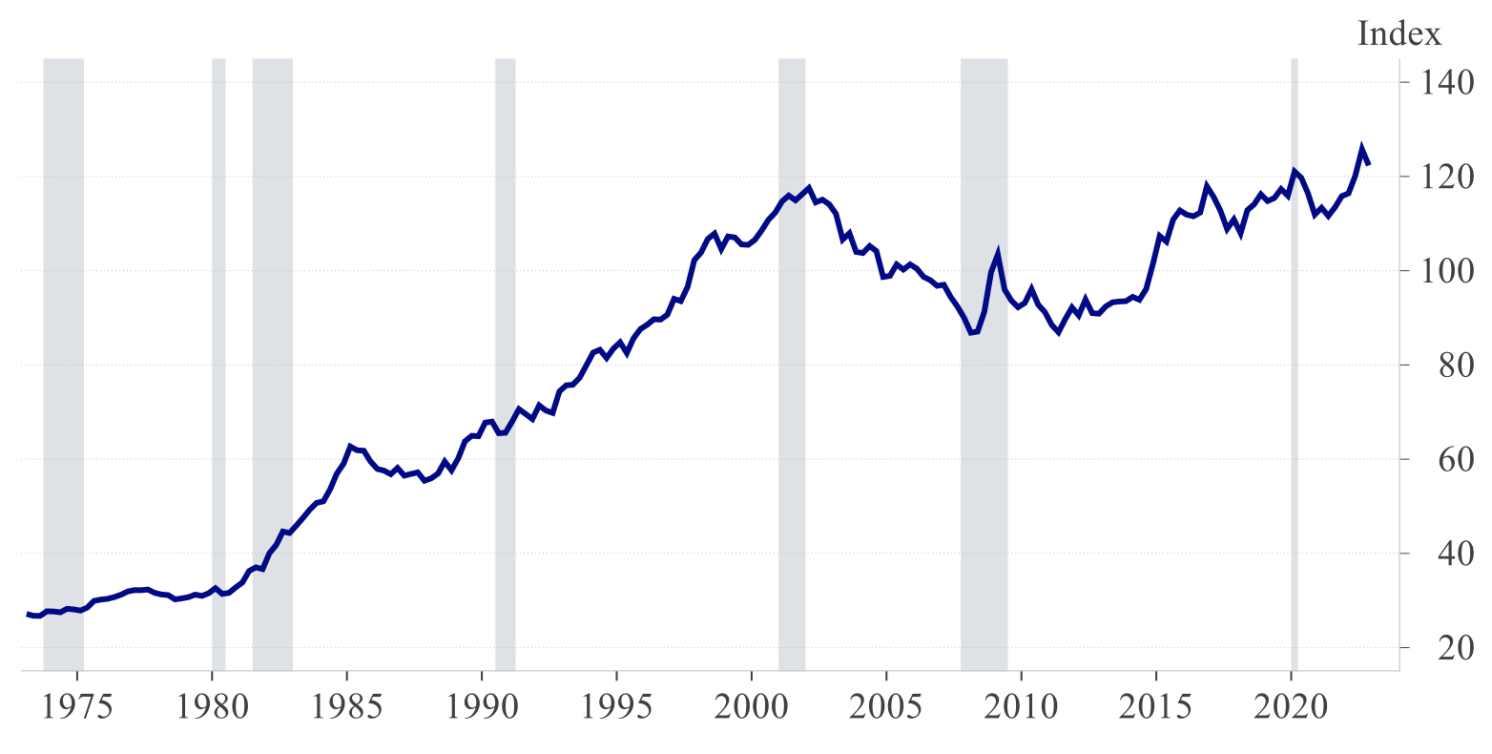

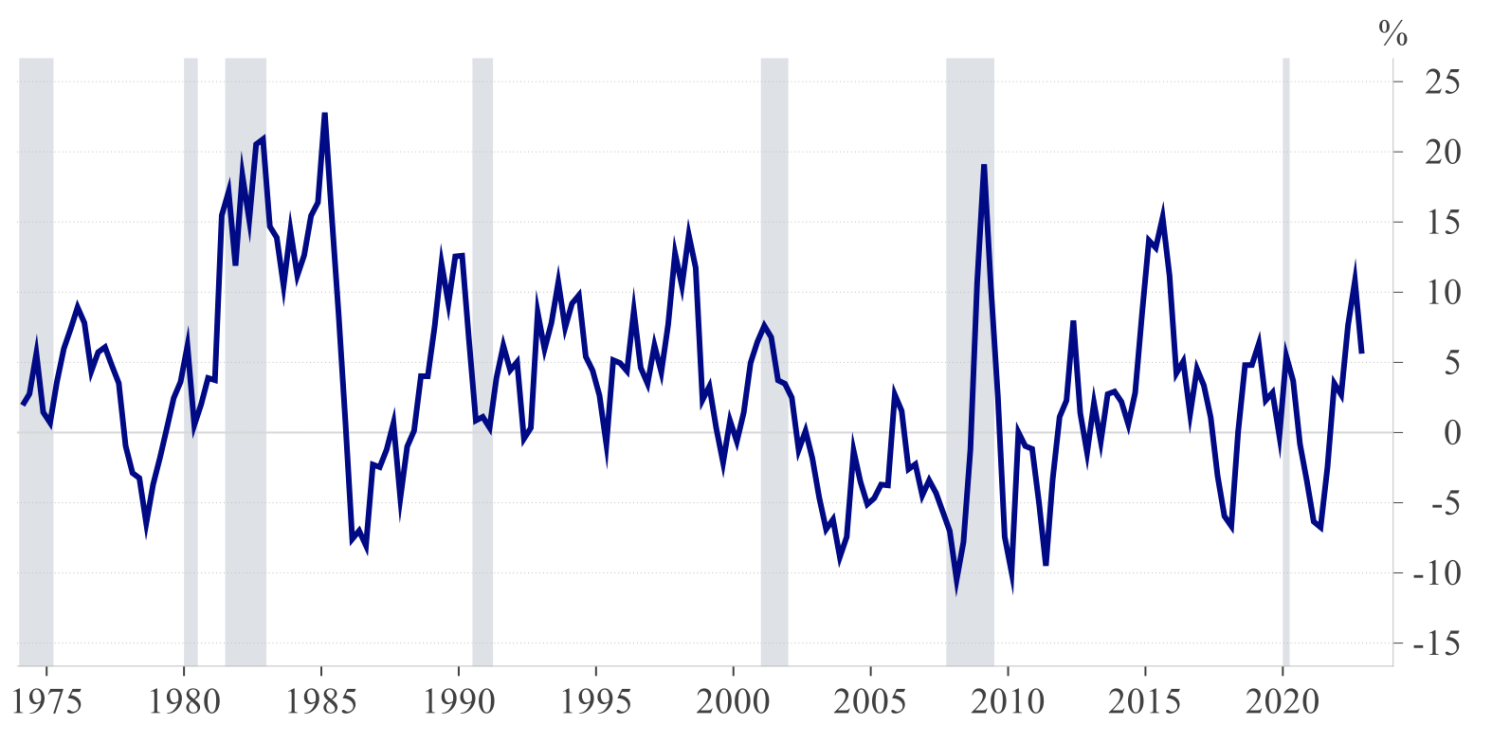

Looking at the coming quarters, a coordinated initiative on exchange-rate misalignment may well become desirable, especially if market forces fail to realign the dollar and as monetary policy in leading regions of the world gradually converge at the end of their contractionary cycle. As shown in Figure 2, in multilateral terms, the dollar reached an all-time high in October 2022. Since then, it has been gently but decisively falling, as positive news on inflation has been suggesting a revision in the pace of US rate hikes.

Figure 2 Nominal broad dollar index (level)

Note: The figure shows the level of the nominal broad dollar index. Source: Board of Governors of the Federal Reserve. The shadowed areas indicate NBER recessions.

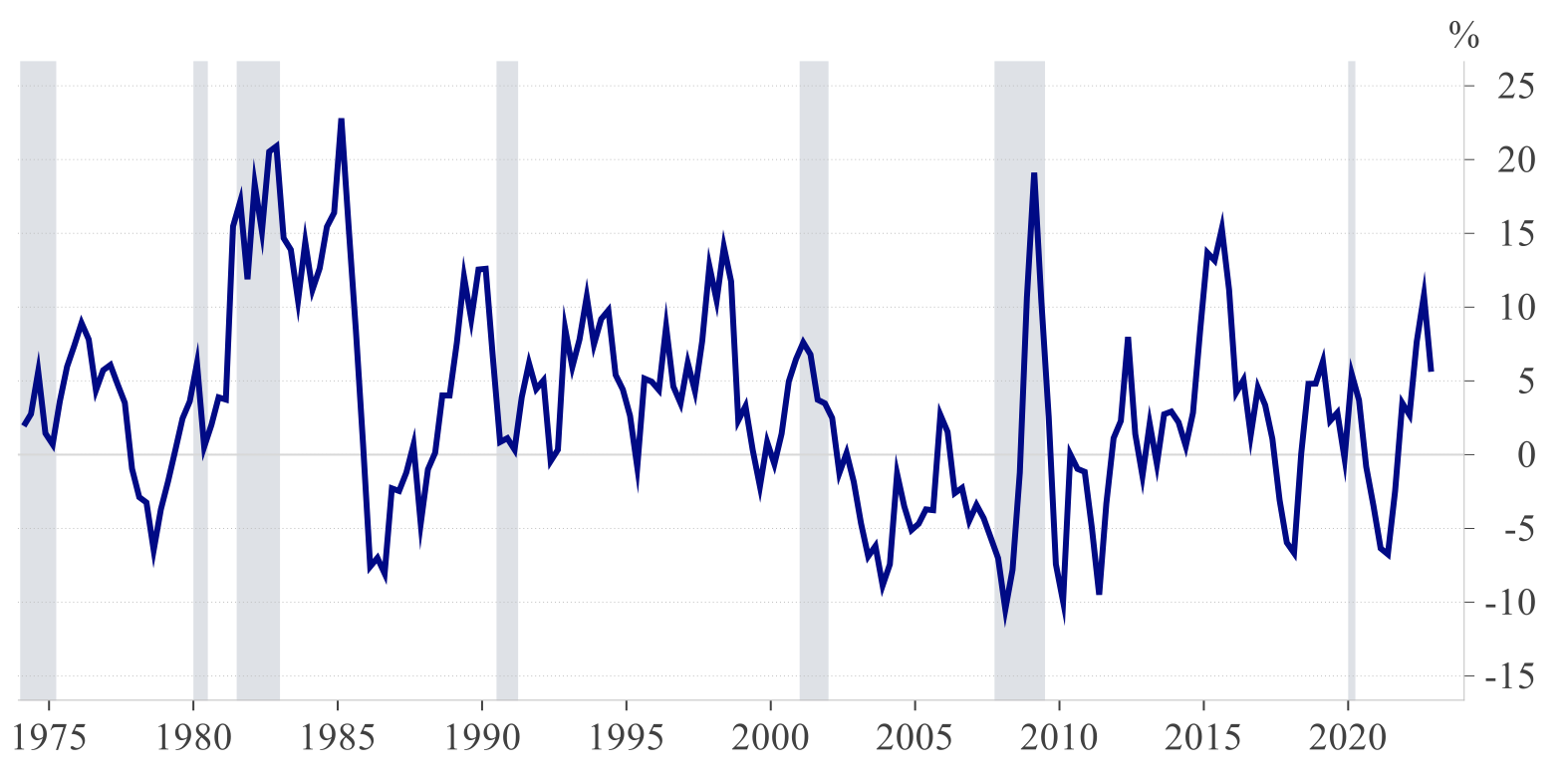

One may observe that, while the value of the dollar is high in level, its appreciation during the inflation crisis has been somewhat smaller than in other crisis periods, for example during the debt crisis in the 1980s (see Figure 3). As shown by this graph, in 2022 the dollar’s annual appreciation peaked at 11%, against 22% in 1982 and almost 23% in 1985. This observation may explain why the economic and financial effects of dollar appreciation have remained relatively contained between 2021 and 2022. That said, the outlook remains highly uncertain in the coming quarters.

Figure 3 Nominal broad dollar index (year-over-year change)

Note: The figure shows the year-over-year nominal broad dollar index. Source: Board of Governors of the Federal Reserve. The shadowed areas indicate NBER recessions.

Relative to the 1980s, the level of cross-border and cross-currency financial interconnectedness of markets and intermediaries is much higher, as is the leverage of intermediaries and private and public debt. Even relatively mild shocks could ignite a massive flight to safety and feed a dollar rally with disruptive effects on financial and real markets and potential geopolitical consequences. National monetary authorities may be called to deliver prompt, coordinated liquidity interventions, extend guarantees to private actors and official institutions, or even adjust conventional instruments.

The US has long enjoyed significant benefits from its unique position in the global economy as supplier of the safe asset. With its larger external debt, and vis-à-vis rising geopolitical challenges, the goal of preserving these benefits may motivate the US to promote and engage in cross-border cooperation to a significantly larger extent than in recent times.

Source : VOXEu

")

")

.jpeg")

")

")

")

")

")

")