Residential prices in the US increased in the suburbs during the pandemic relative to neighbourhoods closer to city centres, reflecting a relocation of residents away from downtowns. At the same time, demand for offices fell. This column argues that these changes can be traced back to the rise of work-from-home arrangements, which have created a ‘commuting dividend’ and a ‘home-office tax’. Changes in urban amenities amplify the effects. While more attractive downtowns are likely to enjoy a renaissance, hosting more creative workers who go into work to benefit from exchanging with others, other downtowns may not recover.

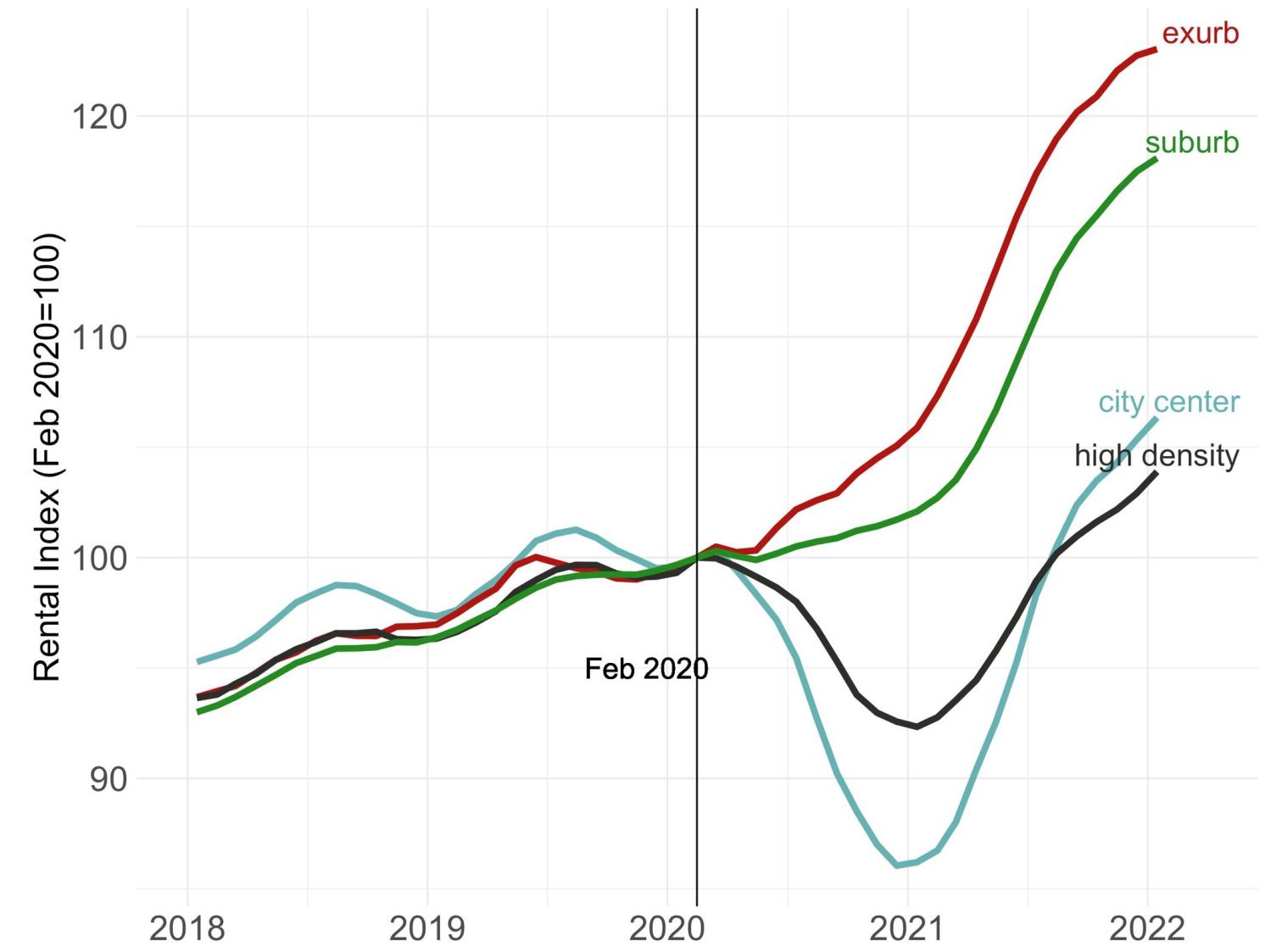

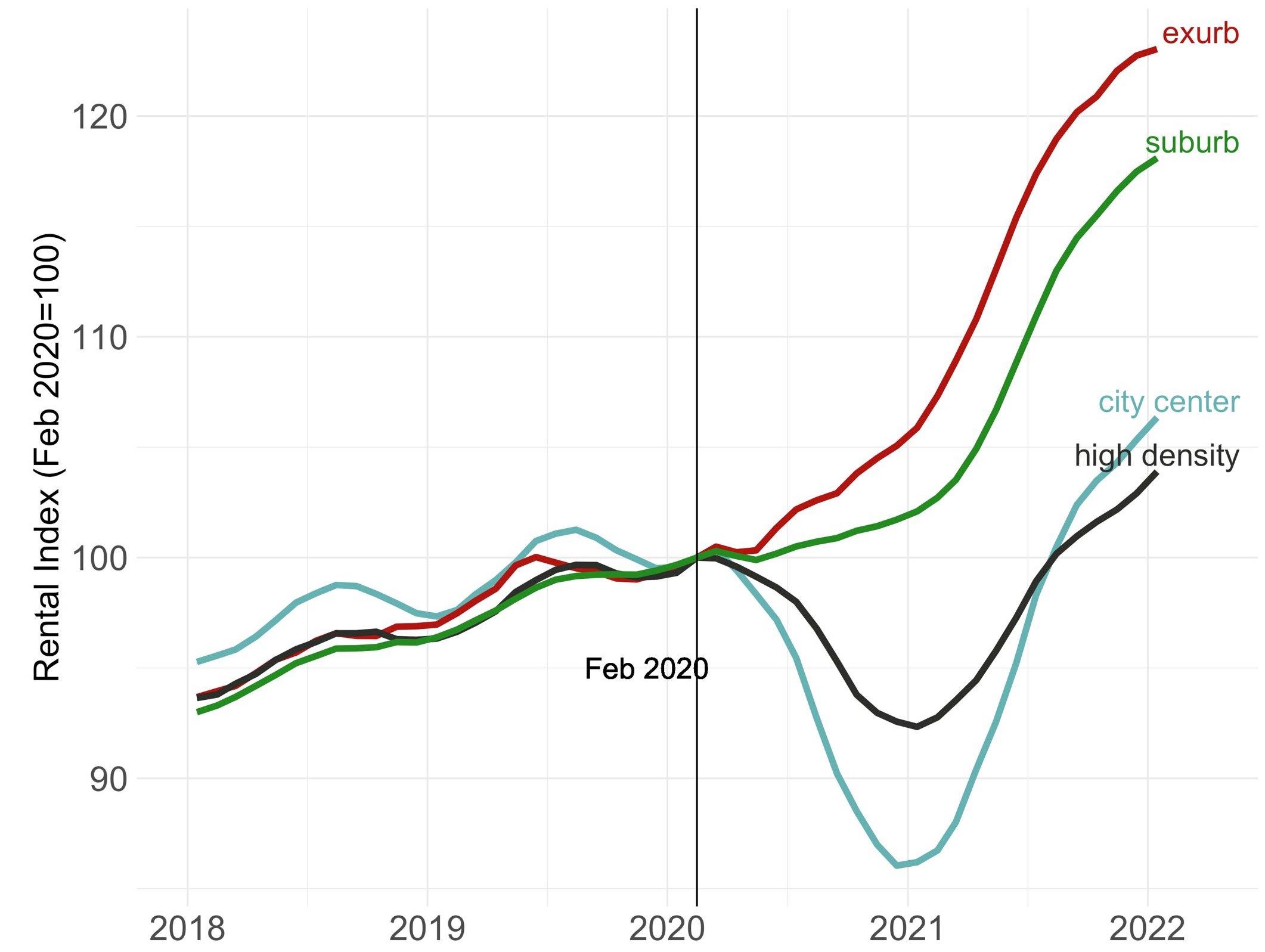

Residential prices in US cities rose on average by about 24% between November 2019, just before the COVID-19 pandemic, and November 2021 (Mondragon and Wieland 2022). Beneath this aggregate shift were important differences in price changes within cities: residential prices increased in the suburbs relative to neighbourhoods closer to city centres, where prices even declined in some cases. Figure 1, borrowed from Ramani and Bloom (2021a), illustrates this flattening of the property price gradient.

Figure 1 Rents in twelve US cities

Note: Zillow data from NY, LE, SF, Chicago, Dallas, Houston, Miami, Philadelphia, Washington, Atlanta, Boston and Phoenix by zip-code population density.

Source: Ramani and Bloom (2021a).

The sharp divergence in prices between centres and suburbs reflects a significant relocation of residents away from downtowns. The US Postal Service National Change of Address database shows households moving from downtown toward the suburbs in large US cities at the onset of the pandemic. Between February 2020 and January 2021, the densest zip codes lost about 15% of their populations, while the least dense gained about 2% (Ramani and Bloom 2021a, 2021b, Thwaites et al. 2021). These large changes are often referred to as a ‘donut effect’, alluding to renewed suburbanisation and a partial hollowing out of cities of their downtown residents.

The commercial real estate markets also saw large shifts. Revenue declined by on average 8% in the office sector in the US between early 2020 and late 2021 (Gupta et al. 2022). These shifts were at first driven by quantity adjustments: vacancy rates boomed in many US cities, reaching more than 30% in San Francisco this summer. Commercial rents are extremely sticky because they are set in long-term leases with pre-agreed escalator clauses. In weak markets, landlords are reluctant to commit to lower rents for new tenants and prefer to wait, leading to vacancies. As a result, commercial rents for offices and retail have started to adjust and they show a similar pattern to housing with a stronger decline downtown and in the largest US cities (Rosenthal et al. 2022).

Behind this lower demand for offices is the rise of working from home, either through hybrid arrangements or fully remote jobs. Working from home rose fivefold from 2019 to 2023, with 40% of US employees now working remotely at least one day a week (Barrero et al. 2023). Gupta et al. (2022) report an occupancy rate of only about 50% for the ten largest office markets in the United States as of May 2022. With every indication that remote work is here to stay, adjustments in the US retail and office markets are far from over, and many are predicting a forthcoming office apocalypse (Gupta et al. 2022)

Despite the much-publicised exodus out of New York and San Francisco early during the pandemic, so far we have only observed small and often temporary outflows from the largest cities. A key reason behind these small flows is the high cost of cross-city moves, exacerbated by inelastic housing supply, since households need an empty house or apartment to move into. As the housing supply begins to adjust, there are hints of more persistent population changes. For example, between a quarter and one-third of moves are beyond commutable distance (i.e. four or more hours from the workplace) (Ozimek 2022). Higher interest rates, however, have made a large dent in new housing construction, which was already weak prior to the pandemic. Although further population adjustment across cities is expected, it will likely take place over many years to come.

In a recent paper (Duranton and Handbury 2023), we show that these changes can all be traced back to the rise of work-from-home arrangements. Working from home changes the household location decision in two ways: the first is a reduction in commuting costs; the second is a reduction in, or tax on, the space one can consume at home to make room for an office. We refer to these as a ‘commuting dividend’ and a ‘home-office tax’. Taken together, these two forces imply an increase in the aggregate demand for housing, since households want to replace the space taken by their new home office, and they find more remote locations relatively more attractive. As long as work from home remains, these forces will remain at play.

The COVID-era shifts we observe in the rents and price gradients are, to a large extent, textbook illustrations of what the simplest urban models would predict following the twin work-from-home shocks of the commuting dividend and the home-office tax. They also reflect what more recent models would predict from a reduction in the amenity value of downtowns, where the demise of the ‘lunch economy’ sustained by office workers has broad-ranging implications for the viability of many downtown amenities. The textbook model in the tradition of Alonso (1964), Mills (1967), and Muth (1969) is useful for interpreting the current situation and further provides a framework with which to form ideas about how future changes may look.

A simple urban model where residential choices depend only on housing and commuting costs matches, qualitatively and quantitatively, the short-run response to the twin COVID shocks that we observe. When most of the workforce is working from home, prices increase in the suburbs and decline near city centres. With adjustments, the model can allow for the scenario where only some workers, typically college educated, continue to work from home but everyone else resumes commuting full-time. This specification matches the medium-run price response in the data: prices increase citywide because the skew in the commuting dividend towards the higher-paid college graduates generates a larger increase in aggregate housing demand.

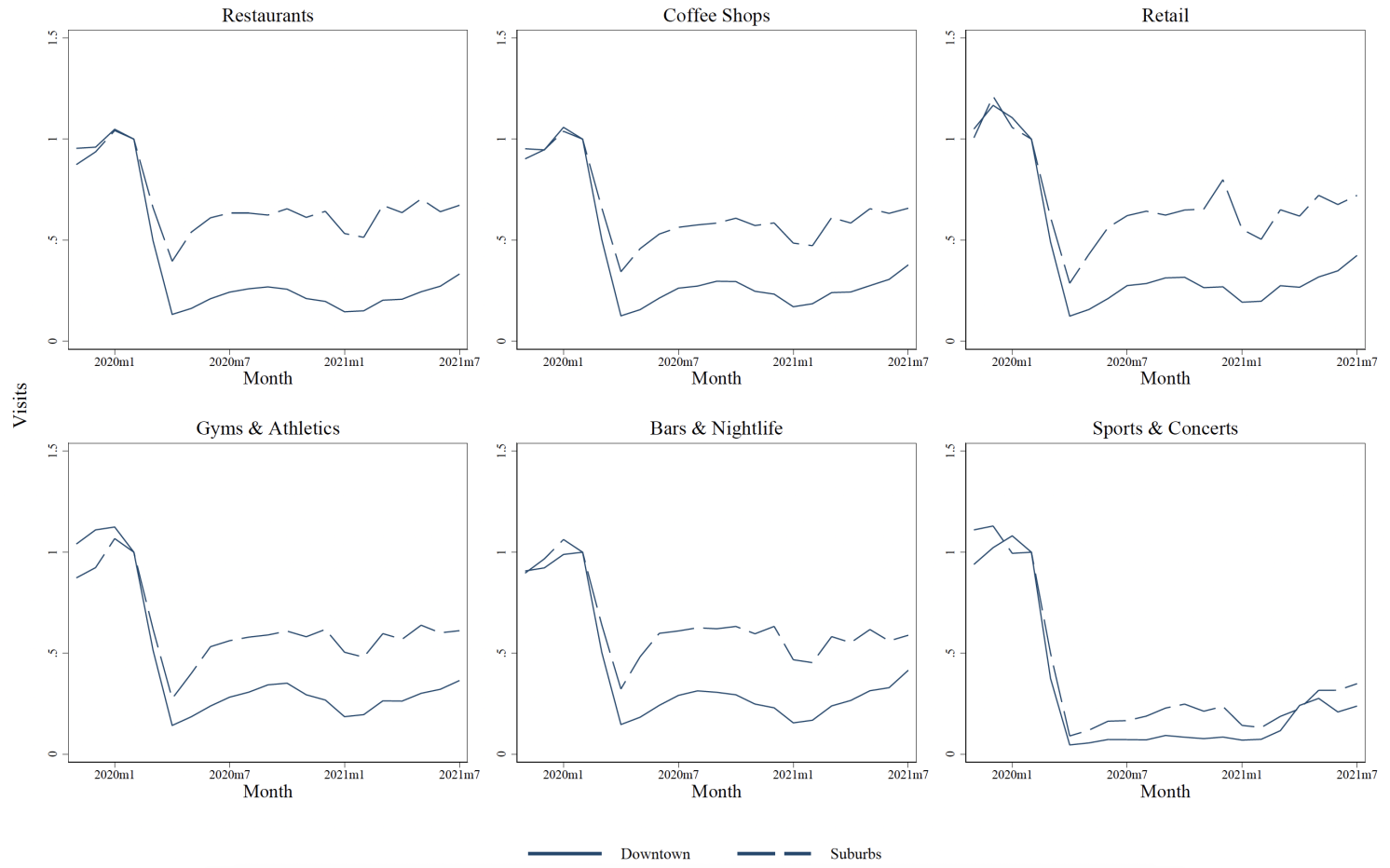

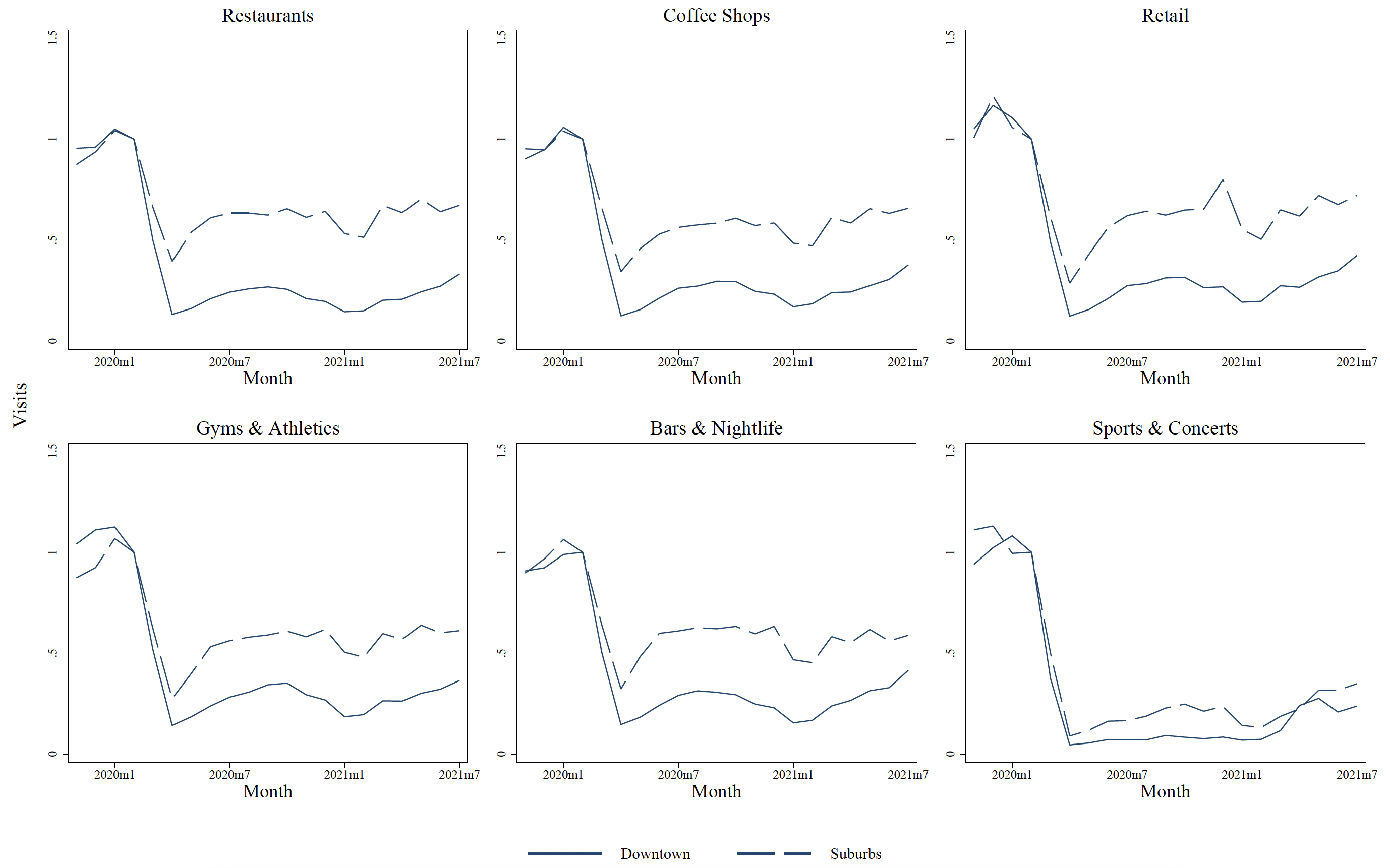

Changes in urban amenities amplify all of these effects. Household demand for restaurants, bars, gyms, salons, and other non-tradeable services has rebounded as the health risks of participating in these indoor activities subsided. However, these amenities may spread out more post-pandemic so that they locate closer to where their customers are, as illustrated by Figure 2 and discussed by Thisse et al. (2022). The advantage of urban centres in providing a wide variety of these establishments relies crucially on the daytime workforce. So, if downtowns cease to be great places to work, they may also stop being such great places to live.

Figure 2 Establishment visits: Downtown versus suburbs

Notes: PlaceIQ data for New York, Los Angeles, Chicago, San Francisco, Dallas, Houston, Miami, Philadelphia, Washington, Atlanta, Boston, and Phoenix by distance to the center (PlaceIQ, 2023). Downtown establishments are those within 2 kilometers of the center; suburban establishments are those further out but within the same Core-Based Statistical Area (CBSA).

In our paper, we also consider the effect that work from home has on the strength of agglomeration forces in cities. To a large extent, the agglomeration economies associated with the physical proximity of workers who learn from each other behave like local amenities. At the same time, these direct interactions are only one channel for agglomeration effects. Other channels, such as those that rely on the thickness of local labour markets or a dense network of input-output transactions, are less susceptible to change from work from home.

Finally, we return to the same model and allow the long-run margins to operate. While obviously speculative, we expect that the twin shocks of the commuting dividend and the home-office tax will amplify the current trends in the longer run. More attractive downtowns are likely to enjoy a renaissance. We expect that the recovering downtowns will host more creative workers who go to work to benefit from exchanging with others. Due to their outward orientation and their spending power, these workers will energise downtowns and other concentrations of economic activity much more than the many workers who previously showed up at work just because everyone thought they should. These centres of economic activity may turn out to be even more vibrant than they were before COVID. Since there are only so many creative workers whose jobs depend on human interactions and these workers can cluster in certain cities, perhaps not all downtowns will recover.

Meanwhile, housing supply will adjust to accommodate the increasing demand for housing by support workers who work from home most of the time and may demand a home office. Cities will likely expand physically to allow for new residential construction. As the response of housing supply is likely to differ greatly across cities, ‘housing hungry’ residents will relocate to cities willing to accommodate urban expansion.

Source : VOXeu

")

")

.jpeg")

")

")

")

")

")

")