The experience of the UK with the Liz Truss government and its ‘mini budget’ brought to the fore the importance of well-functioning political institutions for the economy to prosper (Acemoğlu and Robinson 2012, Alesina and Perotti 1994), and showed that the effect of political degradation on the economy can materialise quickly. The recent credit crunch in South Korea provides an unfortunate but compelling natural experiment in support of this view. We document how a seemingly minor default of an amusement park developer induced by a political misjudgement transformed into a serious credit crunch and caused severe dislocations of broader financial markets. The evidence suggests that the default was not related to the prevailing economic conditions, hence the causality ran from the default to the observed outcomes that followed. We discuss the episode and Korean policy responses to the credit crunch, and the policy challenges ahead that the event highlights.

Background

South Korea’s economic recovery from the covid pandemic was interrupted by the Russian invasion of Ukraine, with GDP growth slowing but remaining positive, while the inflation rate surged to 5.6% in September 2022, significantly above the 2% target. The Bank of Korea (BOK) increased its policy rate from 0.75% in August 2021 to 2.5% a year later to contain inflationary developments. While the Bank of Korea’s economic outlook report for August 2022 (Bank of Korea 2022a) expressed concerns about weaker economic growth and inflationary pressure, its financial market trends report for August 2022 (Bank of Korea 2022b) did not indicate notable developments in credit markets (even though it took note of worsening corporate bond issuance conditions). The situation certainly did not warrant exigent government interventions.

Default

On 28 September 2022, Gangwon province’s newly elected conservative governor, Kim Jin-tae, unexpectedly declared that he would not honour the local government’s guarantee on the A1-rated (the highest rating) asset-backed commercial paper (ABCP) of Gangwon Jungdo Development Corp (GJC), the developer of the Legoland Korea amusement park located in the same province. There was no indication prior to the announcement or since then that the local government was under financial pressure: the missed payment was not due to budgetary reasons. It is understood that the new governor refused to make the payment due to political/ideological considerations as Legoland Korea was associated with the previous liberal governor (Nam 2022, Park 2022). Indeed, the 205 billion won (around $144 million) that was owed by GJC was a minor item for the local government and it was not being asked to pay back the entire amount (Park 2022). GJC missed the payment on 29 September and the default was declared on its asset-backed commercial paper on 5 October.

Gradually, then suddenly

The credit markets started pricing in the implication of the GJC default, an unthinkable event that signalled to market participants that even a government guarantee does not provide adequate protection after all. The incident led to a reassessment of credit risk in broader markets over subsequent days.

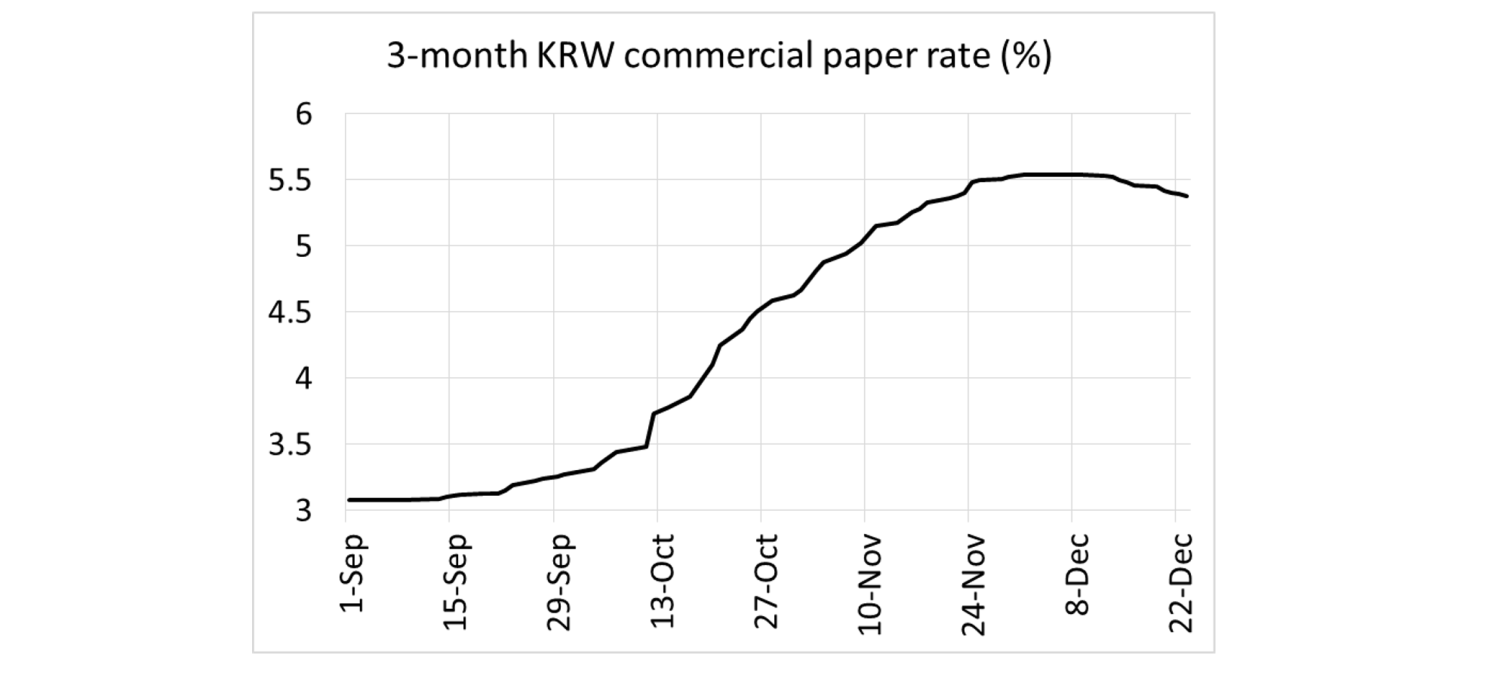

The associated surge in the short-term borrowing cost can be seen from the three-month Korean won commercial paper (CP) rate in Figure 1. The rate, which was on a gradual upward path due to a series of rate hikes by the Bank of Korea prior to the default, started to climb up rapidly. The increase in the borrowing costs did not abate even after Gangwon province vowed to pay back the entire debt on 21 October to respond to mounting criticism (the debt was fully paid on 12 December). The about-face of Gangwon province three weeks after the decision to renege on its promise bolsters the fact that the initial decision was political, not driven by financial pressure on the province.

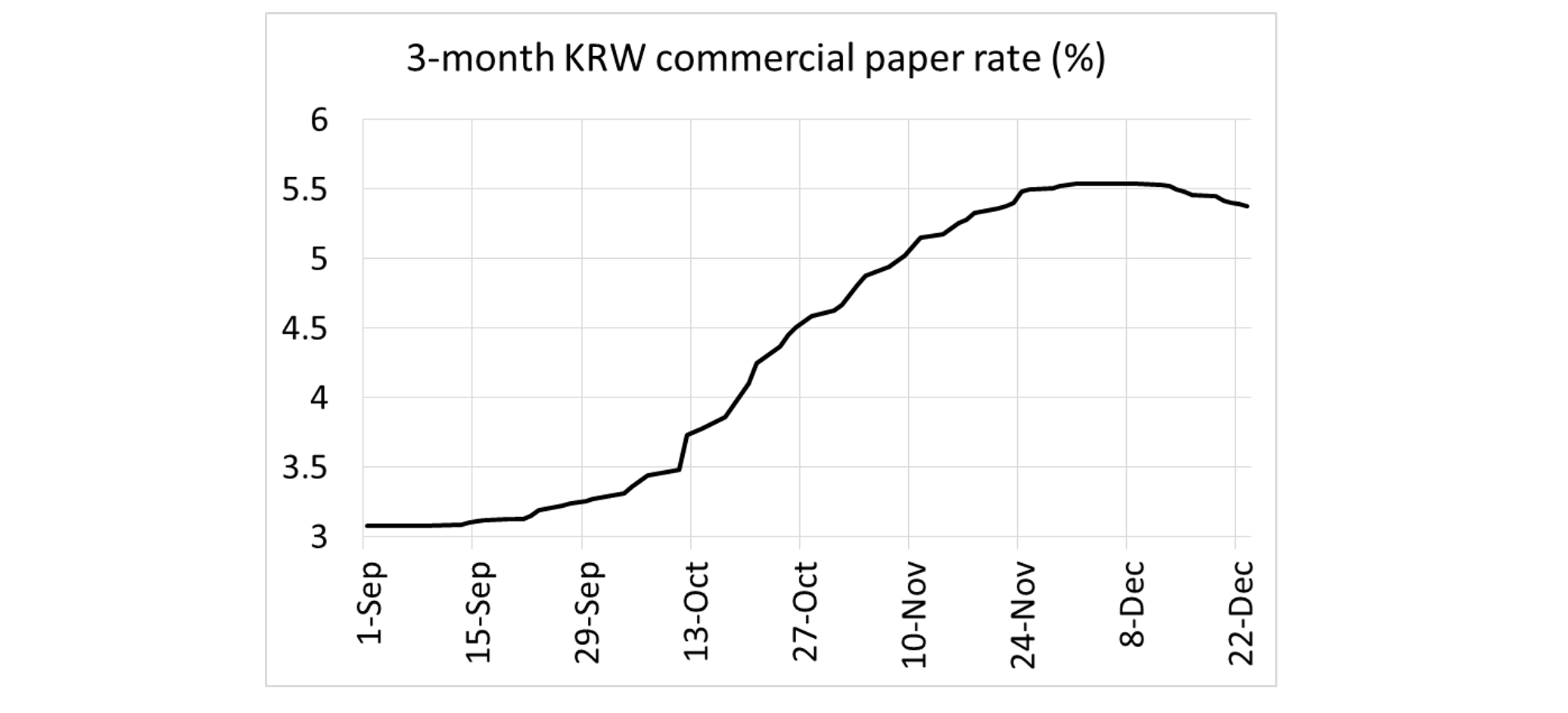

In this period, some of the most trustworthy Korean corporations, even AAA-rated ones, failed to find buyers for their bonds (Kim et al. 2022). The contagion to the broader markets is well-captured by the credit spread in Figure 2, measured by the bond yield spread between three-year corporate (AA-rated) and government bonds. The credit spread reached 1.3% by 21 October, leading to an outcry in financial markets and the Gangwon province’s response.

Figure 1 Three-month Korean won commercial paper rate

Source: Bloomberg

Figure 2 Three-year corporate (AA-rated) government bond yield spread

Source: Bloomberg

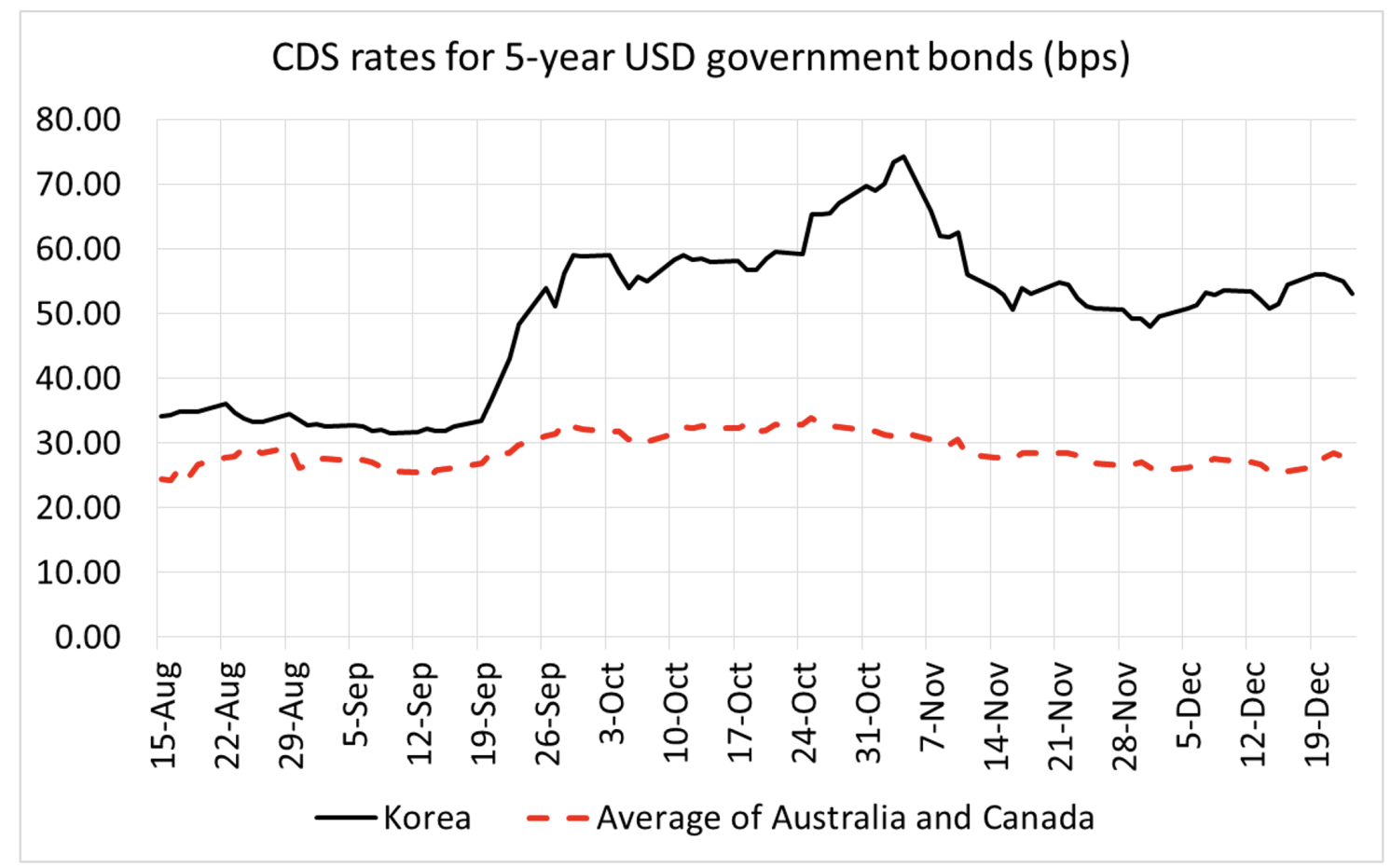

During this period, driven by central bank rate hikes in many countries, global financial conditions were becoming tighter, and the UK gilt market was having a meltdown which spread to financial markets elsewhere (Stubbington and Duguid 2022). We compare the credit default swap (CDS) rates – insurance premium – for dollar denominated Korean government debt to those of Australia and Canada, two countries that are similarly small open economies with inflation rates above their central banks’ targets hence going through rate hikes while facing slowing output growth.

Figure 3 plots the credit default swap rates for five-year US dollar government bonds for Korea (black solid line) as well as the average of the same for Australia and Canada (red dashed line). Prior to the default announcement on 28 September, the Korean credit default swap rate reacted more strongly to the external shocks originating from the UK and the US than those for Australia and Canada, but these countries nonetheless shared upward trends. After the default announcement, which was an exclusive domestic event for Korea, they began to drift away clearly: in the days after the miniscule GJC default, the Korean sovereign credit default swap rate increased by about seven basis points more than the Canadian and Australian average relative to the values on 27 September. This difference-in-differences continued to rise, reaching 18 basis points by the end of October as the figure shows. Our calculation suggests that the default driven by the negative political shocks meaningfully worsened the risk perception about the entire economy, consistent with media narratives (Kim 2022a).

Figure 3 Credit default swap rates for five-year US dollar government bonds

Source: Bloomberg.

Policy responses and resolution

The Korean government reacted to the credit market crisis belatedly, but it went all out when it did. It first announced the reactivation of the bond stabilisation fund established during the pandemic on 20 October (Cho 2022), followed by a joint meeting of the central bank governor, the finance minister, and other senior policymakers on 23 October where at least 50 trillion won (around $35 billion) of government interventions were announced (Kim 2022b), more than 240 times the size of the original default. The magnitude of the intervention and holding the meeting on a Sunday indicate that the government perceived the gravity of the situation.

On 27 October, the Bank of Korea announced temporary collateral easing measures for its lending facilities amidst the ongoing rate-hike cycle, reminiscent of the dilemma the Bank of England faced due to the mini-budget induced fiscal crisis. This was followed by a series of public and private sector measures to improve the credit market conditions, but as Figures 1 and 2 show, the difficulties continued into November, with the three-month commercial paper rate and the three-year credit spread beginning to fall only in December.

The intervention was very costly and pushed the Bank of Korea to face in earnest the trade-off between price and financial stability, its mandates. On 1 January 2023, the Bank of Korea governor Changyong Rhee remarked that the central bank is likely to face an increasing conflict between its policy goals (Yoo 2023).

Conclusion

Countries find innovative ways to shoot themselves in the foot. These range from inane monetary policy in Turkey (Gürkaynak et al. 2022), to inane fiscal policy in the UK, to inane refusals to honour a small loan guarantee in Korea. The last one sounds much less consequential than the first two, but it turned out to have major systemic effects. The Korean episode was not one of multiple equilibria where the minor default acted as a focal point; it was an episode where the financial market participants learned that previously unthinkable refusals to honour loan guarantees by local governments were possible, which changed the risk perception for the entire financial system. As this case study shows, even minor political shocks can snowball into an avalanche in times of elevated uncertainty and policymakers need to be mindful of this source of risk. The blurred boundary between fiscal and monetary policy following the covid pandemic makes this endeavour ever more challenging. This challenge will be present for policymakers around the world who should think about the tools and the communication of macroprudential policy at times of tight monetary policy.

Source :-CEPR

")

")

.jpeg")

")

")

")

")

")

")