The 2025 Sevilla Commitment renews the push for domestic revenue mobilisation, with the EU needing stable, targeted support for low-income partners.

Mobilising domestic revenue in lower-income countries has become more urgent in the face of rising debts, tighter global financial conditions, climate pressures and weakening aid inflows. In this context, the 2025 Sevilla Commitment, in the context of the United Nations Sustainable Development Goals, marked an important political step. Donors pledged to collectively at least double support for domestic revenue mobilisation (DRM) in partner countries by 2030, especially those countries seeking to raise tax-to-GDP ratios to at least 15 percent. This Policy Brief argues that the European Union, as one of the largest donors for DRM, should play a central role in turning that pledge into credible action.

Donor support for DRM in low-income countries is justified by several closely linked goals: financing domestic development, enhancing the stability and predictability of public finances, reinforcing state-building processes, advancing donors’ own long-term financial interests and the growing empirical evidence that external assistance can effectively strengthen tax capacity.

Nevertheless, aid for DRM has been volatile and insufficient. Although the Addis Tax Initiative placed DRM firmly on the international agenda in 2015, donor disbursements have fallen short of agreed targets. The EU remains one of the largest donors, but its support fluctuates and does not consistently prioritise low-income countries.

The Sevilla Commitment and the related Seville Declaration on DRM create an opportunity to reverse this trend. The EU should provide stable annual funding consistent with its commitments, more effectively target low-income countries and those below the 15-percent threshold. It should also adopt a clearer strategy linking DRM aid to broader development strategies such as the Global Gateway, while strengthening international partnerships, for example with regional tax organisations, and taking into account tensions in its relationship with the Global South on international tax cooperation. Together, these steps would make EU support more credible, strategic and effective.

The authors thank Zsolt Darvas, Lucio Pench, Nicolas Veron, Guntram Wolff, Uuriintuya Batsaikhan and Stephen Gardner, as well as participants in the Bruegel Research Meeting, for their comments.

This Policy Brief is based on research funded by the Gates Foundation. The findings and conclusions contained within are those of the authors and do not necessarily reflect positions or policies of the Gates Foundation.

1 Introduction

Mobilising sufficient resources to finance the United Nations Sustainable Development Goals (SDGs) has become increasingly challenging for lower-income countries against the backdrop of rising debt burdens, tightening global financial conditions and mounting fiscal pressures from climate change and demographic transitions1. These pressures have been compounded by recent disruptions to the international aid landscape2.

With international aid flows under pressure, domestic revenue mobilisation (DRM) – broadly defined as the process by which governments raise and manage revenue from domestic sources to finance public spending – has become even more important as a means to finance long-term development3. The case for improving DRM is strong: it provides gov-ernments with a relatively stable source of financing to spur growth and development and can contribute to state-building. Moreover, improving DRM in lower-income countries may reduce their dependency on future development assistance, as aid for DRM can increase revenue.

In July 2025, at the Fourth International Conference on Financing for Development (FfD4) in Seville, Spain, governments adopted the Sevilla Commitment (UN, 2025a). A core element of this is a commitment to at least double aid for DRM by 2030, with particular attention paid to countries – mostly low-income – seeking to raise their tax-to-GDP ratios to at least 15 percent. While the Sevilla Commitment does not provide a reference point for this doubling, members of the Addis Tax Initiative4 have set 2015 levels as their baseline. For the EU, doubling support means raising it to $92 million from $76 million in 2023. This explicit target marks a political acknowledgement of the importance of DRM in achieving the SDGs by reducing aid dependency and underpinning investment in climate and development priorities.

This Policy Brief examines the economic and institutional case for supporting DRM and taxation in particular, reviews recent trends in donor assistance for DRM, particularly by the EU, and assesses the Sevilla Commitment. It then recommends how the EU, as one of the larg-est donors, can translate this new global pledge into stable, predictable and credible action. Thus ‘EU’ in this paper refers to the European Commission and the bodies through which it channels development finance. The bilateral programmes of EU countries that participate in international DRM frameworks are outside the scope of this paper.

2 The case for supporting DRM

Mobilising domestic public resources is a cornerstone of fiscal sustainability and economic sovereignty. In practice, DRM encompasses tax, including social security contributions, and non-tax revenues such as grants, fees, royalties and revenue from state-owned enterprises. However, taxation is the dominant source of government revenue across all country groups (Figure 1), accounting for nearly 85 percent of total revenues in advanced economies and roughly two thirds in emerging markets. Even in low-income countries where non-tax revenues play a larger role, taxes still represent around 60 percent of public revenues. As expected, grants play a much larger role in low-income countries, accounting for nearly one fifth of total revenue.

Figure 1: Composition of total government revenues, 2022

Source: Bruegel based on IMF (2024). Note: tax revenue includes social security contributions. Non-tax revenues include various other revenues except for foreign grants. The grouping of countries into Advanced Economies, Emerging Markets and Low-income Countries follows the IMF’s classification.

The case for donor countries to support DRM – particularly taxation – in developing coun-tries rests on five interrelated arguments: its role in financing development, improving fiscal predictability, strengthening state institutions, serving donors’ long-term financial interests and the empirical evidence that donor support can raise tax capacity.

2.1 Financing sustainable development

In 2015, 193 countries adopted the UN 2030 Agenda for Sustainable Development, committing them to the 17 SDGs which, among other things, aim to eradicate poverty, provide quality education and healthcare and take action to combat climate change. According to the UN (2024), the world is not on track to achieve these targets. About 600 million people will continue to live in extreme poverty in 2030, while progress on climate action is falling far short of commitments. Achieving the SDGs is estimated to require substantial collective additional investment of up to $4 trillion per year. Financing needs are especially acute in developing countries (UN, 2024).

Closing the gap will require both public and private financing. Increasing DRM will be an essential part of the effort. Tax-to-GDP-ratios across developing countries and emerging markets increased between 2000 and 2010, but progress has stalled (Figure 2)5. Low-income countries continue to collect only around 14 percent of GDP in tax revenue, far below the 20 percent typical for emerging markets and the 33 percent observed in advanced economies. This persistent gap highlights the challenges many developing economies face in expanding their fiscal space. The IMF estimates that the untapped tax potential for low-income countries and emerging markets is 8-9 percent of GDP6.

Figure 2: Evolution of tax ratios, % of GDP

Source: Bruegel based on IMF (2024). Note: tax revenue includes social security contributions.

Besides bringing in the necessary revenue for financing their developmental spending, taxation may also spur economic development in the least-developed countries. Theoretically, taxes have a negative effect on economic growth, acting as a disincentive for economic activity. Empirical evidence, mostly from Organisation for Economic Co-operation and Development (OECD) members, confirms that high tax burdens tend to correlate negatively with economic growth, though the relationship may be non-linear (Batini et al, 2014; Gunter et al, 2021; Lee and Gordon, 2005; Romer and Romer, 2010).

However, evidence for lower-income countries suggests that the potential negative impacts of taxes on growth can be more than offset by the positive effects of growth-enhancing spending programmes that they make possible. Gaspar et al (2016) found that growth accelerates once the tax-to-GDP ratio reaches about 13 percent of GDP. Choudhary et al (2024) confirmed the existence of this tipping point and argued that it can be explained by increased public spending on health and education, reduced economic volatility and progressive taxation.

Unlocking even a part of developing countries’ tax potential would not only narrow the SDG financing gap but would also contribute to economic development.

2.2 Predictability

Another central argument for strengthening taxation is that, compared to alternative sources of revenue such as aid, tax revenues tend to be more stable and predictable. Governments require reliable resources to prepare medium-term expenditure frameworks, finance multi-year infrastructure projects and sustain investments in health, education and social protection. Yet, in many developing countries, especially low-income countries, revenue streams, including taxes, can be highly volatile, for example when they are shaped by commodity prices, cyclical economic shocks or unpredictable aid flows from donors. Reducing volatility by shifting the composition of revenue towards taxation can improve fiscal planning, decrease macroeconomic risk and strengthen institutional development (Iannantuoni 2025; Borensztein et al, 2008; Fletcher et al, 2008; Arroyo Marioli et al, 2024).

The volatility of budget support (Figure 3) underscores the limits of relying on aid for core public spending. Annual growth rates in budget support, provided by members of the OECD Development Assistance Committee (DAC)7, exhibit extreme swings, ranging from double-digit contractions to surges of 80-100 percent in single years. Part of this volatility reflects the fact that aid often rises in response to crises. However, aid supports sustained investment in long-term development, which requires more predictable financing than crisis-driven surges.

Figure 3: Annual growth rate of total budget support provided by DAC countries

Source: Bruegel based on OECD CRS data. Note: figures based on disbursements of budget support in constant $ millions by DAC countries. DAC members are: Australia, Austria, Belgium, Canada, Czechia, Denmark, Estonia, the EU, Finland, France, Germany, Greece, Hungary, Iceland, Ireland, Italy, Japan, Korea, Latvia, Lithuania, Luxembourg, the Netherlands, New Zealand, Norway, Poland, Portugal, Slovakia, Slovenia, Spain, Sweden, Switzerland, the United Kingdom and the United States.

Figure 4: Volatility of revenue sources in emerging and developing economies, 2000-2022

Source: Bruegel based on IMF (2024). Note: volatility is calculated as the standard deviation of annual percentage changes in each revenue category over the period of 2000-2022. This cap-tures how much revenues deviate from their average growth rate over the sample period. A higher value indicates less predictable and more unstable revenue flows.

The comparative volatility of domestic revenue sources further strengthens the case for prioritising taxation. Tax revenues are by far the most stable component of government financing in emerging and developing economies (Figure 4). Their volatility is minimal (around 2 percent) reflecting their broad base and close link to domestic economic activity. Non-tax revenues, excluding grants, exhibit much higher volatility (around 9 percent). Grants are the least stable, with volatility exceeding 10 percent. This pattern mirrors long-standing findings in the literature: taxes are significantly less volatile than non-tax sources and far more predictable than aid8 (Bulíř and Hamann, 2008).

Together, these figures illustrate that reliance on non-tax resources exposes governments to high levels of revenue uncertainty. The challenge for governments is to build robust and diversified domestic tax systems that provides the fiscal stability required to undertake long-term development strategies. Strengthening tax systems is therefore not only a matter of raising revenue, but also of enhancing budget predictability and resilience.

2.3 State-building

Beyond fiscal considerations, taxation is central to state-building; taxation fundamentally shapes the relationship between the state and its citizens. The literature on taxation and the social contract highlights several channels through which tax mobilisation promotes state-building. Moore (2008) and Prichard (2015) argued that taxation can trigger bargaining dynamics, whereby citizens demand transparency, accountability and better governance in exchange for paying taxes. These processes help build more responsive and accountable institutions (Dom et al, 2023). Improvements in tax systems can also strengthen trust in government, which in turn fosters tax compliance, especially when accompanied by visible improvements in public service delivery and increased accountability (Dom et al, 2022).

The state-building role of taxation is especially important in fragile and conflict-affected states where weak institutions, limited administrative capacity and low levels of trust often undermine fiscal capacity. Van den Boogaard (2020) demonstrated that even in highly informal or conflict-affected contexts, taxation can foster meaningful state-society engagement. Local-level revenue collection in particular can create spaces for negotiation, enhance perceptions of fairness and slowly rebuild administrative presence and legitimacy (Van den Boogaard and Santoro, 2023). When the social contract is fractured, modest improvements in the equity, consistency and transparency of tax systems can have significant effects on state legitimacy.

This underscores that DRM, especially via tax collection, is not merely a technical exercise aimed at increasing government income; it is a core component of building effective, legitimate, accountable states. Strengthening tax systems can support broader objectives of institutional development and democratic governance.

2.4 Donor interest and aid effectiveness

From a donor perspective, supporting DRM can also improve the long-term effectiveness of development cooperation when traditional aid budgets are under pressure. As domestic tax capacity expands in recipient countries, structural reliance on external transfers declines, reducing future aid demands on donors. In this sense, DRM support aligns donor interests with recipient needs. It is both an efficient use of public funds and a pathway toward domestic fiscal ownership.

If DRM plays such a central role in development and DRM support aligns with donor interests, a key question is whether donor support is effective in raising tax capacity. Empirical research provides growing evidence that aid, in particular aid for DRM, can raise tax performance. While earlier debates suggested that aid may discourage taxation (Djankov et al, 2008), a review of the evidence shows that there is no systematic effect by aid on taxation (Morrissey et al, 2014; Morrissey, 2015).

The composition of aid appears to matter: official development assistance (ODA) grants, as opposed to ODA loans, have been associated with lower revenues (Benedek et al, 2013). Evidence focusing specifically on DRM assistance is more positive. Technical assistance for tax administration and tax policy is associated with measurable improvements in tax revenues, especially in low-income countries (Chami et al, 2022). Importantly, these effects are not confined to stable environments. Complementary evidence shows that similar, positive relationships hold in fragile and conflict-affected contexts (Diarra et al, 2023).

Practical experience reinforces these findings. The Tax Inspectors Without Borders initiative (see section 3) has helped participating countries mobilise an additional $2.4 billion in revenue to date, including $1.91 billion in Africa alone9. However, effectiveness depends on how support is delivered. Fragmented donor engagement reduces impact by increasing administrative burdens and weakening reform coherence (Compaoré and Tagem, 2025). Taken together, the literature suggests that aid for DRM does not merely finance reforms; it can strengthen fiscal capacity.

3 Aid for DRM before Seville

International support for DRM has a long history (Dom and Miller, 2018), but it has become firmly embedded in the global development financing agenda only over the past decade. While taxation was part of the earlier international conferences on Financing for Development in Monterrey (2002) and Doha (2008), the conference in Addis Ababa in 2015 marked a turning point by explicitly placing DRM at the centre of the international financing architecture, with the adoption of the Addis Ababa Action Agenda on Financing for Development. This followed the adoption of the SDGs the same year, including a dedicated DRM target10, calling on countries to improve domestic capacity for tax and other revenue collection, including utilising international support for developing countries.

In Addis Ababa, issues related to the taxation of cross-border economic activity were heavily debated, with a push to upgrade the UN’s work on taxation. The UN Development Programme and the OECD launched the Tax Inspectors Without Borders Initiative (TIWB), to provide hands-on technical assistance to tax administrations in developing countries by deploying experienced auditors to work alongside local officials on real tax audit cases, particularly in international taxation. Meanwhile the IMF, the OECD, the UN and the World Bank started discussing the establishment of the Platform for Collaboration on Tax. The conference also spurred the governments of Germany, the Netherlands, the United Kingdom and the United States to back the Addis Tax Initiative (ATI) to support the implementation of the Addis Agenda, notably on tax matters11.

Figure 5: Timeline of key DRM events

| 2002 | 2008 | 2015 | 2020 | 2025 |

| FfD1, Monterrey | FfD2, Doha | FfD3, Addis AbabaAddis Ababa Action AgendaAddis Tax Initiative (ATI)ATI Declaration 2015 | ATI Declaration 2025 | FfD4, SevillaSevilla CommitmentATI Seville Declaration on DRM |

Source: Bruegel. Note: FfD = International Conference on Financing for Development. Bold indicates FfD-related events; italic indicates ATI-related events.

The ATI Declaration of 2015 laid out three core commitments for its members. First, ‘development partners’ (ie donor countries) were called on to collectively double funding for technical cooperation for DRM by 2020. Second, ‘partner countries’ (ie recipient countries) committed to stepping up DRM as a key requirement for achieving the Sustainable Development Goals and fostering inclusive development. Third, all ATI members agreed to promote policy coherence for development (ATI, 2015). In 2020, ATI members adopted the ATI Declaration 202512, reaffirming their commitment to the implementation of the Addis Agenda, reflecting the importance of DRM for financing the 2030 Agenda for Sustainable Development.

Under Commitment 2 of the ATI Declaration 2025, ATI development partners collectively committed to maintain or surpass the 2020 global target level ($441.1 million) of DRM support for reforms designed and led by recipient governments themselves. ATI Monitoring Reports, however, show a downward trend (Figure 6) in funding for Commitment 2. Total ODA disbursements for DRM peaked at $382.9 million in 2016 but have since fluctuated, falling consistently below the 2020 target (ITC, 2024). In 2020, disbursements stood at $352.7 million, but by 2023 had declined further to just $281.1 million, representing a shortfall of 36 percent (or $160 million) relative to the agreed benchmark of $441 million13. This persistent underperformance signals a failure among ATI development partners to meet their collective commitments and undermines the credibility of the ATI’s efforts to scale up financing for tax reform. If current trends continue, there is a risk that Commitment 2 will remain unfulfilled, jeopardising the ATI’s broader mission to strengthen domestic revenue systems and support sustainable development in partner countries.

Within this broader pattern of underperformance, the EU has remained one of the largest donors for DRM, providing 27 percent of total ATI funding in 2023. EU institutions and EU member states together account for the largest shares of total DRM support throughout the period, consistently exceeding any other donor bloc, including the United States (Figure 6). While the EU’s contributions fluctuate, they remain structurally dominant. This leadership is consistent with the EU’s emphasis on DRM as a pillar of sustainable development14. As a result, shifting EU priorities have system-wide implications: sustained engagement can stabilise global support for tax reform, while retrenchment would strongly affect overall DRM financing.

Figure 6: ODA disbursements for DRM by ATI development partners ($ 000s)

Source: Bruegel based on ATI Monitoring Data 2015-2023.

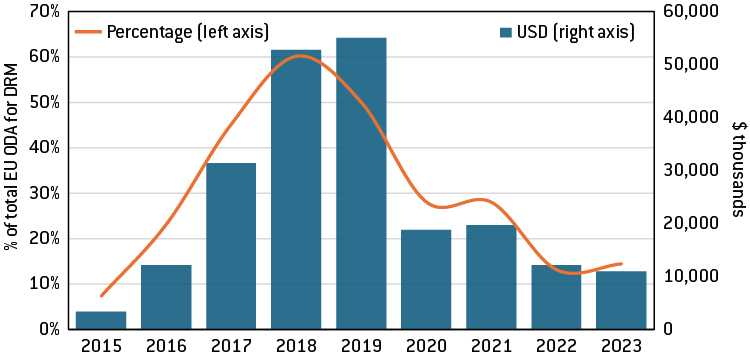

EU support for DRM has been marked by some volatility (Figure 7). Aid from the EU increased steadily following the launch of ATI, rising from the 2015 baseline to a peak in 2019. This upward trajectory was abruptly reversed in 2020 when EU support for DRM fell by 40 percent. At the time, EU development assistance was substantially reallocated toward emergency pandemic response15. While this could explain the immediate decline in DRM support as a crisis-driven reprioritisation, DRM-related disbursements never fully recovered, suggesting a more structural decline in the emphasis on DRM, rather than a purely temporary diversion of resources. Funding has fluctuated considerably since and totalled $76 million in 2023, still below the EU’s target of around $92 million16.

These trends highlight both a challenge and an opportunity for the EU. While recent years indicate difficulties in sustaining support for DRM, the 2019 peak and 2022 level demonstrate that reaching the target is feasible within existing institutional and budgetary constraints. The key issue for the coming years is therefore not capacity, but political prioritisation and the ability to restore a stable and predictable funding trajectory for DRM support.

Figure 7: ODA disbursements to DRM by EU institutions ($ 000s)

Source: Bruegel based on ATI Monitoring Data 2015 -2023.

Beyond aggregate volumes, the allocation of EU aid for DRM across income groups has also varied over time. The share of EU aid for DRM going to low-income countries (LICs) increased sharply between 2015 and 2019, peaking at just under two-thirds of total disbursements (Figure 8). This pattern was well aligned with the development case set out in section 2, and with the Sevilla Commitment, which explicitly prioritises countries seeking to raise tax-to-GDP ratios to the 15 percent benchmark, a group that overlaps heavily with low-income countries.

Since 2019, however, this focus appears to have weakened. Both the share and the absolute level of EU aid to LICs for DRM declined sharply during the pandemic period, falling from $55 million in 2019 to about $11 million by 2023. The share of EU aid flowing to LICs for DRM fell correspondingly, reaching around 13 percent of total disbursements in 2022 with only a modest recovery in 2023. The data suggests that, despite the strong economic and development rationale for prioritising LICs, EU support for tax capacity in the poorest and most fiscally constrained countries has been particularly exposed to post-COVID-19 budgetary reallocations.

Figure 8: Share of EU institutions’ ODA allocated to low-income countries for DRM

Source: Bruegel based on ATI Monitoring Data 2015-2023. Note: countries are classified according to income status following the World Bank classification by year. The figure should be read as showing a lower bound on EU aid for DRM to LICs, as about 23 percent of EU aid for DRM for 2015-2023 cannot be allocated by income level as it comprises aid to, for example, multilateral organisations or regional organisations. This aid may wholly or partly be destined for LICs as well. Additionally, a limited part of the decline in the LIC share reflects income reclassifications rather than allocation changes. Some countries moved from low- to lower-middle-income status during the period, mechanically reducing the measured LIC share. A robustness check holding country classifications constant confirms that while the levels change, the overall pattern remains the same.

In sum, the decade leading up to Sevilla was marked by major milestones, such as the Addis Agenda and the creation of ATI, but also by volatility in aid to DRM and persistent underperformance against targets. For the EU, DRM support has remained significant, but it has been characterised by fluctuations over time and a lack of consistent prioritisation of low-income countries. At the same time, experience shows that higher and more focused EU engagement is feasible. This mixed record highlights both the risks and the opportunities facing the new global ambition. The Sevilla Commitment must not only reverse declining trends but also restore credibility to international promises on DRM. The next section examines how the Sevilla Commitment seeks to achieve this and what it implies for the EU’s role going forward.

4 The Fourth International Conference on Financing for Development

4.1 The Sevilla Commitment

The Fourth International Conference on Financing for Development (FfD4), held in July 2025 in Seville, Spain, unfolded against the backdrop of mounting fiscal pressures for developing countries. Rising debt burdens, tighter global financial conditions, and intensifying impacts from climate change and demographics have left many governments struggling to mobilise sufficient resources to finance the SDGs, which remain severely off-track17.

The Sevilla Commitment, the outcome document of FfD4, reaffirms the importance of strengthening tax systems and includes calls to broaden the tax base, promote progressivity, efficiency, accountability, transparency and effective taxation of natural resources in develop-ing countries. To this end, development partners are called upon to:

“…collectively at least double this support to developing countries by 2030. This increase should be targeted at developing countries aiming to increase tax-to-gross domestic product ratios, especially those seeking to increase their ratios to at least 15 per cent” (UN, 2025).

An open question, however, is the baseline against which ‘doubling’ is measured. The benchmark is left undefined in the Commitment. The choice of baseline will nevertheless be critical in determining whether the Commitment represents a genuine step change or a repackaging of existing efforts.

The Sevilla Commitment also anchors DRM support to the 15 percent tax-to-GDP benchmark; as discussed in section 2.1, this is often seen as the minimum threshold for fiscal sustainability. By making this benchmark a political priority, the Sevilla Commitment highlights the importance of targeting international support at those situations where fiscal fragility is greatest, typically LICs or fragile and conflict-affected states.

4.2 The Seville Declaration on DRM

While the Sevilla Commitment establishes the political framework for scaling up support for domestic revenue mobilisation, implementation occurs in part through the Sevilla Platforms for Action (SPA), complementary but independent initiatives by coalitions of countries and other stakeholders. One such initiative, focused on DRM, is the Addis Tax Initiative’s Seville Declaration on Domestic Revenue Mobilisation, the development of which was led by the EU, The Gambia, Germany, Madagascar and Norway (ATI, 2025). Underscoring the importance of the DRM agenda to the EU, this is the only SPA where the EU has taken on a leadership role.

The declaration builds on past efforts, notably on the ATI Declaration 2025 agreed in 2020, which guide ATI development-partner engagement on DRM in the years ahead and supports the implementation of the outcomes of the FfD4. Under this declaration (ATI, 2025), ATI members commit to promote “fair and effective domestic revenue mobilisation, policy coherence and the social contract through partnerships and knowledge building” by taking the following actions:

- “Action 1: ATI members commit to support enhancing DRM on the basis of fair, gender responsive and environmentally sensitive tax policies, as well as fair, efficient, effective and transparent revenue administrations.

- Action 2: ATI development partners collectively recommit to at least double the volume of DRM cooperation provided at the time the Addis Tax Initiative was established to support country-led tax reforms.

- Action 3. ATI members commit to apply coherent and coordinated policies that foster DRM and combat tax-related illicit financial flows (IFFs).

- Action 4: ATI members commit to enhance space and capacity for DRM accountability stakeholders in partner countries to strengthen the broader social contract” (ATI, 2025).

Compared to the Sevilla Commitment, the Seville Declaration on DRM provides an operational anchor by explicitly reaffirming the commitment made at the launch of the Addis Tax Initiative (ATI) in 2015 to double DRM support relative to the baseline of $220.6 million. This clarity is a strength, although it does not raise ambition. While the Commitment prioritises countries with low tax revenues, the Declaration does not explicitly reiterate this objective. However, according to the Declaration, ATI members commit to DRM cooperation in a manner consistent with the Commitment. Therefore, the implementation of the Declaration by ATI partners should align with the Commitment’s emphasis on supporting low-tax countries.

4.3 The European Commission’s endorsement

The European Commission endorsed the ATI Seville Declaration on DRM on 10 December 2025, aligning itself with the ATI framework for implementing the DRM-related elements of the Sevilla Commitment18 and committing itself to at least doubling collective support for DRM relative to the baseline at the launch of the ATI. This endorsement therefore goes beyond political support for the Sevilla Commitment, promising increased EU engagement and financing for DRM. This means increasing EU aid for DRM to $91 million by 2030, an increase of 28 percent over the 2023 level.

While current EU aid spending on DRM falls short of this target, the EU did meet the target in 2019 and 2022 (Figure 6). Given that the EU’s main development cooperation instrument NDICI–Global Europe receives roughly €9.8 billion in the 2026 budget (Council of the EU, 2026), reaching this level of DRM support would represent only a small share of the EU’s over all development spending, suggesting the constraint is not so much one of resources, but of political prioritisation.

It remains unclear how the EU’s commitment will be financed in practice, whether via additional resources or a reallocation within existing development budgets. According to the EU’s 2026 annual budget, commitments for actions supporting good economic governance, including domestic revenue mobilisation, amounted to €38 million in 2024, €35.3 million in 2025 and €44.7 million in 202619. As these funds cover a broader set of policy areas, only part is devoted to DRM. At the same time, ATI-reported disbursements consistently exceed commitments under this heading, suggesting that EU DRM support is also financed through other budget envelopes (ITC 2024). This makes the overall level of funding for DRM in the EU budget difficult to assess, though the identifiable DRM-related line items are not sufficient to achieve the Seville target.

Looking ahead, the Commission’s proposal for the next EU budget (2028-2034) foresees the creation of a new consolidated development instrument – Global Europe – which is expected to have a budget of €200 billion. However, it does not specify how much of this envelope would be allocated to DRM (European Commission, 2025a). The Commission’s proposed Global Europe instrument lists DRM as one of its geographic programming principles20, but no longer as a separate thematic programme, as it currently is in the NDICI-Global Europe instrument21. This distinction matters: a thematic programme ring-fences funding and establishes standalone accountability for DRM, whereas geographic programming leaves it to compete for resources within broader country allocations. Moreover, the draft (European Commission, 2025a) states that the “proposal provides an enabling framework through which external action policies and international commitments can be implemented,” but only includes a reference to the outcome documents of earlier FfDs, not to the Sevilla Commit-ment.

In addition, it is not entirely clear how the EU’s commitments under the Seville Declaration on DRM will be reflected in the broader EU development policy framework, most notably the Global Gateway. The Global Gateway, launched in 2021, is the EU’s flagship development strategy, focusing on investment in infrastructure development around the world (European Commission, 2021). A central pillar of this strategy is the creation of an investment-friendly environment in partner countries. In this context, the Global Gateway explicitly recognises the importance of strengthening DRM, public finance management and debt sustainability as part of the environment required to attract investment. This emphasis echoes the earlier EU approach to DRM, previously articulated through the “Collect More, Spend Better” (CMSB) framework (European Commission, 2016), which treated DRM, expenditure quality and debt management as mutually reinforcing components of sustainable development finance and state capacity.

However, it is unclear whether the CMSB framework continues to serve as the EU’s primary strategic reference for DRM and, if so, how it relates to the Global Gateway22. The evaluation of CMSB implementation found that support for domestic public finance reforms was often fragmented, with limited synergies across country portfolios and weak links to other EU interventions (European Commission, 2023). This raises questions about whether the EU has developed a more integrated approach under the Global Gateway or whether earlier coordination challenges persist. While the Global Gateway recognises DRM as part of the enabling environment for investment, it does not define the characteristics of tax systems that would support its objectives, nor does it specify how DRM assistance should be sequenced or coordinated with infrastructure investments. In practice, DRM appears embedded only implicitly within a broader narrative focused on mobilising private capital and delivering large-scale projects. As a result, the relationship between the EU’s commitment to scale up DRM assistance and its flagship development strategy remains only loosely defined.

4.4 External perceptions of the EU’s tax agenda

Beyond funding and institutional arrangements, the effectiveness of EU support for DRM will also depend on the EU’s relationship with partner countries. As argued by Saint-Amans (2024), the EU currently faces mistrust in parts of the Global South, particularly in the context of ongoing debates and reforms of the international tax system.

Historically, OECD, supported by the EU, has led international tax rulemaking, but many low- and middle-income countries therefore perceive this rulemaking as insufficiently representative of their interests and biased towards advanced economies (Christensen et al, 2020; Cadzow et al, 2023). A source of tension has been the EU’s promotion of good-governance standards, including requirements related to tax transparency and compliance with the OECD’s Base Erosion and Profit Shifting (BEPS) framework (OECD, 2013), as well as more recent reforms such as the global minimum tax (Pillar 2)23 (Harpaz, 2023).

These standards have at times been reinforced through EU instruments such as the list of non-cooperative jurisdictions (‘blacklisting’), which conditions access to EU markets and financing on compliance. Developing countries have criticised this approach as disproportionate and, in some cases, misdirected at jurisdictions that are neither major tax havens nor significant threats to a level global playing field (Cadzow et al, 2023).

Against this backdrop, a coalition of developing countries, particularly African nations, has supported a shift towards initiatives led by the UN, notably the proposed United Nations Framework Convention on International Tax Cooperation (UNFCITC)24. This initiative is widely understood as a means to rebalance power asymmetries in global tax rulemaking and better align international tax norms with development priorities, thereby challenging the OECD’s longstanding leadership (Isa et al, 2025). The fact that all EU countries voted against the UN resolution ‘Promotion of inclusive and effective international tax cooperation at the United Nations’25 further deepened the divide between the EU and the Global South, with the latter criticising the EU for not supporting developing countries’ calls for a more inclusive framework26.

These tensions are further compounded by other EU policies, such as the carbon border adjustment mechanism (CBAM) which, although not technically a tax instrument, has worsened the relationship, as it is perceived as imposing unilateral constraints on developing economies regardless of their capacity and resource constraints27.

5 How to deliver on EU aid commitments for DRM

Delivering on the Sevilla Commitment will require more than an increase in headline spending. It will demand a clear and strategic vision of what EU support for DRM is meant to achieve, where it should be targeted and how it should be delivered.

- Recommendation 1: the EU should act on its commitment to deliver stable and appropriate funding to match the Seville Declaration on DRM. The EU is the largest donor to DRM, reflecting its leadership in promoting sustainable fiscal systems globally. However, EU aid for DRM has not consistently matched its commitments under either the Seville Declaration on DRM or earlier ATI Declarations. The upcoming EU budget provides an opportunity to allocate the funds and put in place a transparent reporting mechanism. If the EU is committed to achieving its target under the Seville Declaration on DRM, then this target should also be reflected in the next EU Multiannual Financial Framework. It should guarantee that the equivalent of $92 million is available annually for DRM projects in the Global South.

- Recommendation 2: EU support for DRM should be more clearly and consistently targeted at low-income countries, particularly those countries seeking to increase their tax-to-GDP ratios to at least 15 percent, in line with the Sevilla Commitment. Through the endorsement of the Seville Declaration on DRM, the Commission committed to pursue its DRM cooperation in a manner consistent with the Sevilla Commitment, eg prioritising countries with the weakest tax capacity. The proposed regulation establishing Global Europe should be revised to include a reference to the Seville Declaration on DRM and the Sevilla Commitment. Alternatively, the programming principles of the Global Europe instrument could be revised to reflect the prioritisation of low-income countries when it comes to DRM aid.

- Recommendation 3: the EU requires a clear DRM strategy integrated with other EU development objectives. The EU should clarify the strategic positioning of DRM within its development policy by either updating the “Collect More, Spend Better” framework or by explicitly integrating DRM into existing flagship strategies, most notably the Global Gateway. In the latter case, this could take the form of a coordinated co-investment approach that systematically links support for domestic fiscal systems in partner countries with Global Gateway investments. In practice, this would mean that infrastructure investments should be accompanied by targeted assistance to strengthen tax policy, tax administration and public financial management capacities that are directly relevant to the long-term sustainability of those projects.

- Recommendation 4: leverage renewed political commitments into stronger and more sustained delivery partnerships, particularly through regional tax organisations. In regions such as Africa, where low-income countries with low tax capacity are most concentrated, institutions like the African Tax Administration Forum (ATAF) offer a credible and well-established platform for supporting domestic revenue mobilisation28. Regional organisations can combine technical expertise with peer learning, political legitimacy and a deep understanding of local constraints, making them well suited as partners in complex and long-term tax reforms. Strengthening cooperation with such partners offers a practical way for the EU to scale up support for DRM while reinforcing country ownership and regional cooperation.

- Recommendation 5: EU support for DRM should be understood and designed con-sidering the broader political economy of international tax cooperation. The effectiveness of EU assistance will depend not only on technical capacity-building but also on trust and perceived fairness in global tax governance. Persistent tensions between the EU and many low- and middle-income countries risk undermining tax cooperation. One way to start resetting the relationship is by reducing the scope of countries subject to compliance reviews related to good governance principles, particularly OECD and EU tax transparency and anti-evasion standards. The current system has required many developing countries – including those that do not pose significant risks to the international tax system – to adopt complex standards originally designed with tax havens in mind. A more proportionate, risk-based approach would focus compliance expectations on jurisdictions that present material risks to the integrity of the international tax system, while taking into account differences in capacity, economic structure, and actual exposure to cross-border tax avoidance. This may help reset the conversation onto more pragmatic grounds.

Source : Bruegel

.jpg")

")

")

.jpeg")

")

")

")

")

")

")