Economic sanctions are increasingly being used by states to penalise both other states and non-state actors. One way to assess their effectiveness in incentivising a change in behaviour is to analyse the economic harm they cause to targeted firms or entities. This column assesses the impact of US sanctions on Xinjiang Production and Construction Corps, imposed after alleged human rights abuses against ethnic minority groups residing in Xinjiang. While the sanctions imposed a substantial cost in terms of expected future profitability, the Chinese government was able to shield the targeted entities from most of the direct effects, albeit at a considerable cost.

Economic sanctions have become a popular tool used for a wide range of policy objectives ranging from nuclear non-proliferation to fighting terrorism. For example, US and EU sanctions imposed on Russia following the invasion in Ukraine have been studied in Borin et al. (2023) and Nigmatulina (2022). In recent years, new legislation in the US, EU, and other countries has been introduced to use sanctions to promote accountability for human rights abuse and corruption. A novel features of these sanctions is that they can be targeted at sub-national entities and individuals responsible for human right violations, and not only at countries. As with any other type of sanction policy, there is considerable debate about its effectiveness and limited evidence available to inform these debates.

For sanction policies to be effective, they need to be designed such that the targeted individuals and entities have an incentive to stop the contested behaviour, such as nuclear proliferation or humanitarian rights abuse. One way to assess sanction effectiveness is therefore to analyse the economic harm they cause on targeted firms or entities. For instance, Ahn and Ludema (2020) show that US and EU sanctions significantly harmed financial performance of targeted Russian firms. Draca et al. (2023) find that international sanctions imposed considerable costs on Iran’s political elite during the negotiations over its nuclear programme.

In a recent paper (Maystadt et al. 2024), we provide novel evidence of the economic cost of humanitarian sanctions imposed on a Chinese conglomerate, the Xinjiang Production and Construction Corps, over the alleged human rights abuses against ethnic minority groups residing in Xinjiang. Different from standard sanctions, they are not imposed directly on a nation state, but on individuals and economic entities. We estimate the economic cost of the imposed sanctions on firm performance of XPPC-controlled companies using stock market and firm-level accounting data.

What is the Xinjiang Production and Construction Corps (XPCC), and why were they sanctioned?

In July 2020, the US government imposed sanctions on the Xinjiang Production and Construction Corps (XPCC), a Chinese paramilitary organisation, for its alleged assault on human rights of the ethnic minority groups residing in Xinjiang. XPCC is a major policy arm of the Chinese central government and Xinjiang regional government with a mandate to maintain regional stability and promote local development. It is a gigantic state-owned enterprise and the main producer of cotton in China. XPCC has long faced serious allegations of human rights abuses within the region (e.g. Lehr 2020, Bukharin 2021, Murphy 2022), although the Chinese government has always denied these accusations.

What was the impact of the humanitarian sanctions on the XPCC?

Our analysis of the economic impact of the US sanctions on XPCC is twofold. First, using firm-level stock market data from the Shanghai and Shenzhen stock exchanges we construct a portfolio of XPCC-controlled firms and a control portfolio with firms that have no known connection to XPCC but that are similar in several observable characteristics such as industry composition and size and profitability. Using a difference-in-differences identification strategy with firm and trading day fixed effects, we estimate that the imposition of US sanctions resulted in a negative stock market return for the XPCC-controlled firms of 1.15 percentage points relative to the control portfolio of unrelated firms. In terms of market capitalisation, this caused a cumulative loss in market value of 905 million RMB ($129 million) for the targeted companies.

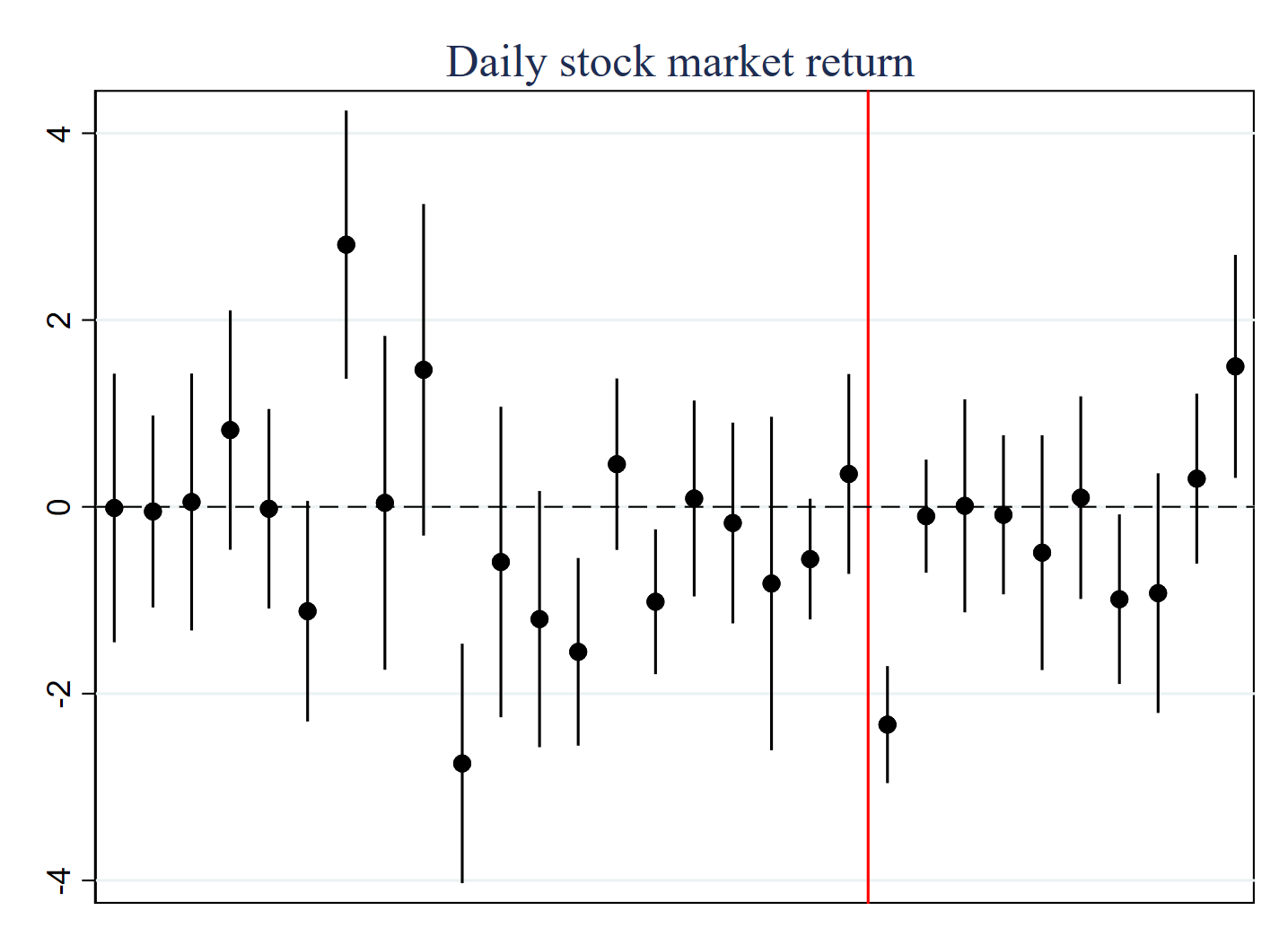

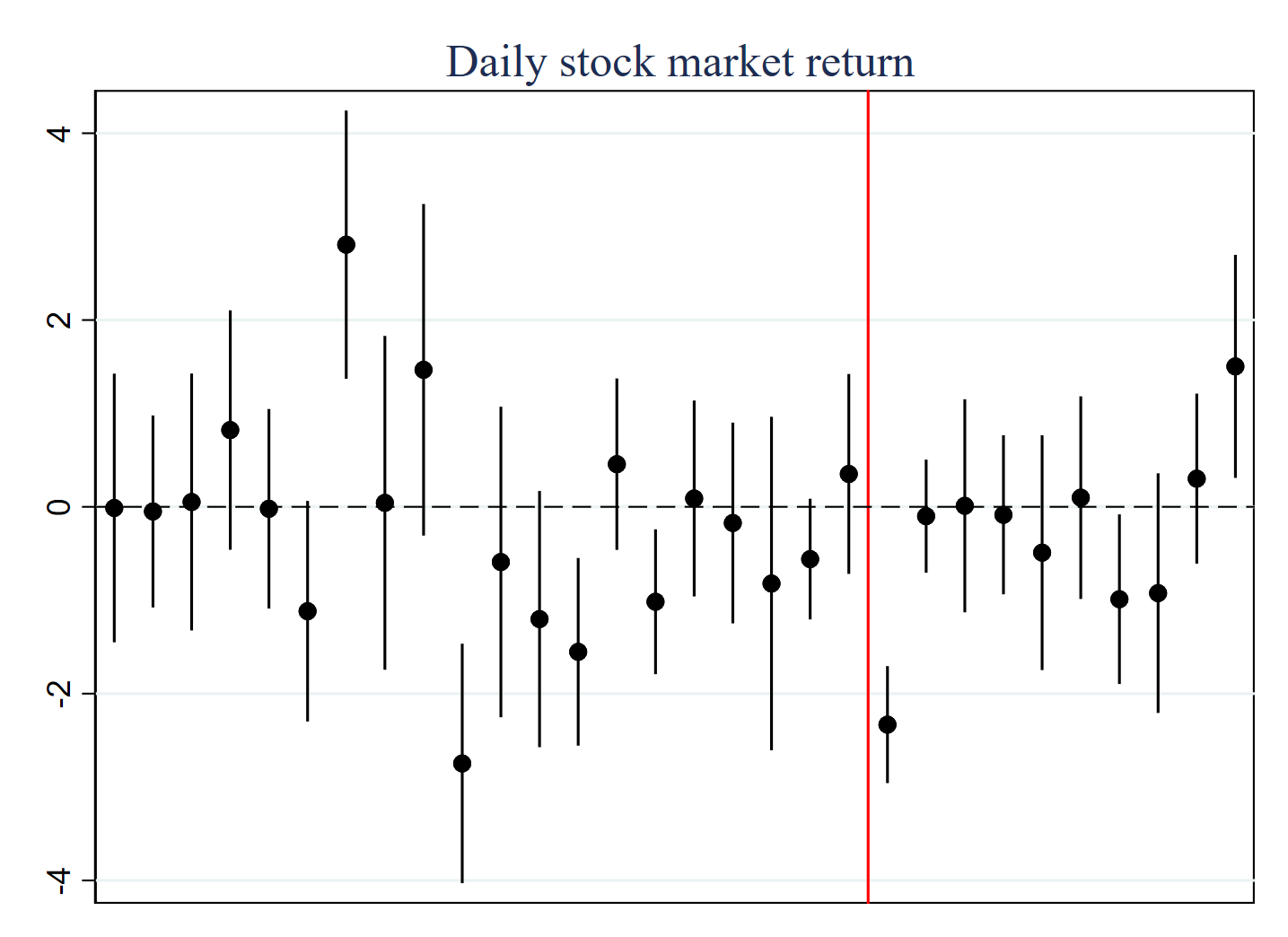

Figure 1 Event study on the stock market effect of GLOMAG sanctions on XPCC-related companies

Note: Each marker is a coefficient estimate on an interaction term between 30 consecutive trading day dummies and the targeted portfolio dummy, with the vertical segments the corresponding 95% confidence intervals. The red vertical line is placed to the left of the initial day of GLOMAG sanctions, which was 31 July 2020.

This effect is calculated over the first two trading days after sanctions were enacted. The results in Figure 1 show that the adverse impact was concentrated on the first day of the treatment period (31 July 2020), while the effects already became insignificant on the next trading day (3 August 2020). If we limit attention to the first trading day, the estimated negative stock return rises to 2.27 percentage points. The daily estimates are very noisy leading up to the imposition of sanctions, but there is no trend in the stock market returns. The imposition of sanctions was not expected by the market. Given that our event study passes the parallel pre-treatment assumption between target and control portfolios, we can interpret these baseline estimates as causal effects. The US sanctions imposition therefore clearly imposed a substantial cost on the XPCC in terms of expected future profitability.

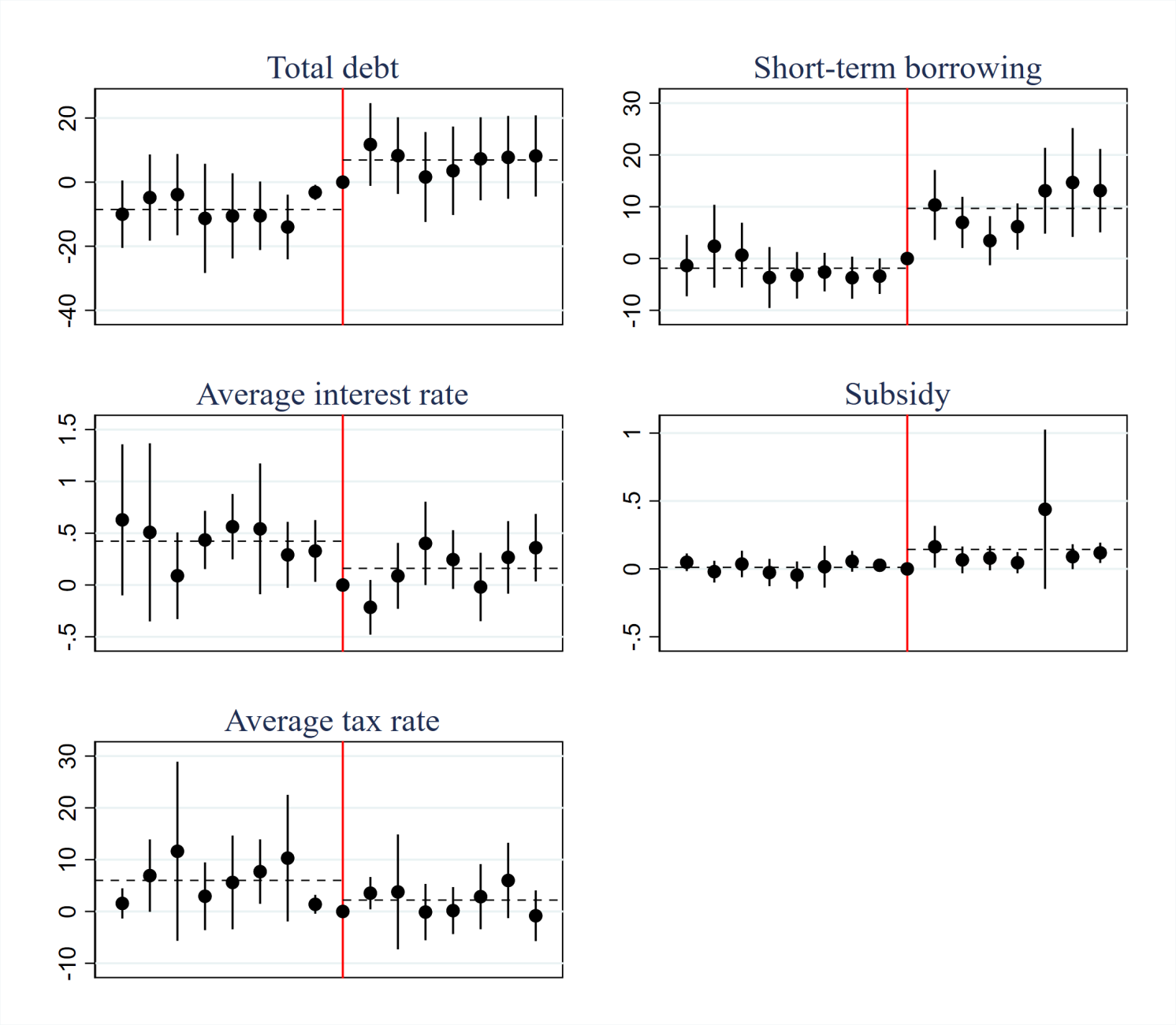

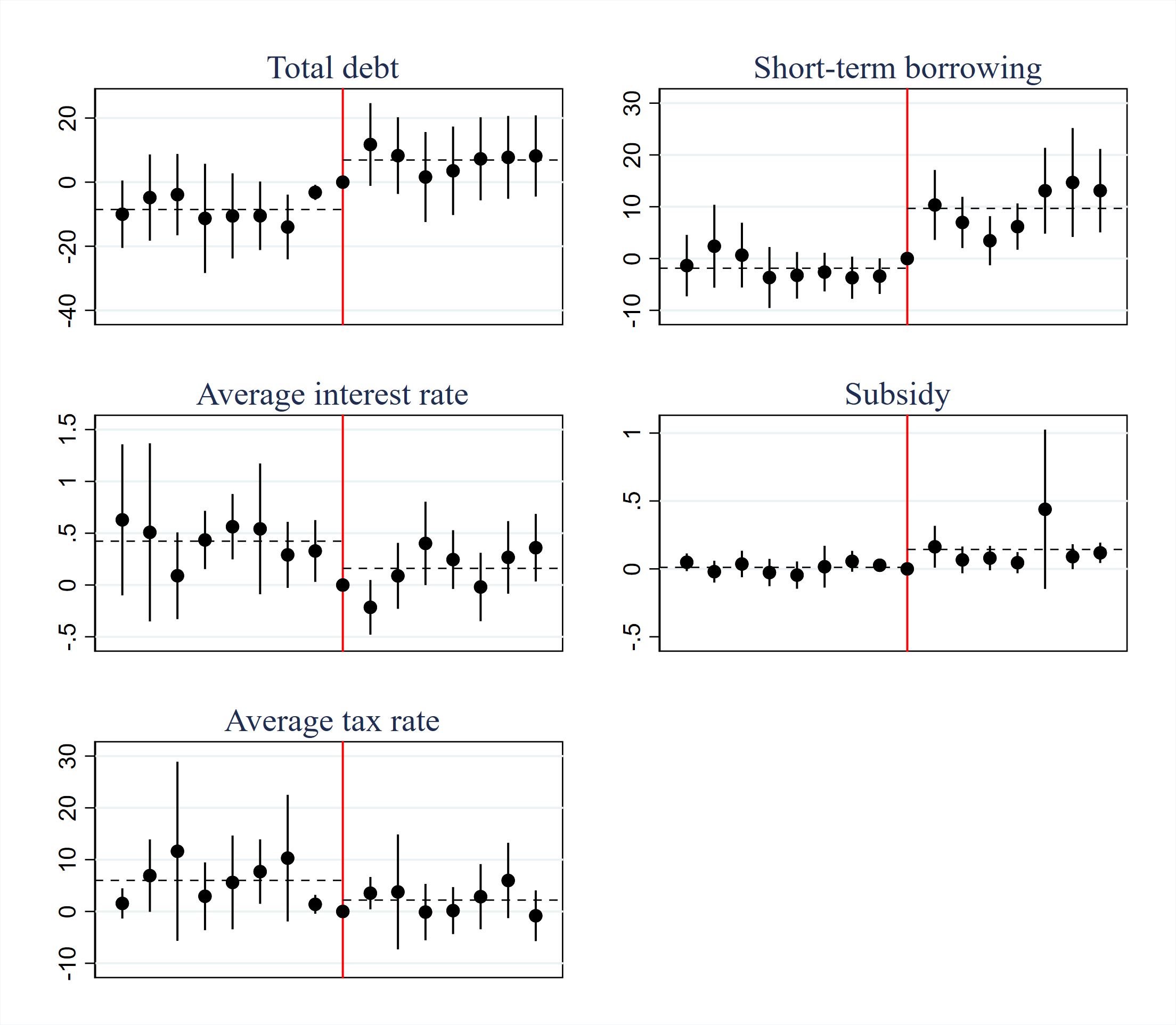

Next, we estimate the impact of the US sanctions on the financial performance of the XPCC-controlled firms by analysing quarterly firm-level accounting information before and after the sanction imposition. Using again a differences-in-differences identification strategy we estimate the impact of the US sanction on various dimensions of firm profitability, size, and liquidity. Surprisingly, we find barely any impact. There is no significant change in revenue, profits, EBIT, various asset measures, or cash flow in the XPCC-controlled firms. The only dimensions where we find a significantly worse performance are increased inventories and reduced capital expenses. Importantly, we do find that after the US sanction implementation, the targeted companies were able to borrow more, both in total and short-term, and benefited from lower interest rates. Moreover, relative to firms in the control group, they received higher government subsidies and lower tax rates. These latter effects are shown in separate event studies in Figure 2.

Figure 2 Event study on the financial effects of GLOMAG sanctions on XPCC-related companies

Note: Each marker is a coefficient estimate on an interaction term between 16 quarter dummies and the targeted portfolio dummy, with the vertical segments the corresponding 95% confidence intervals. The red vertical line is placed in 2020Q3, the first quarter of the treatment period.

The Chinese government and connected institutions (e.g. state-controlled banks) seem to reallocate resources to shield targeted companies from the effects of sanctions. This government response can explain the relatively limited impact on firms’ stock market performance, but of course it is not costless. The total cost of shielding is estimated at 14 billion RMB, or approximately $2.1 billion. This pattern is in line with a few other recent papers that found evidence that Russia also mitigated the effect of Western sanctions by supporting domestic firms. For example, Ahn and Ludema (2020) and Nigmatulina (2023) document a systematic response of the Russian regime to protect targeted companies with economic and financial support.

Concluding remarks

Our study explores the economic effects of humanitarian sanctions recently imposed by the US on Chinese companies affiliated with the Xinjiang Production and Construction Corps. Our estimates support the following conclusions:

- Although limited in time, targeted humanitarian sanctions are costly for those with direct economic interests in XPCC operations in Xinjiang. Their cumulative loss in market value is estimated at 905 million RMB ($129 million).

- The Chinese government was able to shield the targeted entities from most of the direct effects, but at a considerable cost. As a result, the financial performance of targeted firms is maintained, but the cost to the Chinese government is estimated at 14 billion RMB ($2.1 billion).

So, can economic sanctions promote human rights? The answer is yes, sometimes. Carefully targeting sanctions on those responsible for human rights abuses can impose significant costs on these individuals or entities, and create an economic incentive to uphold human rights. Sometimes though, governments might deem these targeted individuals and entities worth shielding, even at considerable cost.

Source : VOXeu

")

")

.jpeg")

")

")

")

")

")

")