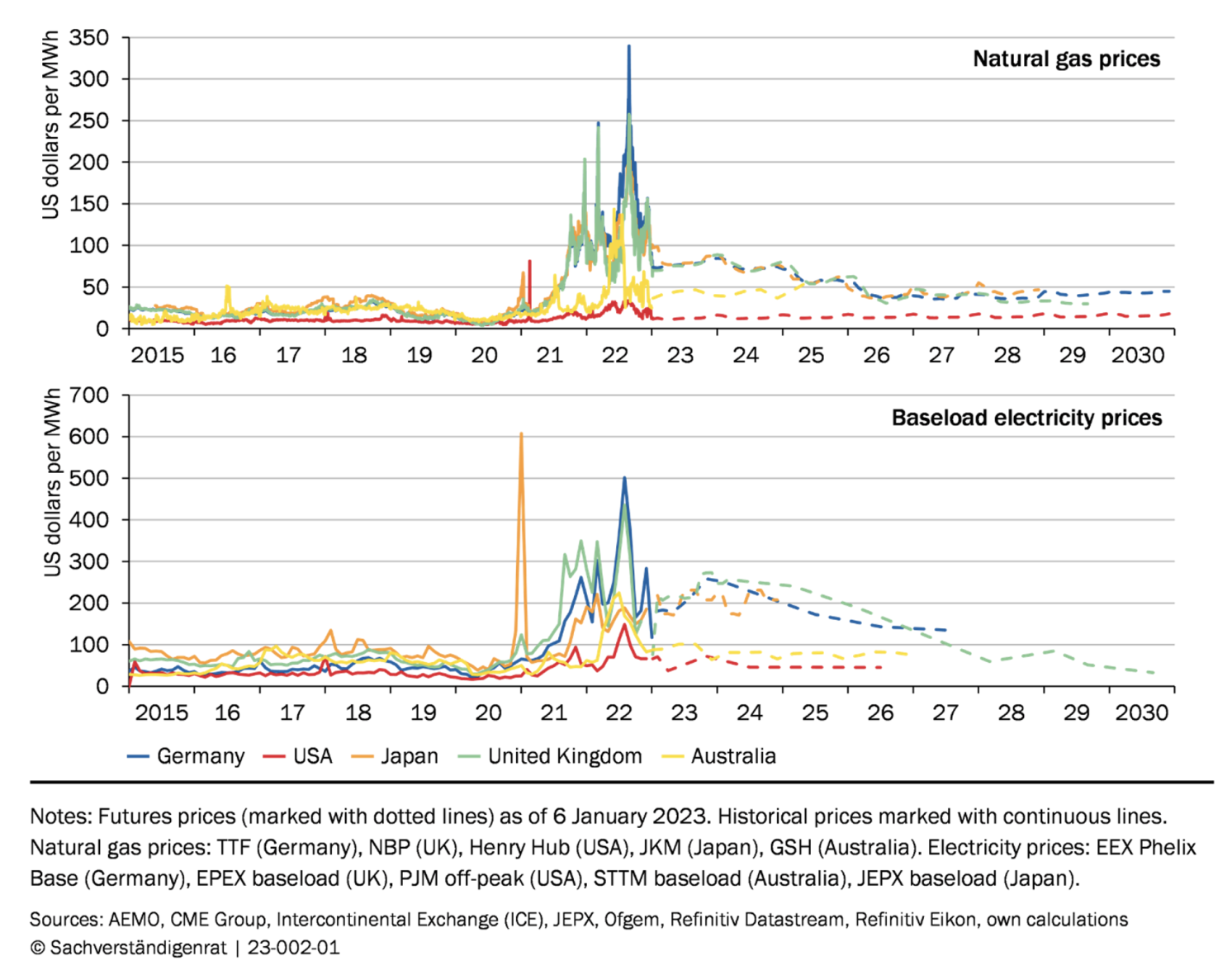

Historically, despite being high in international comparison, European energy prices did not constitute an insurmountable obstacle to industrial expansion because of the exceptional energy efficiency of the local manufacturing sector (Rezessy et al. 2015). However, the recent developments in energy markets have driven an extreme wedge between prices in Europe and some other regions, as European wholesale energy prices have reached unprecedented levels in 2022. While the price differences are expected to decrease in the next few years, European prices are likely to stabilise at levels substantially higher than the pre-crisis prices (Figure 1). This has sparked fears of a loss of competitiveness and, in consequence, of deindustrialisation. The Belgian Prime Minister, Alexander De Croo, warned that Europe risks a huge reduction in industrial activity if it does not act quickly to bring down energy prices (FT 2022). Nowhere have the fears of deindustrialisation been greater than in Germany, where manufacturing constitutes over 20% of GDP – more than in any big highly developed country.

Figure 1 Selected wholesale energy price developments in Europe

Predicting the implications of the energy crisis within the manufacturing sector and assessing which policies are appropriate to address the situation requires understanding how energy price developments in wholesale markets affect manufacturers. In this column, we discuss the factors that determine how elevated energy prices can affect industrial production in Germany and talk through policy implications. The interested reader can find additional analyses in the German Council of Economic Experts (2022).

The magnitude of final energy price increases

While wholesale prices for energy commodities have skyrocketed, their immediate impacts are limited to industrial customers who directly transact in wholesale markets and only for their unhedged energy purchases. Smaller industrial facilities contract with utilities and other intermediaries. As a result, they become affected by wholesale price developments only when higher prices are passed on to them through the intermediaries who themselves can employ hedging strategies. Contractual terms, especially price guarantees, which can be binding for up to five years, limit the pass-through.

In the short term, the final energy prices paid by manufacturers, in particular by the small ones, are thus partly shielded from wholesale developments. While wholesale day-ahead electricity prices have increased by 240%, for German manufacturers with the median annual usage of electricity of ca. 420 MWh, average electricity prices before taxes and surcharges rose by 29% in the first half of 2022 compared to the first half of 2021. In contrast, companies consuming over 150,000 Mwh experienced a 192% rise.

Over time, wholesale price developments increasingly translate into final prices for industrial customers. However, in January 2023, the German government implemented ‘price brakes’, implying that wholesale and final prices for electricity and natural gas will remain decoupled for the time the breaks are in place, i.e. likely until spring 2024.

How much does the energy price increase impact the energy costs of firms?

To understand how final energy prices for manufacturers translate into their energy costs, we need to consider the composition of energy carriers as well as the amounts of energy consumed.

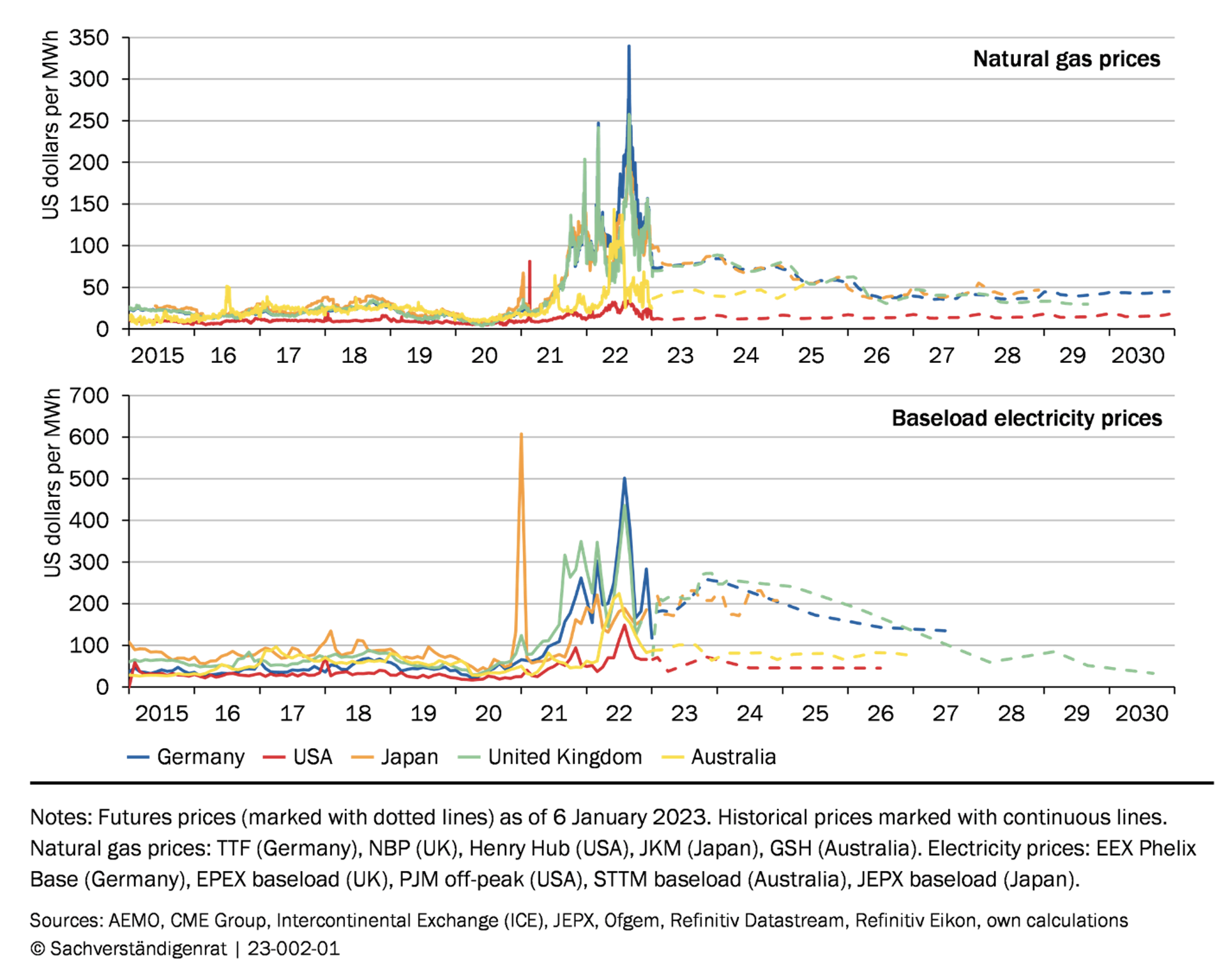

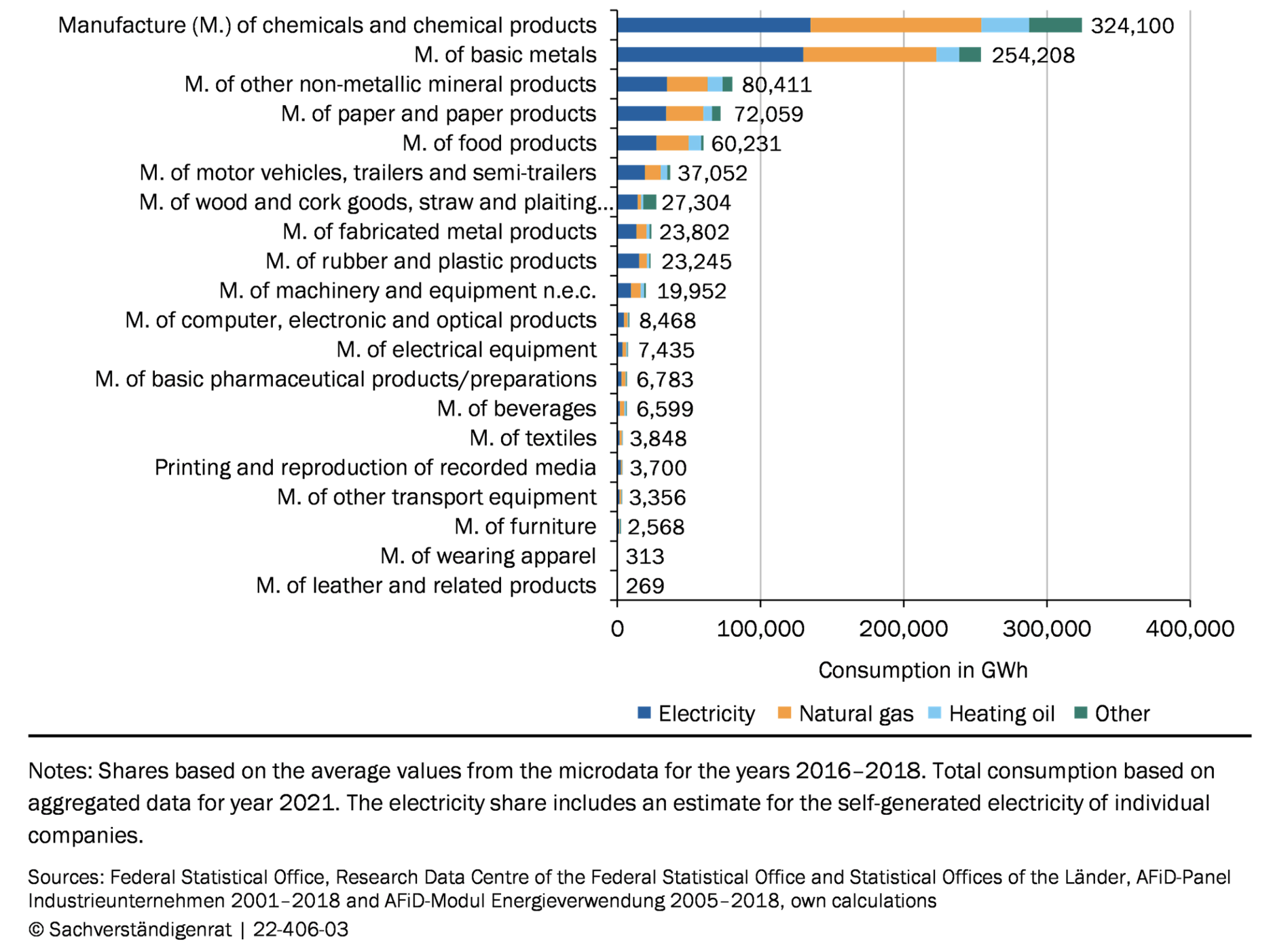

Figure 2 makes clear that absolute increases in energy costs will be unequally distributed across sectors. For instance, in Germany, the sectors most likely to experience higher costs of production imposed by extreme natural gas prices are the manufacture of chemicals and chemical products (37% of the total industrial natural gas usage), food products (11%), basic metals (10,5%), and non-metallic mineral products (9%). However, even within these sectors, the costs are not spread equally but are instead concentrated within a few products. Müller and Mertens (2022) show that out of the 1,600 product categories, 300 are responsible for almost 90% of natural gas consumption. The five products with the highest gas consumption are basic chemicals and make up around 5% of total industrial gas consumption.

Obviously, firms have the possibility to adapt in response to energy price spikes and partially offset cost increases. The empirical literature has investigated various margins of adaptation, including innovation, especially in the field of energy efficiency (Popp 2002, Hassler et al. 2021); product portfolios (Elliott et al. 2019); and production process adjustments, such as fuel switching (Brehm 2019), production shifts between plants, and increases in own electricity generation (Rottner and von Graevenitz 2022) as well as adjustments in the use of other production factors (Mertens et al. 2022). Indeed, since the beginning of the energy crisis, evidence of substantial adjustments has emerged. For example, large industrial consumers in Germany reduced their usage of natural gas by around 15% in 2022 compared to mean consumption between 2018-2021, with the majority of firms cutting their energy usage while maintaining output (Ifo 2022). However, so far, there are no estimates of to what extent these adjustments are able to buffer cost increases.

Figure 2 Industrial energy consumption in selected manufacturing sectors

The relative magnitude of the cost increase

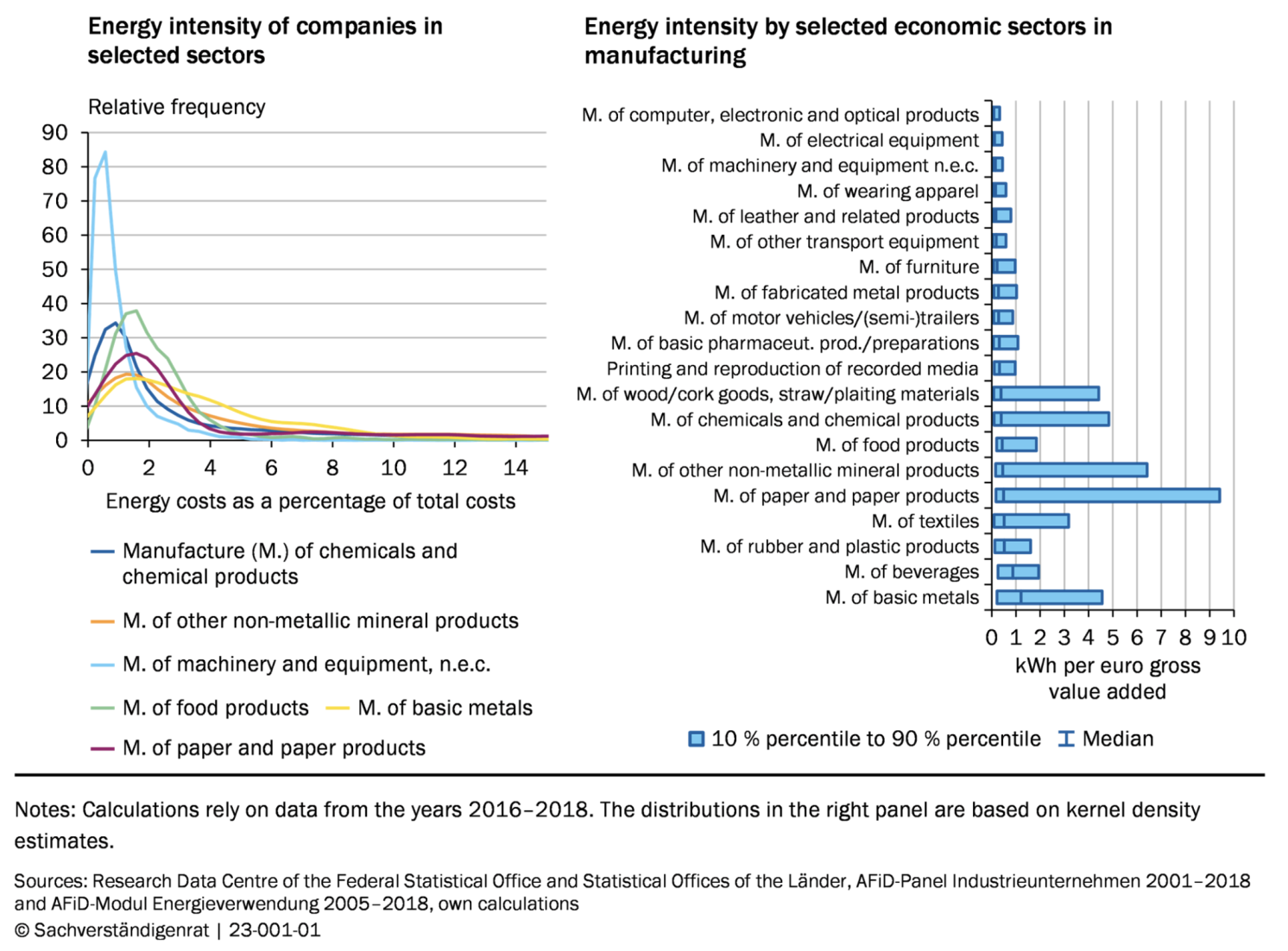

The economic relevance of the cost increases will depend, among others, on the relative magnitude of the increases. This can be measured, for instance, by the amount of energy needed to create one euro of gross value added (GVA) or through the ratio of energy costs to total costs.

An analysis of German microdata reveals a strong degree of heterogeneity, both across and within the sectors (Figure 3). While median manufacturing of machinery and equipment in the years 2016-2018 required only 0,15 kWh per euro GVA and constituted around 1% of total costs, there were individual companies with energy cost shares of around 5%. On the other hand, a median manufacturing operation of paper and paper products required 0.45 kWh per euro GVA but 10% of companies used over 9 kWh per euro GVA and had energy cost shares exceeding 15%.

Figure 3 Distribution of the relevance of energy costs within selected manufacturing sectors

Cost pass-through

The cost increases will harm companies only if they cannot be passed through to final product prices or if increased prices precipitate a loss in sales or market share. In the context of the current energy crisis, the possibilities of a pass-through are limited by non-European competitors as these have been much less affected by wholesale energy spikes than European manufacturers (Figure 1). This suggests that German manufacturers may not be able to pass on cost increases in markets where they compete against non-European producers, as is the case for basic metals – they will either need to shoulder lower profit margins, potentially even losses or lose market share.

On the other hand, competition from outside the EU is limited for industries like the manufacture of beverages, for which transport costs are high relative to value added. As such, beverage manufacturers may be more easily able to pass on the substantial energy cost increases they incur (Figure 3).

Mitigating policies

How much final energy prices affect the competitiveness of the German industry is influenced by policy measures. For instance, the carbon border adjustment mechanism together with EU-ETS2 for transportation make energy costs less relevant for upstream industries as they reduce incentives for imports. Similarly, industrial policies, like the ones targeting the battery sector, reduce the relevance of energy price impacts for supported industries. Carbon contracts for differences, on the other hand, would help companies move away from the particularly expensive natural gas and could even safeguard against energy price developments should it include automatic price adjustments as currently considered by the German government.

Energy policy can help curb wholesale price increases and thus also final prices. It also helps manufacturers move away from natural gas and invest in decarbonised production if large amounts of green energy are available at competitive prices. Here, both supply-side measures and demand-side instruments may have significant impacts. Besides accelerating the build-out of renewables, policies that expand hydrogen and electricity infrastructures and make the demand for electricity more flexible are expedient.

Policy implications

Putting these factors together provides a nuanced picture of the future perspectives for the industry in Germany. Some sectors will be adversely affected, and within individual sectors, there will be losers and winners, with the most energy-efficient producers gaining market share. Our analysis suggests that the manufacturers of basic metals, glass, textiles, and basic chemicals are at the greatest risk unless additional policies are put in place. Other sectors that are energy intensive but are partly sheltered from international competition (e.g. beverage manufacturing) are unlikely to relocate outside of Europe en masse. Those sectors that cannot escape from competition outside the EU will need to boost their energy efficiency, as some have successfully done over the last decades.

Taken together, the German industry will need to undergo a substantial structural change in the next few years, but the fears of wide deindustrialisation are misplaced. Policymakers should not hinder the transformation unless strategic industries are at play; using taxpayers’ money to halt structural change is costly and, in most cases, futile. Instead, the focus needs to be put on the measures to accompany the changes, such as retraining and reskilling workers.

This blog post is based on data from the recently published VoxEU.

")

")

.jpeg")

")

")

")

")

")

")