Divestment of polluting companies has gained traction as way for investors to incentivise the transition to a low-carbon economy. This column examines the tilting of equity portfolios to green versus brown firms internationally, and finds that investors in richer countries tend to hold relatively greener portfolios compared to investors in poorer countries. By acting as backstop owners of brown equities, investors in poorer countries could limit any positive effect of the divestment of brown equities in richer countries on the green transition.

Studies on portfolio greening by institutional investors (e.g. Boermans and Galema 2019, Benz et al. 2020, and Heath et al. 2023) prompt the question of who the purchasers of the brown assets that institutional investors sell are. For the case of the US, Pástor et al. (2023) find that large institutional investors increasingly tilt their portfolios toward green stocks, while other institutions and households increasingly invest in brown stocks. In a recent paper (Benink et al. 2024), we examine the tilting of equity portfolios to green versus brown firms internationally. We find that investors in richer countries tend to hold relatively greener portfolios compared to investors in poorer countries. This reveals that investors in poorer countries have started to act as the backstop owners of brown assets internationally. The willingness of investors in poorer countries to hold relatively brown portfolios could limit the effectiveness of divestments from brown shares by investors in richer countries in bringing about the green transition.

The carbon intensity of national equity portfolios and economic development

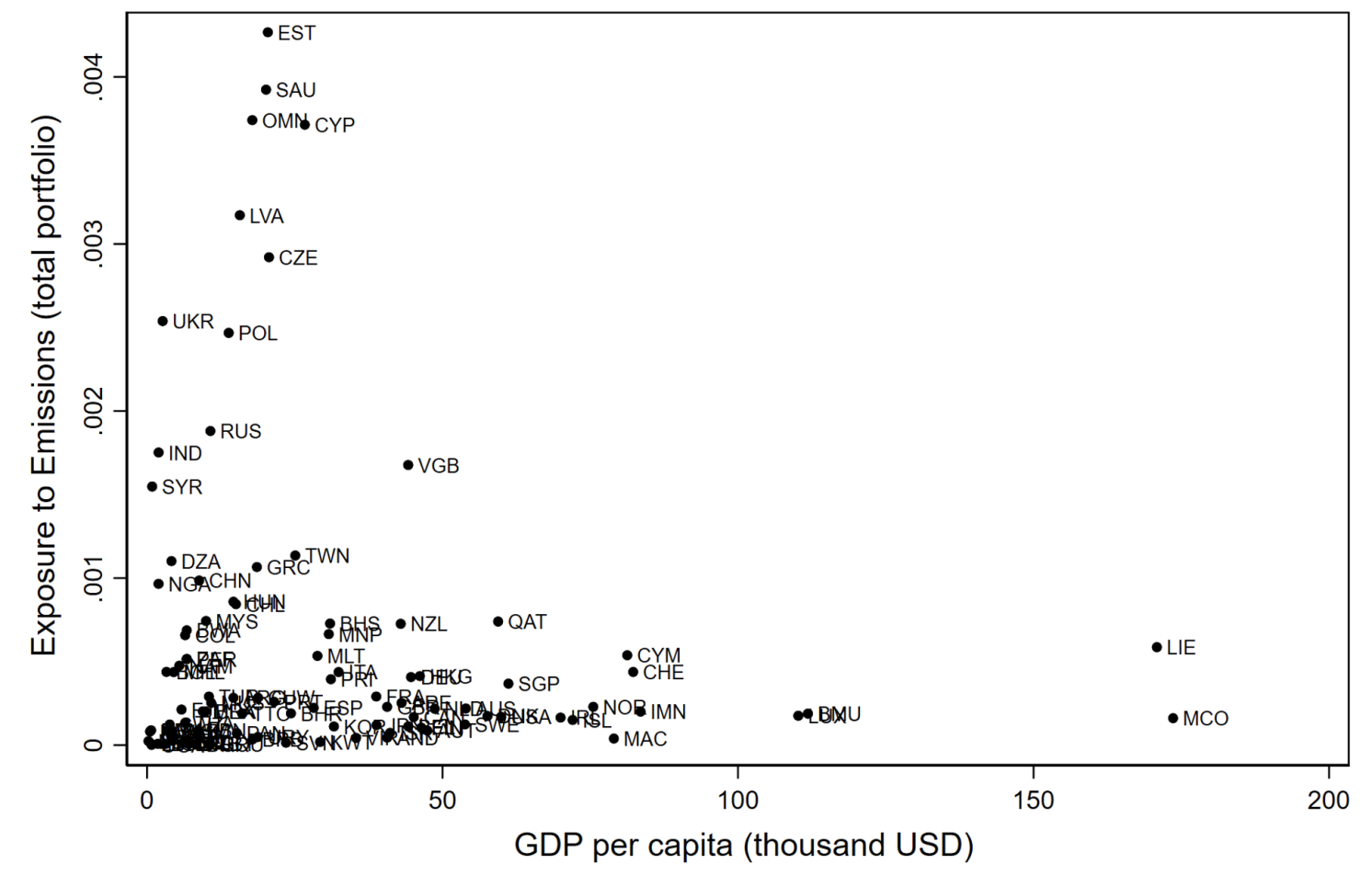

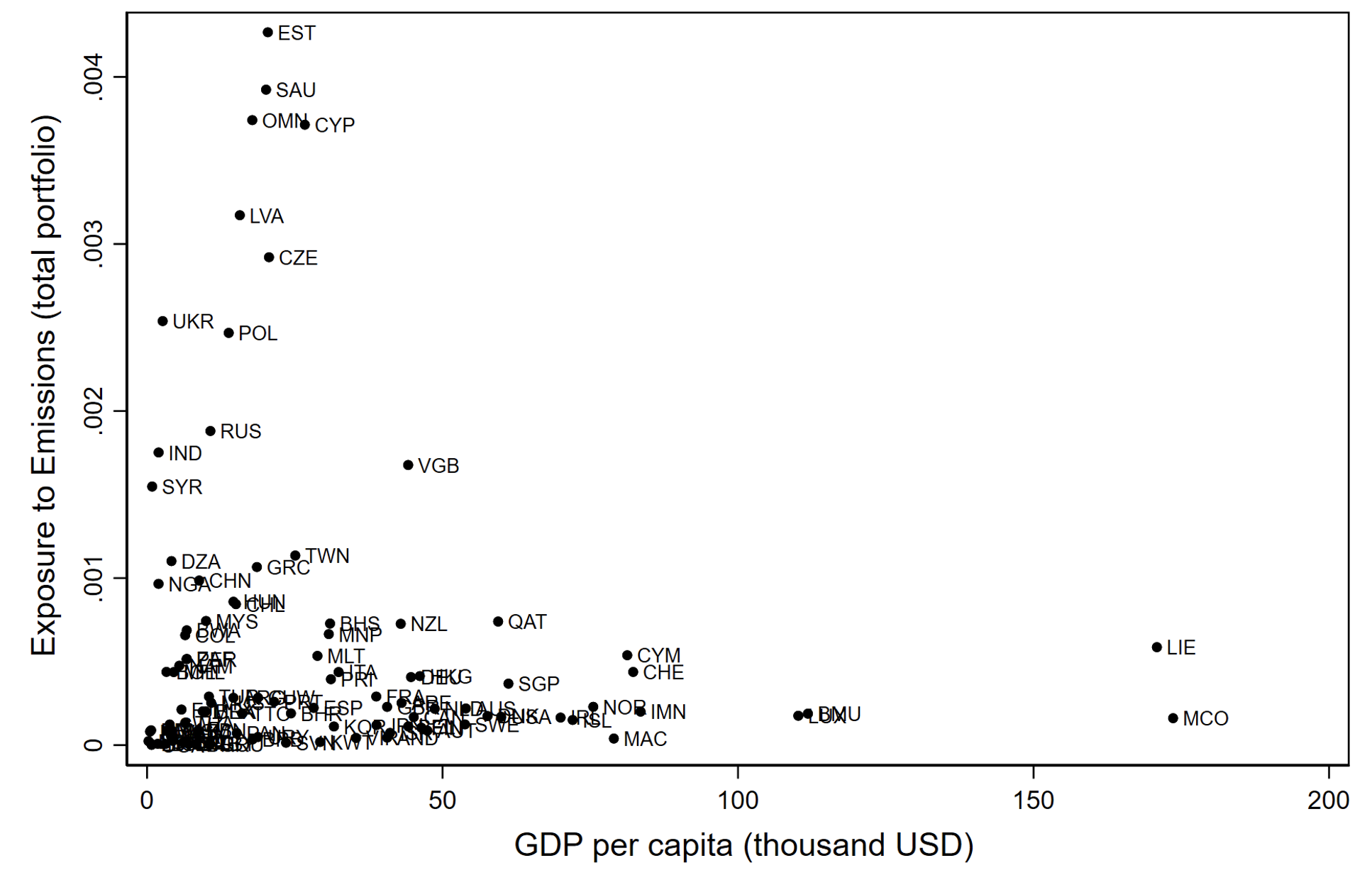

Combining information on firm-level pollution and the global distribution of firm ownership, we construct a measure of the carbon intensity of national equity portfolios. Our index for a firm’s carbon intensity is the ratio of scope 1 and 2 carbon emissions to revenues. We obtain information on the global (direct) ownership of firms from Refinitiv, focusing on firms with at least 75% ownership information. Aggregating over investors in each country, we calculate the carbon intensities of national equity portfolios as the ratio of the ownership-weighted average carbon intensity of individual shareholdings to the ownership-weighted average revenues. Figure 1 provides a scatter diagram of the carbon intensities of national equity portfolios and GDP per capita in 2017, a few years after the adoption of the Paris Agreement in 2015. The figure displays a negative relation, reflecting a correlation between national portfolio carbon intensity and GDP per capita that is negative at -0.12. Poorer countries such as India, Syria, and Ukraine are seen to have much higher portfolio carbon intensities compared to richer countries such as Liechtenstein and Monaco.

Figure 1 The carbon intensity of national equity portfolios and GDP per capita in 2017

Note: Carbon intensity as a measure of exposure to emissions is measured as tonne CO2e per thousand US dollars of revenues. GDP per capita is in thousands of US dollars.

Our empirical analysis confirms a negative relation between the carbon intensity of equity investments and economic development, as proxied by GDP per capita. Specifically, in our empirical work we relate the aggregate national ownership share for individual firms to, among other things, an interaction term of the firm-level carbon intensity and the log of investor-country GDP per capita. This interaction term is estimated with a negative coefficient, which suggests that a country’s tendency to avoid investments in relatively brown equities increases with its GDP per capita. The estimated effect is economically significant, as our estimation implies that an increase in a country’s (log) GDP per capita by one standard deviation increases its ownership share of a ‘green’ firm relative to a ‘brown’ firm by 2.9% (where the ‘green’ and ‘brown’ firms are taken to have carbon intensities that are one standard deviation apart). Our analysis suggests that economic development, which may come at a cost of additional pollution, could have a silver lining, as it can lead to a greening of the national equity portfolio. Internationally, our analysis can explain that richer countries hold greener equity portfolios.

The roles of investor type and firm characteristics

Investors differ in the rationales underlying their investments, and hence in their abilities to divest from any brown equities that they hold. Following our data source, we distinguish between ‘investment managers’ who make portfolio decisions on behalf of their clients and ‘strategic investors’ who maintain stakes in certain firms for strategic reasons. Investment managers in principle have the discretion to reduce their exposure to brown stocks, while strategic investors generally are less flexible. In line with this, we find that the ownership shares of relatively brown firms of investment managers, but not of strategic managers, decline with economic development.

Investor type is further revealed by an investor’s average portfolio turnover. Investors with high portfolio turnover, specifically, may be more interested in short-term trading profits than in the long-term implications of their investments for climate change. Consistent with this, we find that investors with higher portfolio turnovers have a lower tendency to green their portfolios at higher income levels.

The tendency of investors in richer countries to divest more from brown equities is found to depend on several firm characteristics. In particular, this proclivity is stronger for firms that belong to generally brown industries such as oil and gas, and metals and mining, which suggests that investors screen firms based on firm-level carbon intensity as well as on average industry-level carbon intensity (in line with evidence in Amel-Zadeh and Serafeim 2018). Furthermore, we find that investors in richer countries are more prone to reduce their investments in larger carbon-intensive firms, which could reflect the greater visibility of larger firms or the perception that larger firms have a greater impact on climate change (Azar et al. 2021). Finally, we find that investors in richer countries are less inclined to divest from browner stocks that are included in the MSCI World index. Probably this reflects the prominence of index investing, whereby investors forego the selection of individual stocks based on firm characteristics including carbon intensity. As an implication, the increasing popularity of index investing with investors in richer countries could inadvertently have slowed down portfolio greening in these countries.

Conclusion

Using global stock ownership data, we show that investors in richer countries tend to hold greener equities. This finding is consistent with the theory of the private provision of public goods, which predicts that wealthier individuals would contribute more to the supply of the public good of portfolio greening (Bergstrom et al. 1986).

By acting as backstop owners of brown equities, investors in poorer countries could limit any positive effect of the divestment of brown equities in richer countries on the green transition. In particular, the willingness of investors in poorer countries to purchase brown assets could limit the negative share price effect of any divestment of such equities by investors in richer countries, thereby reducing the incentive for polluting firms worldwide to become greener. Also, the higher ownership of brown equities by investors in poorer countries could slow down the green transition, if such investors are less able or willing to use voice (engagement) to prompt brown firms to reform.

Source : VOXeu

.jpg")

")

")

.jpeg")

")

")

")

")

")

")