There is growing interest globally in responsible investing, whereby institutional investors incorporate environmental, social, and governance (ESG) issues into their investment processes. For instance, the Global Sustainable Investment Alliance estimates that in 2020, assets amounting to $35 trillion were invested according to ESG principles, a figure that has almost tripled since 2012 (GSIA 2013, 2021). In the second LTI Report (Gibson Brandon and Krueger 2023), we explore a series of issues relating to the responsible equity and fixed-income investment choices of institutional investors.

For instance, we use data for a global sample of institutional investors consisting of both asset owners (e.g. pension funds, insurance companies) and investment managers (e.g. banks, asset management companies, hedge funds) to study what drives institutional investors’ ESG performance at the equity portfolio level. To quantify the ESG performance of an institutional investor, we calculate ESG performance measures at the equity portfolio level. Intuitively, our ESG performance measures capture the ESG characteristics of the average holding in an institutional investor’s stock portfolio.

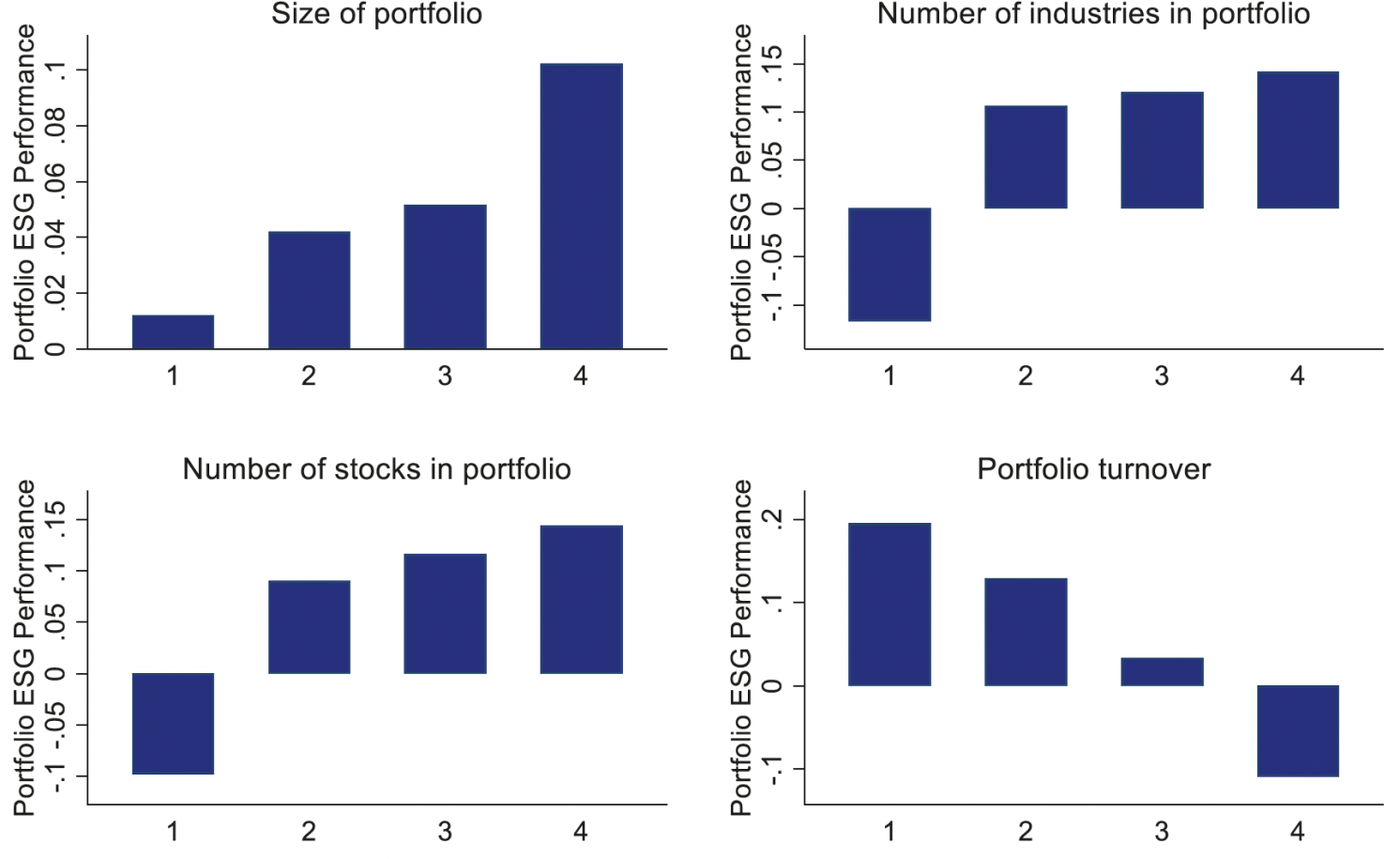

Figure 1 shows that larger institutions (in terms of assets under management, the number of stocks, or the number of invested industries) as well as more long-term oriented institutions (in terms of portfolio turnover) tend to exhibit better portfolio-level ESG performance.

Figure 1 ESG portfolio performance and institutional investor characteristics

The evidence of larger and more long-term oriented institutions exhibiting better ESG performance is consistent with the idea that ‘universal owners’ – i.e. large institutional investors who own a broad cross-section of the economy hold shares for the long term, and do not trade often (Hawley and Williams 2000) – tend to be more ESG oriented.

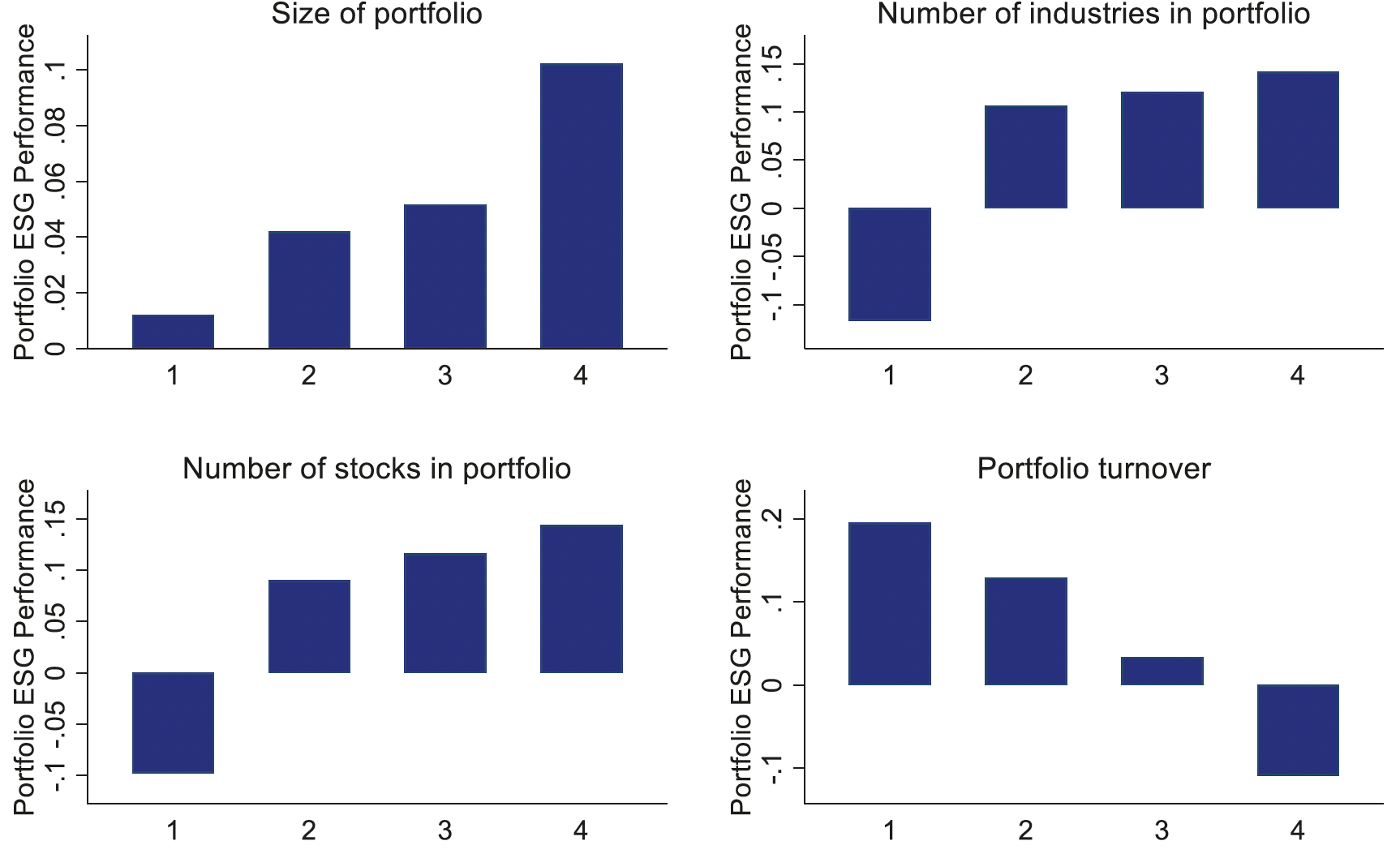

Another important driver of institutional investors’ responsible investment decisions is their geographic location. Dyck et al. (2019) highlight that societal norms and values regarding social and environmental issues are possibly important determinants of institutions’ responsible investment decisions. Hence, the LTI report also explores whether specific cultures, norms, and values of the institutional investors’ countries of location affect their responsible investment choices.

As Figure 2 shows, investors located in Europe tend to have better ESG portfolio performance than investors located in other parts of the world.

Figure 2 ESG portfolio performance by geographical area

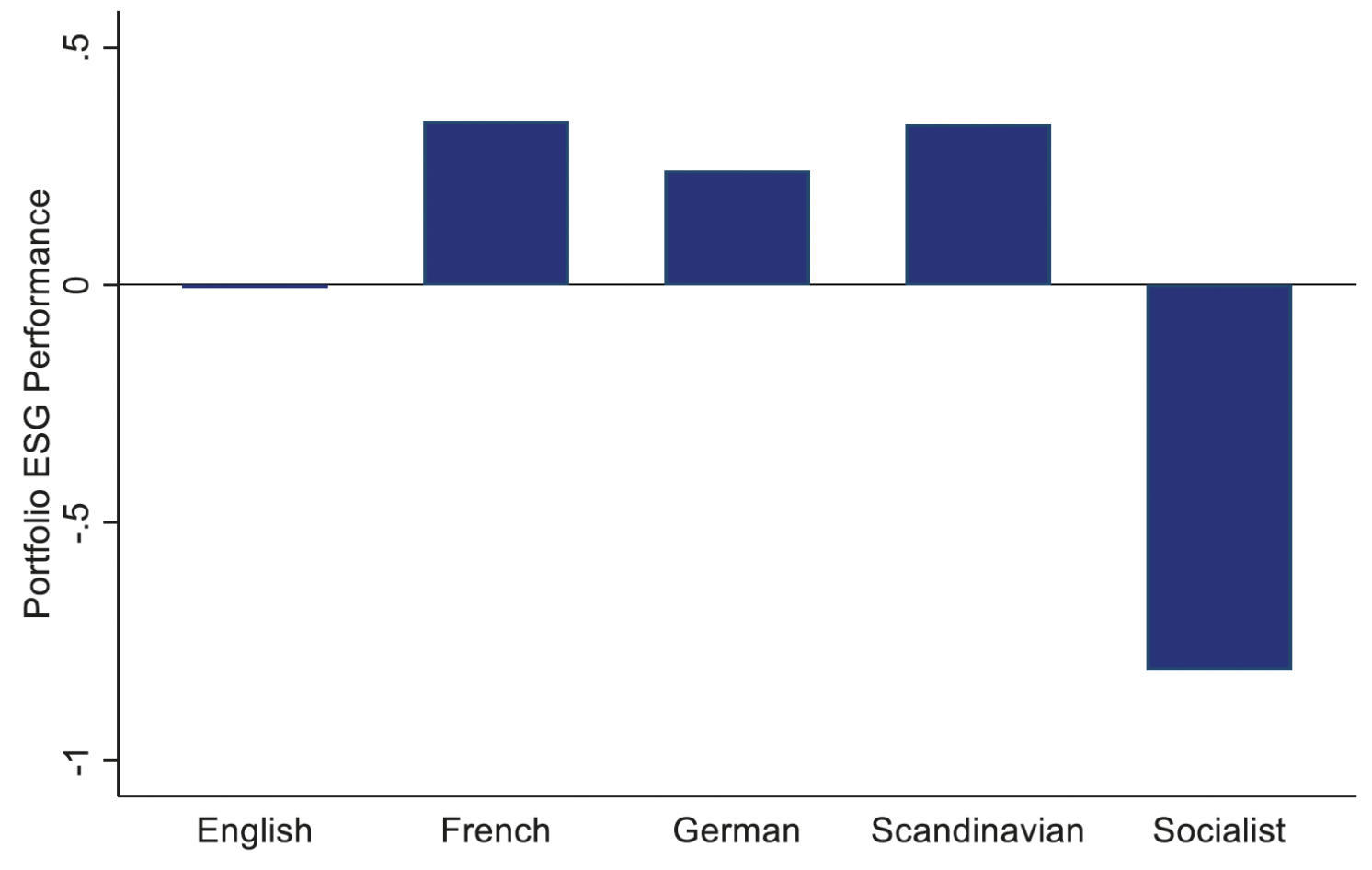

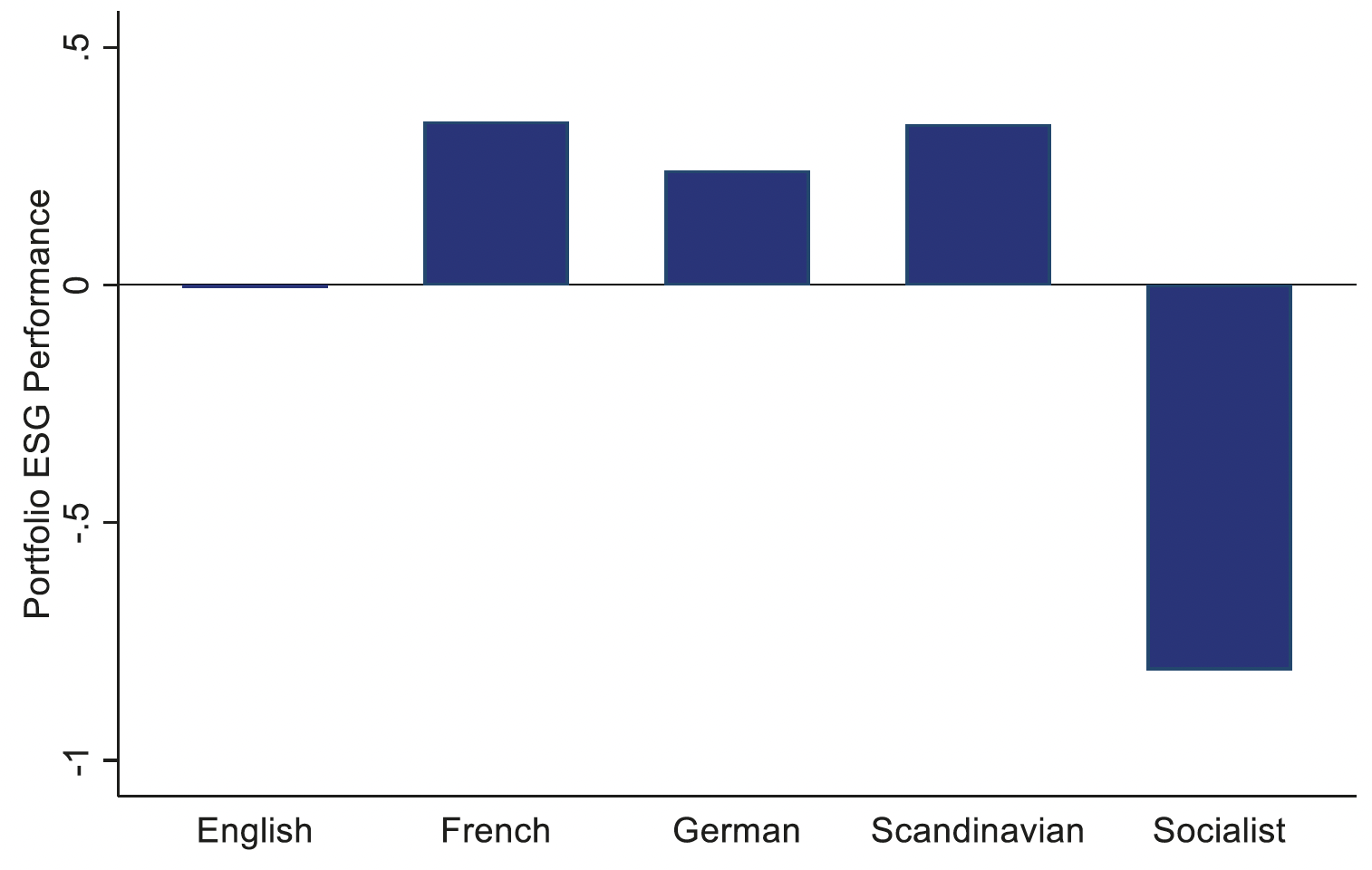

Another reason to believe that geographic variation plays a key role in explaining investor choices regarding responsible investing is related to the fact that legal traditions differ around the world and these legal traditions are likely to have a bearing on the extent to which institutional investors adopt responsible investing approaches. Using differences in legal traditions (or origins) to explain economic outcomes has a long tradition in economics and finance research (La Porta et al. 1998, 2008). In the report, we hypothesise that the legal origin of the country in which the investor is headquartered should also have a strong impact on the relative importance that investors attach to ESG issues. More specifically, civil law countries are known to have stronger concerns for labour issues and social protection (Botero et al. 2004). Common law countries, on the other hand, are generally regarded as emphasising investor protection, stronger protection of shareholder rights, and a stronger view of other governance issues (e.g. La Porta et al. 1998, Doidge et al., 2007). In other words, civil law countries are closer to being stakeholder oriented; thus, investors in these countries should be more inclined to follow a stakeholder approach (Allen et al. 2015, Magill et al. 2015) and care about ‘E’ and ‘S’ matters (see also Liang and Renneboog, 2017).

Figure 3 shows that investors from countries with civil law legal traditions (e.g., French, German, or Scandinavian) tend to have the best overall ESG performance. In contrast, investors located in countries with socialist legal origins tend to have the worst ESG portfolio performance. The figure also shows that, as expected, the overall ESG portfolio performance of investors located in common law countries is worse than that of investors located in civil law countries. Further analysis in the report demonstrates more subtle differences in terms of the individual portfolio-level E, S, and G performances.

Figure 3 ESG portfolio performance by legal origin of the institutional investor’s country of location

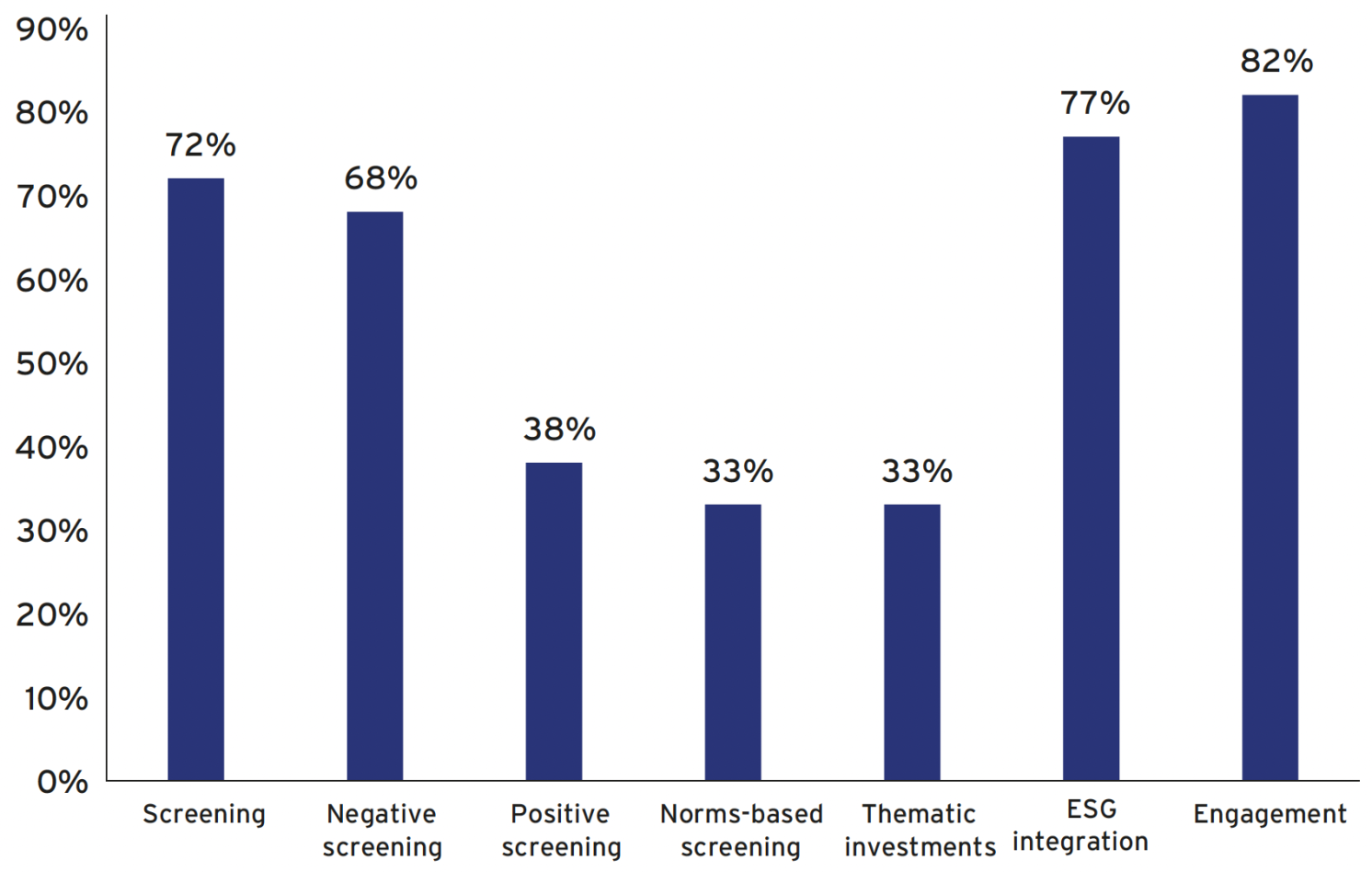

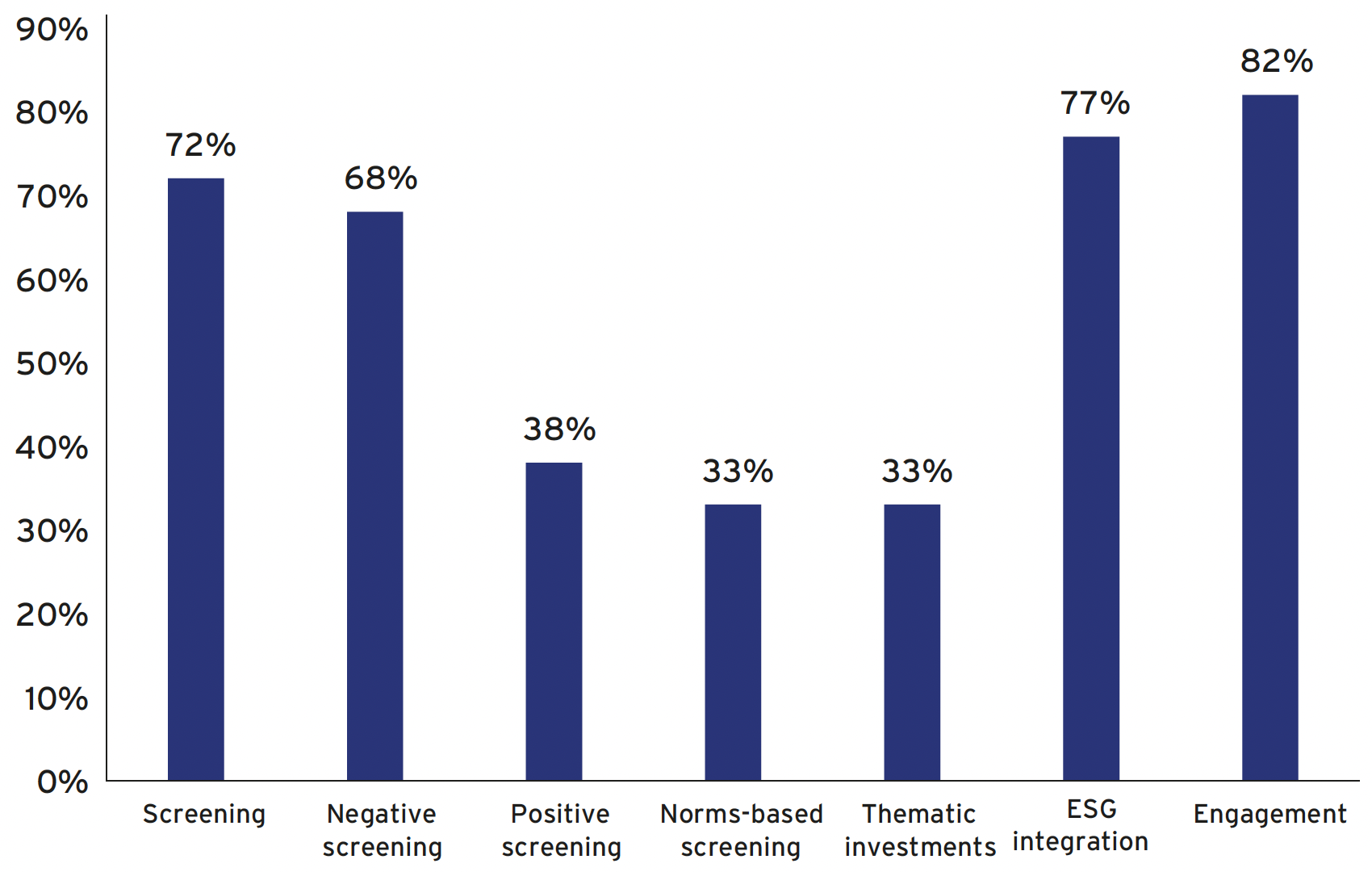

In the report, we also examine the extent to which institutional investors use specific responsible investment strategies. Typically, institutional investors use screening (positive, negative, or norms based), ESG integration, sustainability themed investing, and shareholder engagement to implement responsible investing in their equity investments. As Figure 4 shows, institutional investors predominantly use screening, engagement, and ESG integration, while sustainability-themed investments are still niche.

Figure 4 Usage of different responsible investment strategies

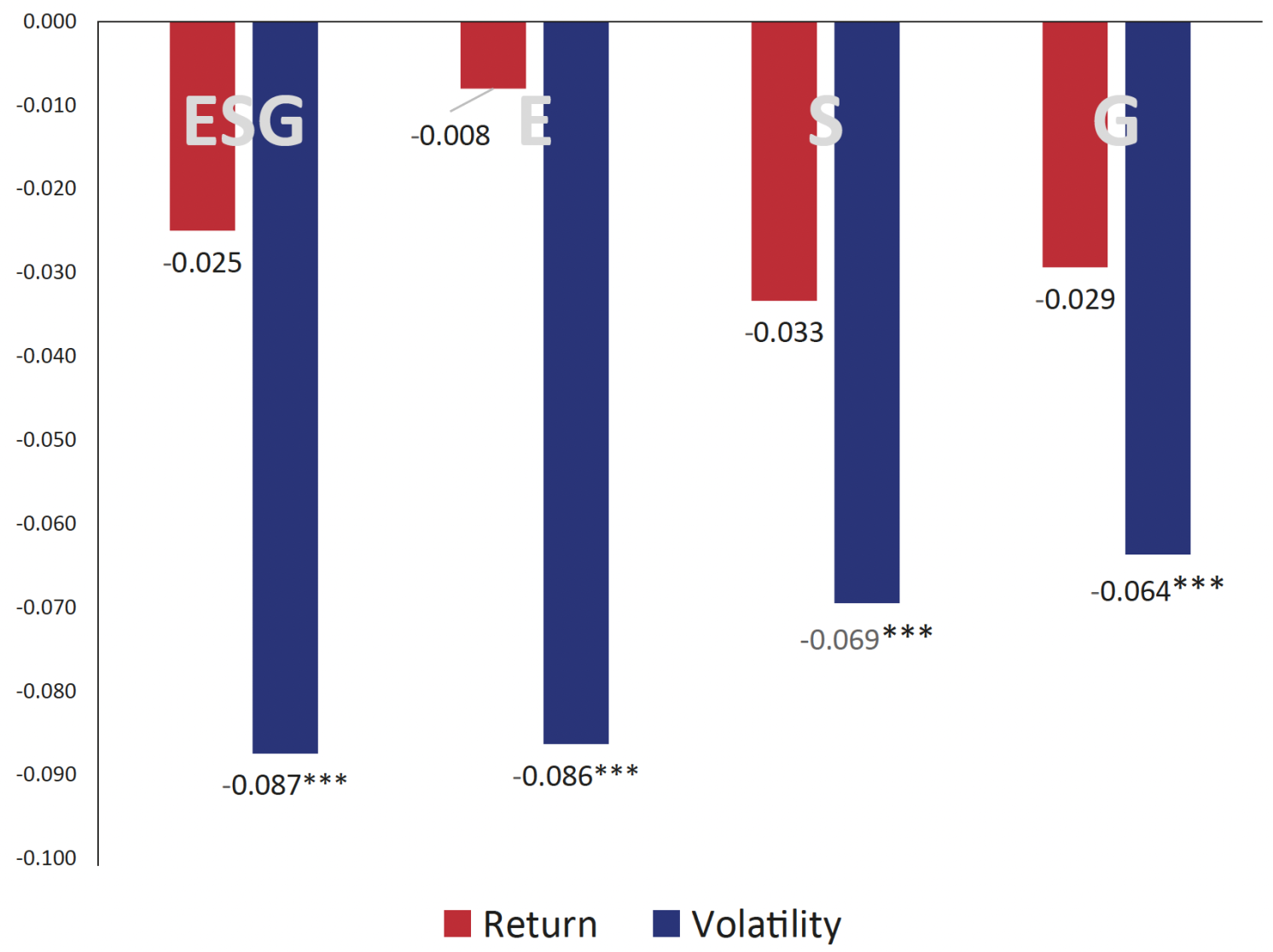

Shifting attention to the financial consequences of responsible investing, the report also examines whether the risk and return characteristics of institutional investors’ equity portfolios depend on the responsible investment choices of firms.

Figure 5 demonstrates that institutions with better ESG performance at the portfolio-level tend to have significantly lower portfolio risk, but the returns of their equity portfolios are not affected by their approach to ESG.

Figure 5 Standardised effects of ESG portfolio performance on portfolio return and risk

Relying on our own research and the emerging academic literature on greenwashing, we also discuss the important policy question of whether investors who promise to invest responsibly actually do so in practice and ‘walk the ESG talk’. We highlight important heterogeneity among institutional investors and greenwashing concerns being more pronounced in the US, a result that is also emphasised in Gibson Brandon et al. (2022).

The second part of the report focuses on sustainable fixed-income markets by examining a new class of sustainability-related fixed-income instrument: sustainability-linked bonds (SLBs). Unlike green bonds, proceeds from SLBs can be used for all sorts of expenses and investment projects and are not bound to finance only green projects. However, the main particularity of sustainability-linked bonds is that the coupon payment structure of these bonds depends on the achievement of a predefined sustainability target at a pre-specified date, and a penalty is typically added to the coupon if a target based on a measurable sustainability key performance indicator (KPI) is not met.

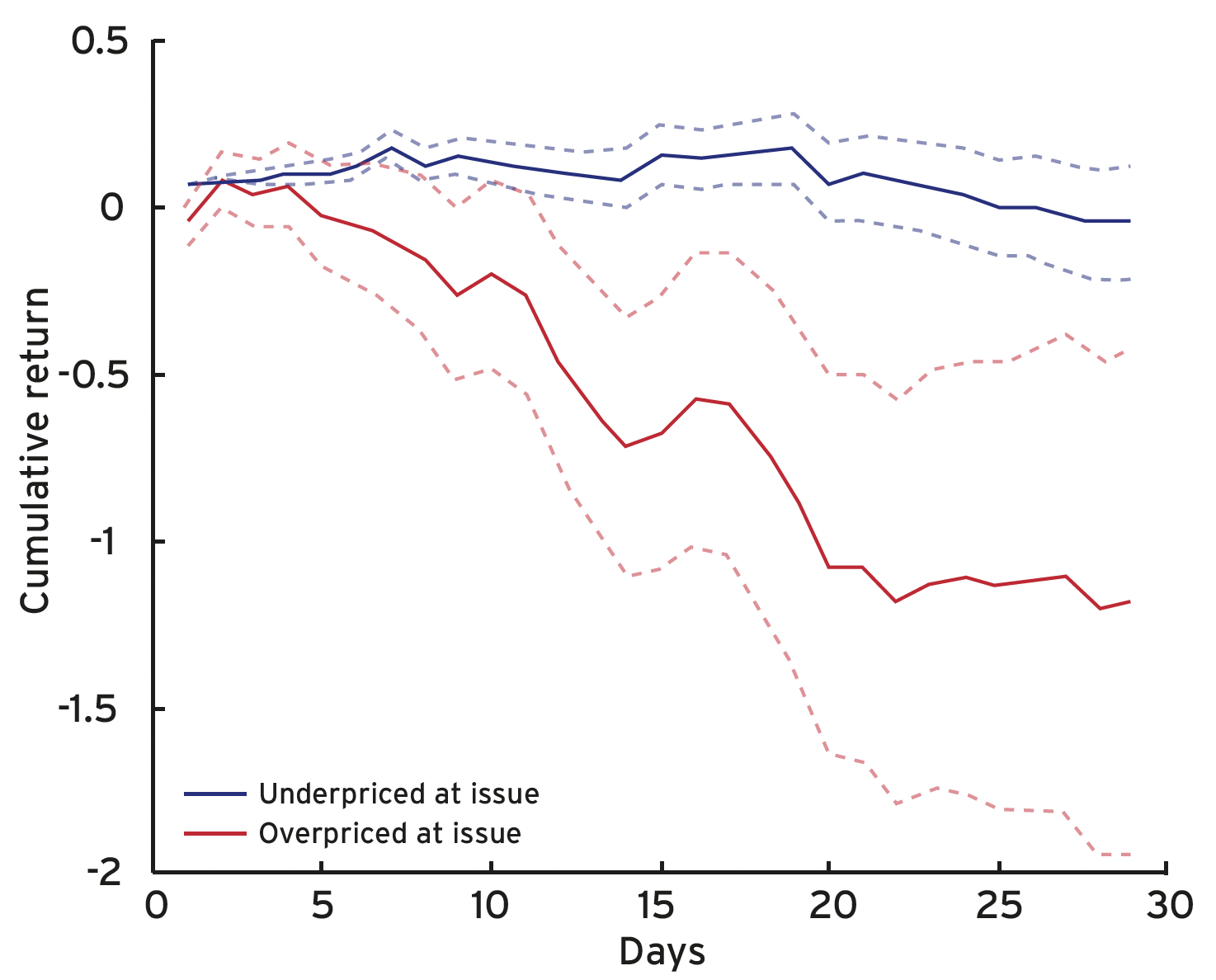

Using novel analysis and building on our existing research (Berrada et al. 2022), we document several empirical facts regarding SLBs. For instance, we demonstrate that SLBs are primarily issued in Europe by large, levered, and profitable firms. In addition, we ask the question of how well the market prices these instruments at issuance. To address this question, we rely on the SLBs mispricing measure developed in Berrada et al. (2022). This study documents that overpriced bonds represent about 20% of SLBs issued between 2018 and early 2022. Empirically, such overpricing leads to a post-issuance decrease in their prices on the secondary bond market (Figure 6). The secondary market performance difference between overpriced and underpriced bonds is about 1 percentage point during a 30-day horizon after issuance. In the figure below, the solid red (blue) line shows the 30-day post-issuance cumulative returns of overpriced (underpriced) SLBs.

Figure 6 SLBs post-issuance performance

Another empirical finding in Berrada et al. (2022) is that when firms issue overpriced and SLBs, a significant wealth transfer occurs from the bondholders to the shareholders of the issuing firms: stock prices react more positively when firms issue more overpriced, which are large relative to the market capitalisation of the issuing firm. A final and important practical implication of the analysis in Berrada et al. (2022) is that it allows for a comparison of the original market yield of each SLB at issuance with the standard industry-computed yield at issuance. This yield comparison suggests that the industry generally ‘overstates’ the yield discount on an SLB for the issuing firm because the industry-computed yield typically ignores the expected coupon penalty faced by these firms.

Going beyond Berrada et al. (2022), the LTI report additionally focuses on the ‘real effects’ of SLBs by examining if firms that have issued SLBs with an environmental KPI target significantly reduce their CO2 emissions (or CO2 emission intensities) in the year of issuance. We find that relative to control firms, ‘treated firms’ that have issued SLBs reduce their CO2 emissions intensities by approximately 11 to 14 percentage points more in the year of issuance. These effects seem sizeable, but we should bear in mind that they are estimated using only a small sample of SLBs, mainly because of limited data availability.

Source : VOXEu

")

")

.jpeg")

")

")

")

")

")

")