Disasters are mostly unexpected, but during recent decades the world has witnessed a rising incidence of disasters of various types, including armed conflicts, infectious diseases, and natural calamities. This rise is expected to continue in the future due to political and demographic developments, nature loss, and climate change. The third LTI Report studies how banks are affected by unexpected disasters and how banks can prepare once the occurrence of disasters becomes more routine and thus expected. The authors review the nascent theoretical and empirical literature in this area and present complementary empirical analyses at bank and country levels.

Various types of disasters have been occurring more frequently recently, and governments have strengthened their responses to them.

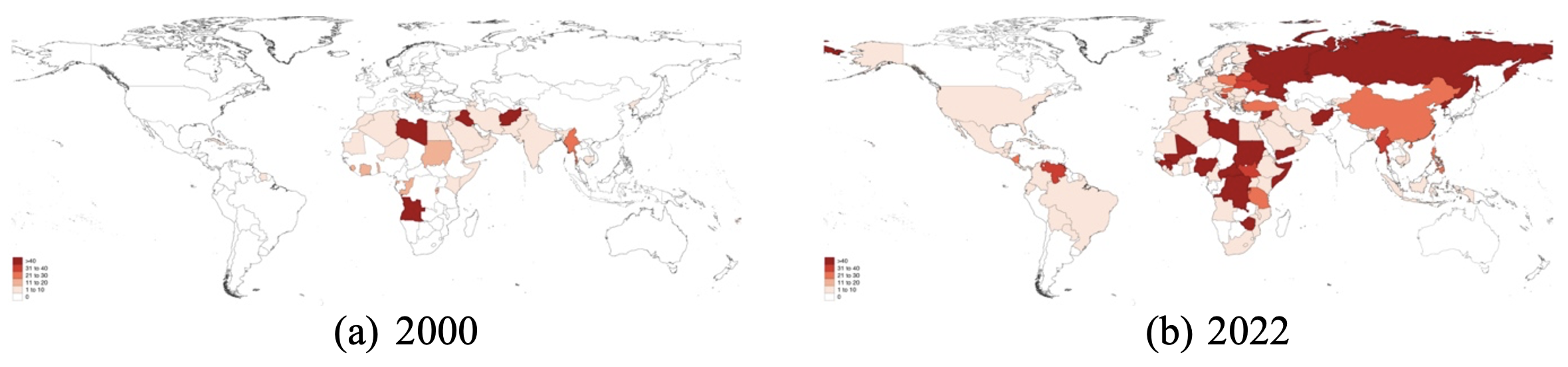

Armed conflicts, both domestic and international, may be ignited more often by failing states, demographic imbalances, and forced climate migration, and may have become potentially more damaging due to technological developments in armaments and targeting, and due to cyber capabilities. Two maps in Figure 1 illustrate the rise in conflicts worldwide and over time. Two recent striking examples include the Russia-Ukraine war launched in 2022 and the Hamas-Israel war in 2023. Figure 2 shows that countries launching wars are increasingly punished by economic sanctions imposed by the West (Felbermayr et al. 2020, Cipriani et al. 2023).

Infectious diseases, with cross-species viral transmission causing epidemics and pandemics, may increase and be more lethal due to weakening public health systems, ageing populations, and climate change (Carlson et al. 2022). The recent COVID-19 pandemic has had dramatic negative effects on economic performance and social cohesion (Chetty et al. 2023).

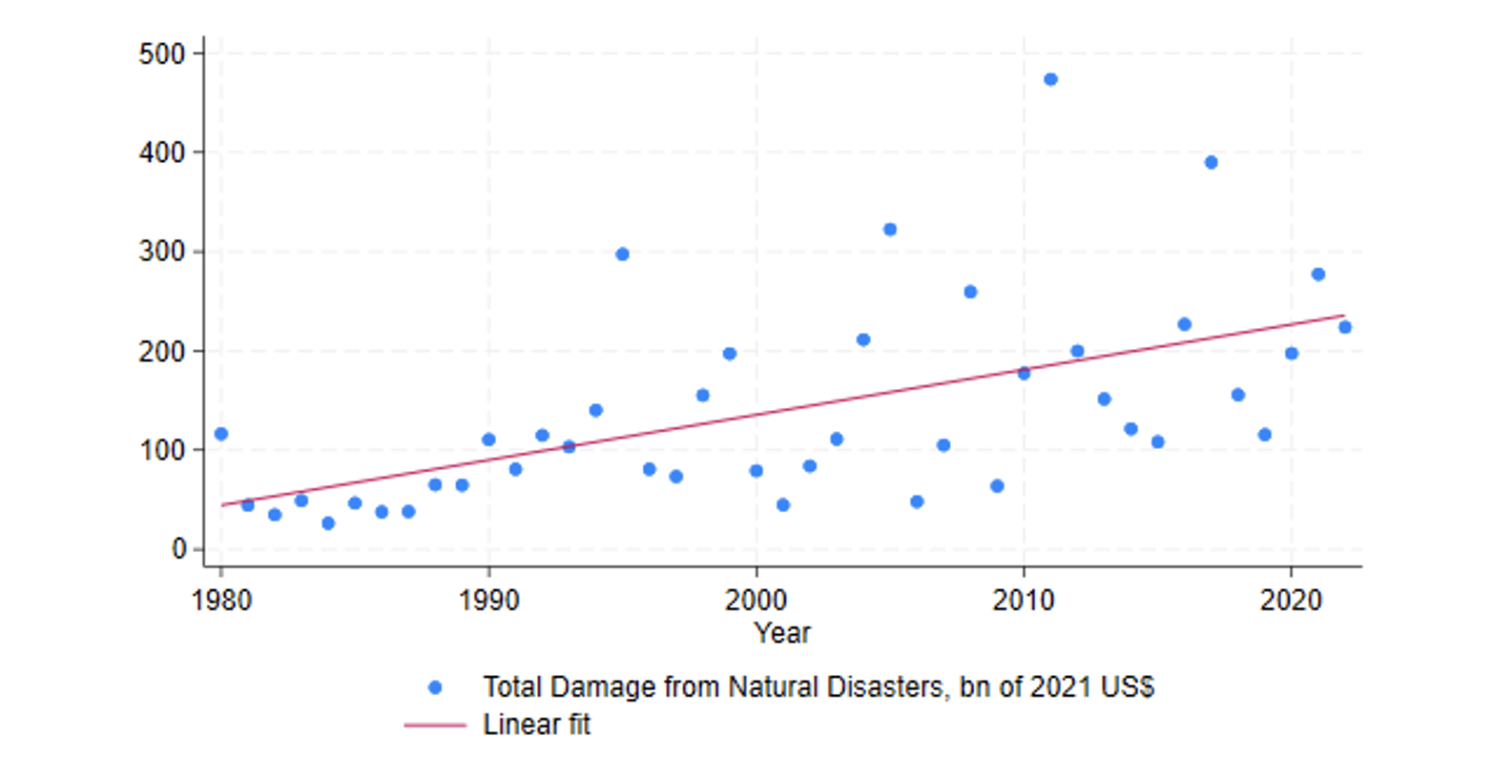

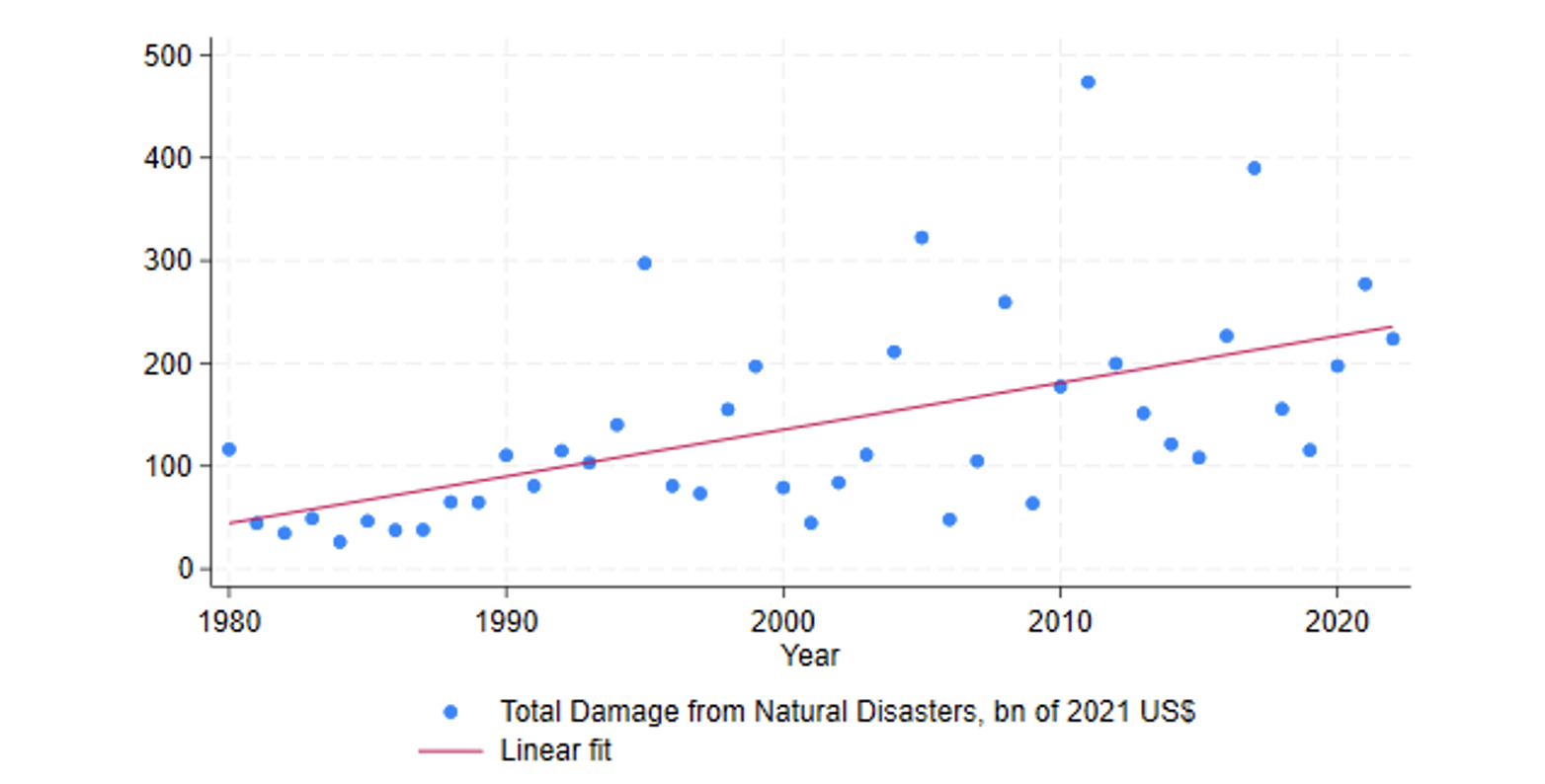

Finally, natural disasters, such as the hurricanes in Mexico in 2023 and in the US in 2022 and the drought in Brazil’s Amazon in 2023, may become more frequent due to climate change. Damages from earthquakes (such as in Morocco and Turkey in 2023) may have increased due to population density and systemic corruption. Total annual damage from natural disasters more than doubled over the last three decades (Figure 3).

Figure 1 Rising armed conflicts around the world

Source: Uppsala Conflict Data Program (UCDP).

Figure 2 Growing geographical spread of international sanctions

Source: The Global Sanctions Database (Felbermayr et al. 2020)

Figure 3 Total damage from natural disasters across the world (billions of 2021 US dollars)

Source: EM-DAT, the International Disasters Database

In the third LTI Report, an initiative of the Long-Term Investors (LTI@UniTO) think tank launched by the University of Torino and hosted by Collegio Carlo Alberto since 2017, we study how banks respond to unexpected disasters and how they adapt to predictable disasters (Mamonov et al. 2024)

CHAPTERS

The survey of existing research on finance and armed conflict presented in the Chapter 1 of the report yields several lessons. First, banks and their clients are affected by war and peace: war translates into higher loan rates; and when peace is restored, banks witness an increase in loan demand stemming from a higher willingness to invest. Second, civil unrest activates loan officers’ taste-based discrimination, which results in price discrimination of loan applicants based on non-economic (e.g. religious, national) characteristics. This implies that the emotional state of loan officers plays an important role in their credit decision-making. Third, banks are affected by international sanctions by the opportunity to place new debts in the financial markets of sanction-imposing countries being cut off and the risk of their foreign assets being frozen. However, the severe effects of sanctions are usually mitigated through the following three channels: financial support from the sanctioned government; evasion of the international restrictions with the help of banks from non-sanctioning countries (e.g. China), and sometimes the banks from sanctioning countries as well (e.g. Germany); and the staggered implementation of the global sanction policy. Under staggered implementation, the first sanction announcement has strong negative effects on the sanctioned banks but also causes strong anticipatory effects on those not-yet-sanctioned banks, leaving some time for them to adapt both their international and domestic operations in the most favourable way.

In the novel bank-level quantitative analysis presented in the report, we focus on spillovers of international financial sanctions imposed on Russia to formally non-targeted banks (i.e. subsidiaries of foreign financial institutions operating in the sanctioned country). These spillovers are likely to arise because of the home-based pressure on foreign banks (from both the regulatory and customer sides) and potentially deteriorating domestic macroeconomic conditions forcing the banks to exit. We study sanctions against Russia which were implemented in a staggered fashion between 2014 and 2019 to analyse the adaptation of both politically connected and foreign banks in Russia. We show that the first sanction announcement forced not only politically connected banks to adapt their international exposures, as has recently been established in our previous work (Ongena and Mamonov 2021), but also subsidiaries of foreign banks. Sanctions against major domestic government-connected banks spilled over to foreign banks in Russia, which reduced the overall inflow of funds from abroad by 6.6% in 2014 and by 15.9% during 2014–2016.

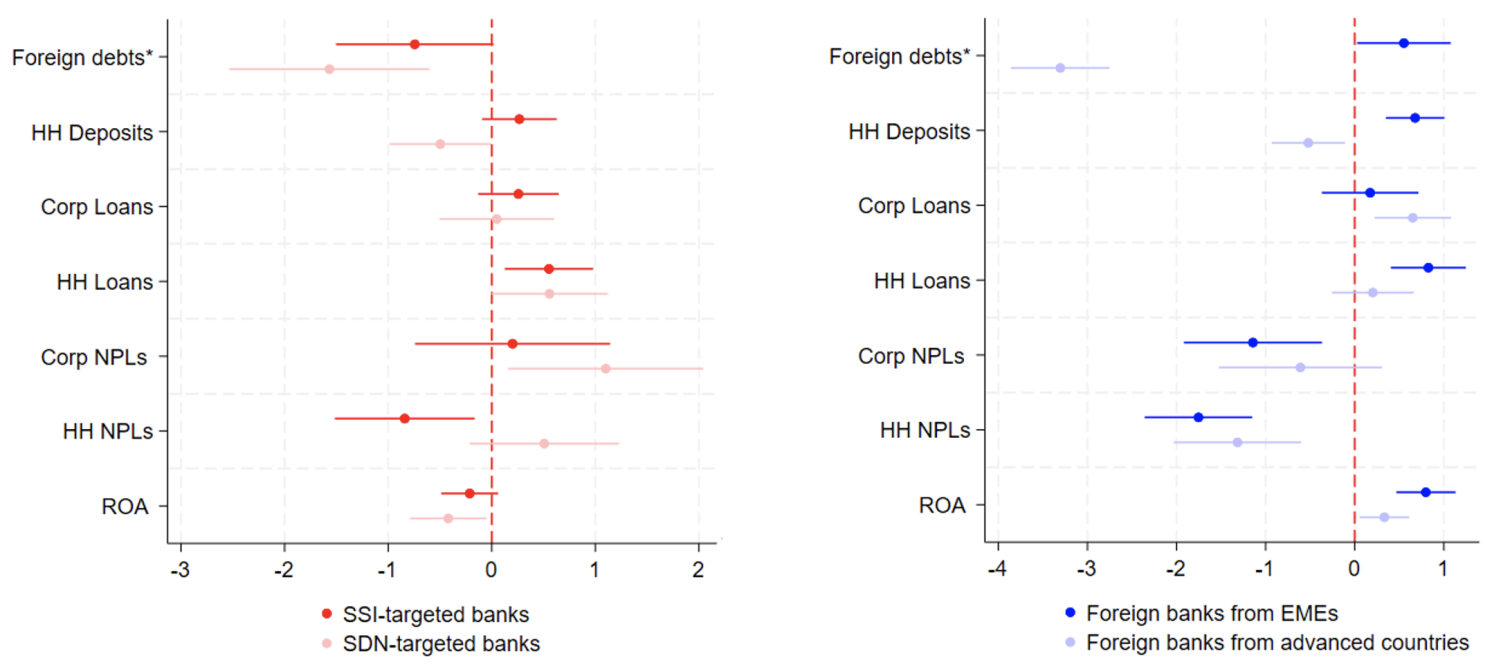

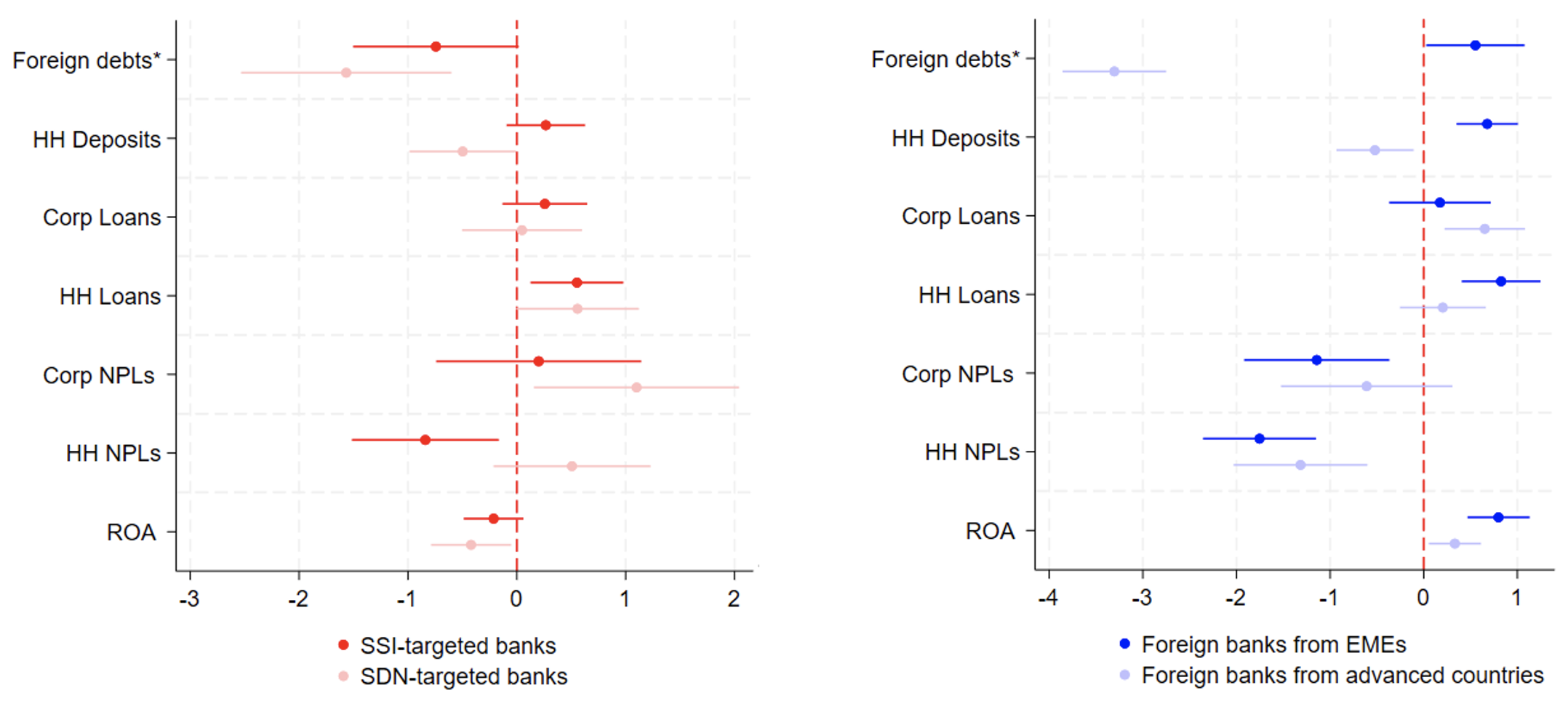

Our analysis reveals substantial heterogeneity in the spillover effects of anti-Russian sanctions on foreign banks in Russia. First, in line with the findings from the previous literature that political partisanship matters for the cross-border flows of capital, our estimation demonstrates that foreign banks originating from the West (UniCredit, City, Société Générale, Raiffeisen, etc.) reduced their foreign liabilities in Russia (i.e. the inflow of funds to Russia from abroad) by over 30% in the three years after the first sanctions. Conversely, subsidiaries of foreign banks from the East (mainly Turkey, India, and China) increased their foreign liabilities in Russia by 5.5% over the same period (Figure 4, foreign debts). Despite shrinking foreign liabilities, Western foreign banks did not cut domestic operations, with one possible reason, according to our analysis, being the opportunity for profit (Figure 4, positive effect on ROA for foreign banks). This sheds light on why foreign business may be hesitant to withdraw from sanctioned countries.

Figure 4 Treatment and spillover effects of sanctions on Russian banks

Notes: The figure presents the difference-in-differences estimates of the effects of the first sanction announcement against Russian banks that occurred in March 2014. Dependent variables are along the Y axis: log of foreign borrowings, one-month log-difference of the following variables: household deposits (HH Deposits), corporate loans, household loans, non-performing corporate loans, non-performing household loans, and annualized return on assets (ROA). All variables are in percent of total bank assets, except foreign debts. * For comparability of the estimates across dependent variables, the coefficient on foreign debts variable is multiplied by 10. Key explanatory variables: treatment and spillover binary indicators after the first sanction announcement. Both groups are divided into two sub-groups: treatment — into SSI-targeted banks (red) and SDN-targeted banks (pink); spillover — into foreign banks originating from EMEs (blue) and foreign banks originating from advanced countries (pale blue). The effects are measured over a 36-month period. The control group is domestic private banks.

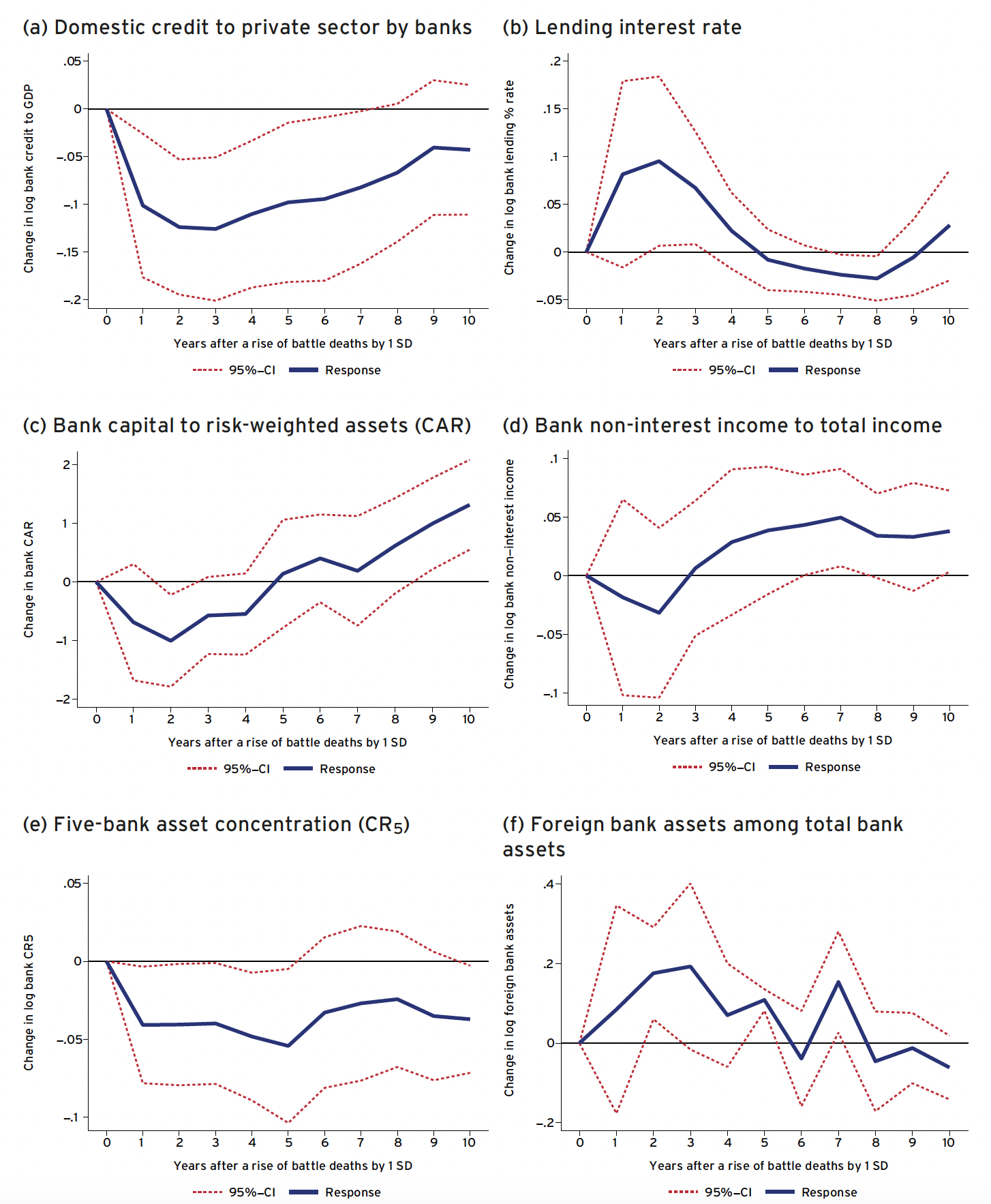

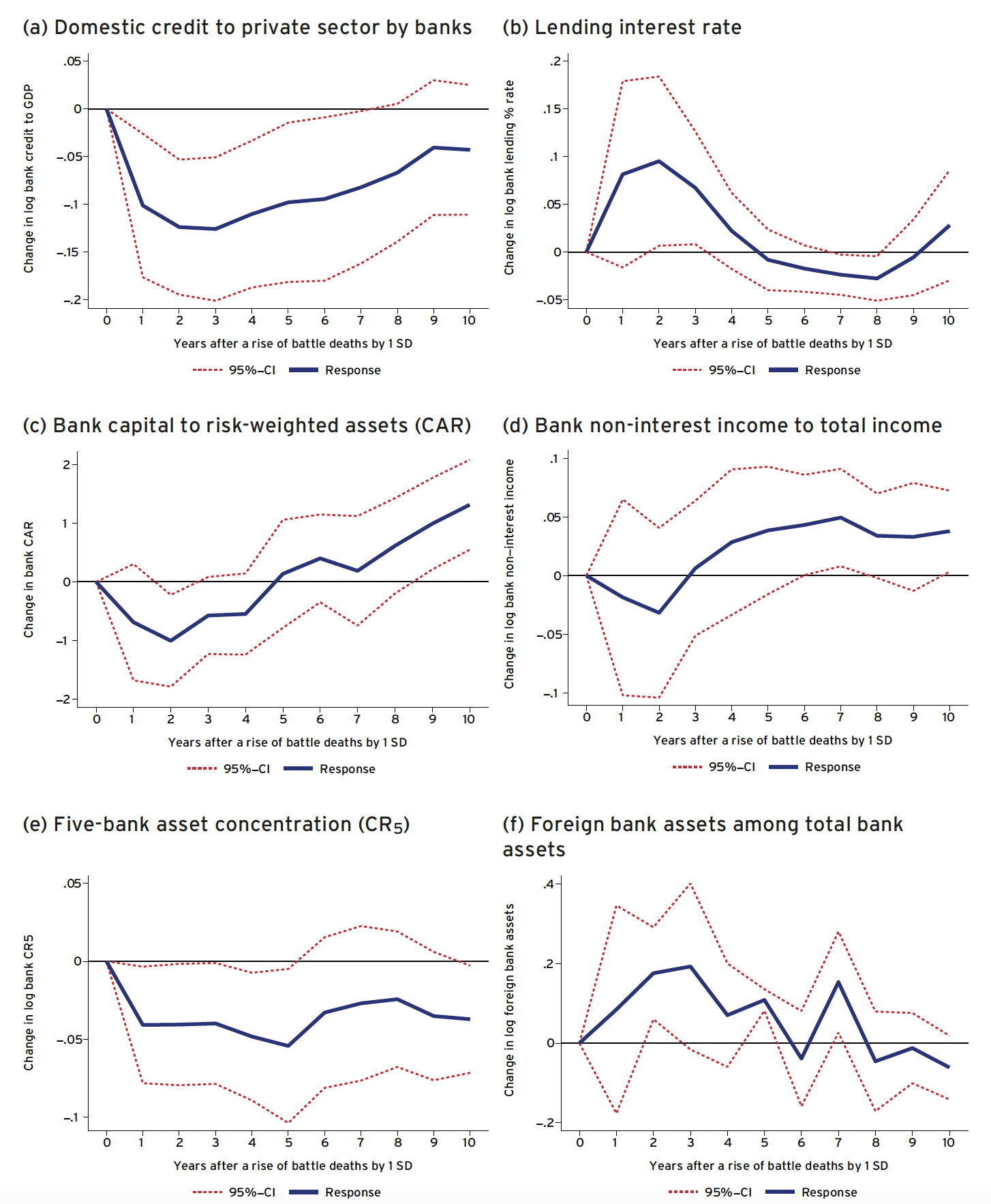

Our cross-country analysis of armed conflicts and banking shows that, on top of negative macroeconomic supply shocks, as shown in previous research (Koczan and Chupilkin 2022, Federle et al.. 2024), wars appear as negative credit supply shocks: they reduce lending and increase lending rates. Credit-to-GDP falls by up to 12%, with the effect dying out only after seven years, and interest rates spike by up to 10% of the initial price of loan, with the significant increase in 2-3 years from the onset of conflict (Figure 4). The capital adequacy ratio (CAR) declines in the first 1-2 years after a war, suggesting that bank owners may withdraw or lose their funds. Over time, however, the CAR tends to rebound, likely reflecting post-crisis economic recoveries. Wars reduce bank concentration in countries affected by conflicts. Foreign banks, however, tend to increase their presence in war-affected regions as time passes, potentially capitalising on reduced concentration and post-war economic recovery. The impact of wars on bank credit varies substantially across countries. In the report, we show that tighter fiscal and monetary policy, along with excessively volatile stock markets, exacerbate the negative effects of wars on banking. However, a greater ability to attract foreign loans and rising world prices of the affected countries’ exports substantially mitigate the adverse economic effects of wars.

Figure 5 The effects of armed conflict on banking

Note: These charts report the responses of banking system indicators to a one standard deviation increase in log battle deaths in year 0 (relative to population) estimated using local projections. Sample: 781 observations for 87 countries ever experienced battle deaths of their civilians over the period 1989-2019. Standard errors are double-clustered: at country and year levels to account for rising autocorrelation at larger prediction horizons.

In Chapter 2 of the report, we study bank adaptation to infectious diseases, focusing primarily on the literature devoted to the COVID-19 pandemic. We survey existing research and document the effects of the pandemic on bank lending, profitability, and the structure of bank operations. During the COVID-19 pandemic, banks increased their markups yet faced deterioration of their performance and shifted towards government-supported lending. The pandemic facilitated a major transformation of banking, accelerating the shift away from in-person interactions to online and mobile transactions, and gave an advantage to fintech lenders. The spread of infectious diseases accelerates the use of mobile transactions and technology in banking and increases inequality along several dimensions.

Our cross-country regression analysis shows that infectious diseases exert a dampening effect on the demand for loans. Both the volume of bank loans and the interest rates on loans tend to decrease as infectious diseases spread. This contrasts with the impact of wars, which primarily affect the supply of loans. Furthermore, our results demonstrate that infectious diseases may be associated with an increase in banks’ capital adequacy ratios. This phenomenon is likely driven by banks reducing loans to riskier borrowers while maintaining their capital levels. As loans shrink, banks also tend to rely more on non-interest income sources as a response to the spread of infectious diseases. In addition, we observe a trend towards greater bank concentration, suggesting that larger banks could be more resilient to the effects of infectious diseases than their smaller counterparts. This resilience may stem from larger banks’ capacity to reorient their operations from regions more heavily affected by disease to those less affected, either within a single country or across multiple countries.

In Chapter 3 of the report, we review the literature on how banks adapt to natural disasters. Bank performance is negatively impacted by natural disasters, though the effect is short-lived lived and far from catastrophic even in the case of most destructive disasters (such as Hurricane Katrina). Non-native banks are more likely to leave markets affected by natural disaster. There is an increased credit demand in the areas affected by natural disasters, but banks redirect funds across geographies with multiple frictions. Bank-borrower relationships, as well as geographically diversified connections, help sustain access to finance, while low bank capitalisation amplifies local natural disaster shocks. Banks price anticipated disaster risk: they charge higher interest rates for mortgages on properties exposed to a greater risk of sea level rise. Mortgage lenders transfer climate-related default risk through securitisation in the aftermath of natural disasters, which eventually helps sustain credit supply in disaster zones.

Our cross-country analysis does not find significant negative effects of adverse environmental events on bank credit to the economy, which is consistent with short-lived losses and multiple frictions during the recovery previously found in the literature. Additionally, we conjecture that the lack of identified country-level effects of natural disasters on banking may stem from its predominantly local nature.

Overall, we conclude that disasters negatively affect banking though banks price an anticipated disaster risk and transfer it, if possible. In the foreseeable future, banks may have to respond more actively than ever to such disasters given that political and demographic developments and climate change may put banks in ‘triple jeopardy’. Banks’ responses will likely consist of a combination of balance sheet strength, technological developments, and personnel skills and training.

Source : VOXeu

.jpg")

")

")

.jpeg")

")

")

")

")

")

")