Most studies on central bank digital currencies focus on the effects after they become well established. This column analyses the macroeconomic effects in the transition to the new equilibrium. Using a two-country model with financial frictions, it shows that, under plausible assumptions for demand for central bank digital currency, the transition is characterised by volatility in the digital currency, cash, and deposits, leading to volatility in loan rates, investment, and consumption. Binding caps on holdings of the digital currency during the transition period are shown to be most effective in reducing disintermediation and output losses and in minimising international spillovers.

A large academic literature – summarised in Ferrari Minesso et al. (2021), Niepelt (2021), and Panetta et al. (2022) – has developed and examined various potential effects of central bank digital currencies (CBDCs) on banks, the financial sector more broadly, and the rest of the economy, as well as on international spillovers. These papers have studied how shocks propagate differently through the economy once CBDCs are available, that is, around the new equilibrium with CBDC well established as a monetary instrument.

In a recent study (Assenmacher et al. 2024), we look at the issue from a different angle. We study the macroeconomic effects of CBDC in the transition to the new equilibrium – that is from the moment of initial launch up to the longer run before the CBDC is well established as a monetary instrument. We pay particular attention to policies that can help balance trade-offs in the transition phase. On the one hand, risks to macroeconomic and financial stability from excess demand for CBDC can arise. On the other hand, welfare losses may materialise when CBDC demand is overly constrained and the resulting menu of monetary instruments available to households overly reduced.

We develop a two-country model with financial frictions to study the transition from a steady-state without CBDC to one in which the home country issues a CBDC. There are two symmetric economies (home and foreign), which trade goods and financial assets under incomplete financial markets. In each country, consumers supply labour to firms, save, and consume final aggregate goods. They also need liquid assets to purchase final goods and can invest in three financial assets: bonds, deposits, and money, which in our setup means cash. Money can be used for payment, is not remunerated, and is subject to linearly increasing storage costs. Bonds, which are the only asset traded internationally, are remunerated but cannot be used for payment. Deposits are remunerated and can be used for payment, though they may not provide the same liquidity services as cash. Put differently, households have specific preferences over payment instruments, which are imperfect substitutes. Importantly, banks hold market power in the deposit market (see Drechsler et al. 2017, Andolfatto 2021). They can extract a surplus from deposit contracts, i.e. utility that households derive from liquidity services provided by deposits. As a result, deposits are remunerated below their marginal return for banks and the risk-free rate. Households accept such a contract in equilibrium because deposits provide valuable liquidity services.

The financial sector is populated by finitely lived banks that combine net worth and deposits to finance loans to firms. We assume that there is a financial friction like the ‘financial accelerator’ mechanism of Bernanke et al. (1999), which implies that bank credit plays a key role in firms’ financing. This mechanism also introduces frictions in the credit market, which only slowly adjusts to shocks. The economy’s production sector is populated by three different types of firms: capital good producers, intermediate good producers, and retailers.

Importantly, we assume that – in addition to cash – the home country can issue a central bank digital currency (CBDC). The CBDC is a liability of the central bank that is directly accessible to households and can be used for payment. Moreover, the CBDC can be traded across countries subject to certain limits. In the baseline configuration, it is not remunerated. It is a digital payment instrument – a digital version of a banknote – and is not subject to storage costs, unlike cash. CBDC provides variety to the menu of monetary instruments available, which households value – their marginal utility decreases in the amount of each instrument held. Moreover, as CBDC adds an alternative payment instrument, households’ budget constraints become less binding, thereby lowering the rents banks can extract from deposits. In the absence of adjustment of the terms of deposit contracts by banks, deposits would flow out from the banking system, resulting in bank disintermediation.

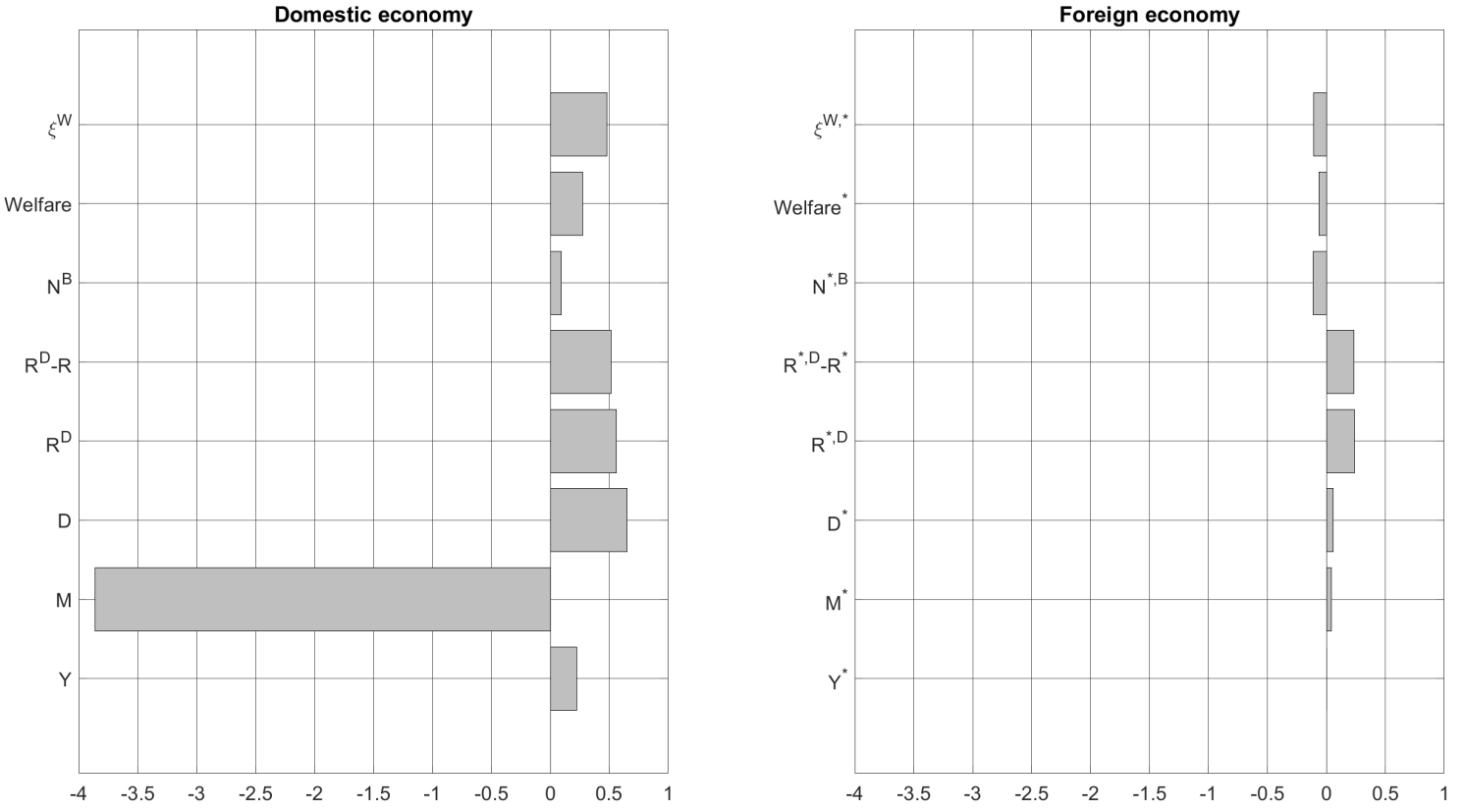

Figure 1 Percentage changes between the stochastic steady states without and with central bank digital currency

Note: The bars except ξW show percentage changes between the stochastic steady states of the model without CBDC and with CBDC. We consider the stochastic steady state to factor in the impact of uncertainty and thereby solve the model at the second order with pruning. ξW is a measure of the welfare-consumption equivalent, i.e. the change in consumption needed to make consumers in the baseline model indifferent to the introduction of the CBDC. The CBDC is issued in the home country, and, in this exercise, there are no restrictions in place to limit demand for CBDC.

We compare the equilibria with and without the CBDC using calibration values from Ferrari Minesso et al. (2022). The simulations are in Figure 1. In the new equilibrium, CBDC substitutes cash (M). Deposit rates (RD) and deposits (D) increase. The introduction of a CBDC is essentially a cost push shock on an input for banks, which now extract lower rents due to an increase in varieties of payment instruments. Accordingly, the deposit supply function shifts to the left and at the same time flattens (in an interest-rate/quantity chart). Therefore, although banks face higher costs, they also face a more elastic deposit supply, which reduces their market power. In the new equilibrium, banks find it optimal to pay a higher interest rate on deposits to maximise profits, even above the level needed to maintain deposit supply stable. This increases the convenience of deposits. Households thus have incentives to increase their deposit holdings at the margin, hence substituting only cash with CBDC. Moreover, output (Y) increases marginally in the new equilibrium. Welfare, measured as welfare gains in terms of steady-state consumption (ξW), improves at home and abroad because of the CBDC’s appeal in terms of convenience, absence of storage costs (relative to cash), and reductions in banks’ market power. The effects for the foreign economy are smaller.

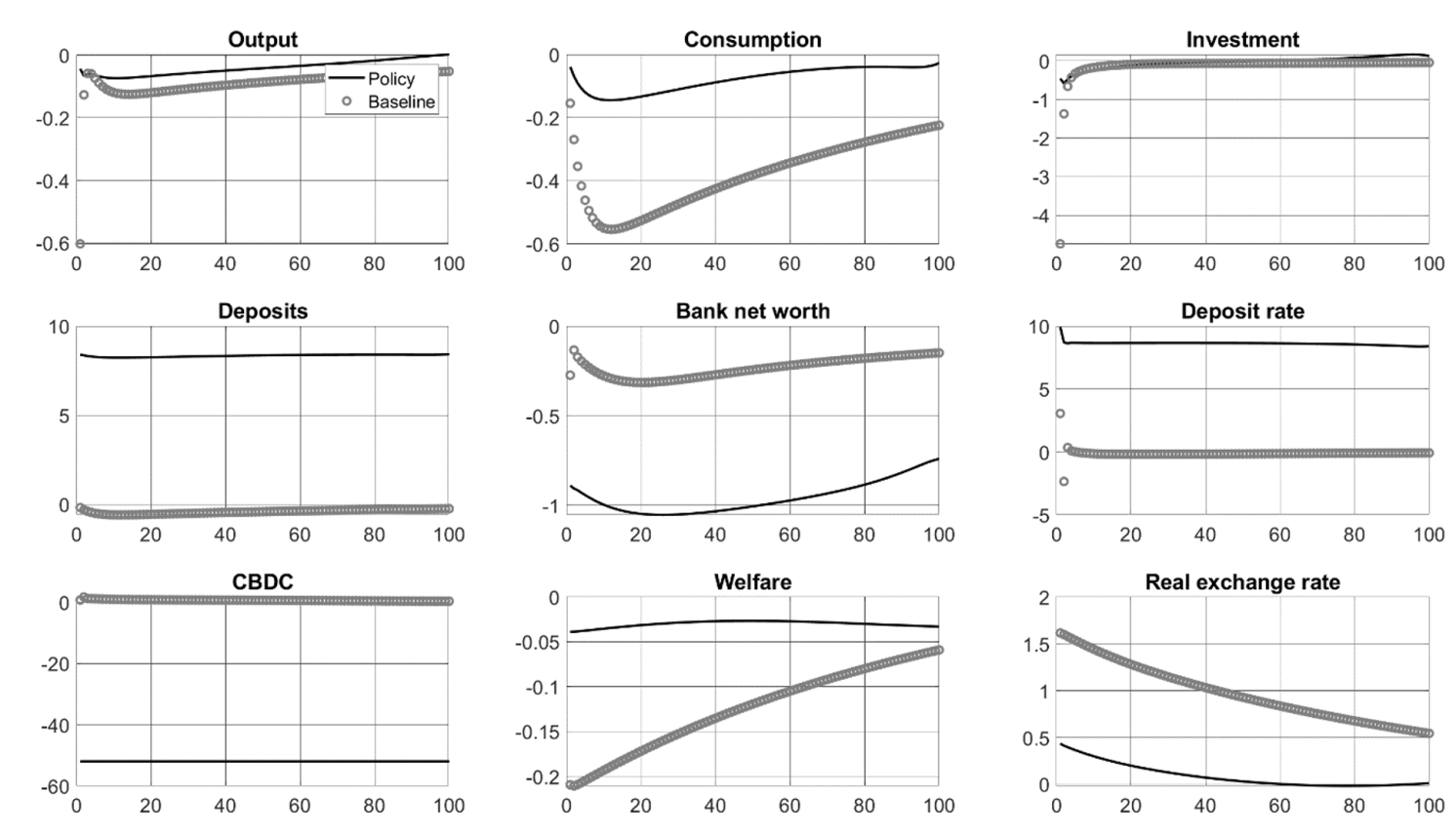

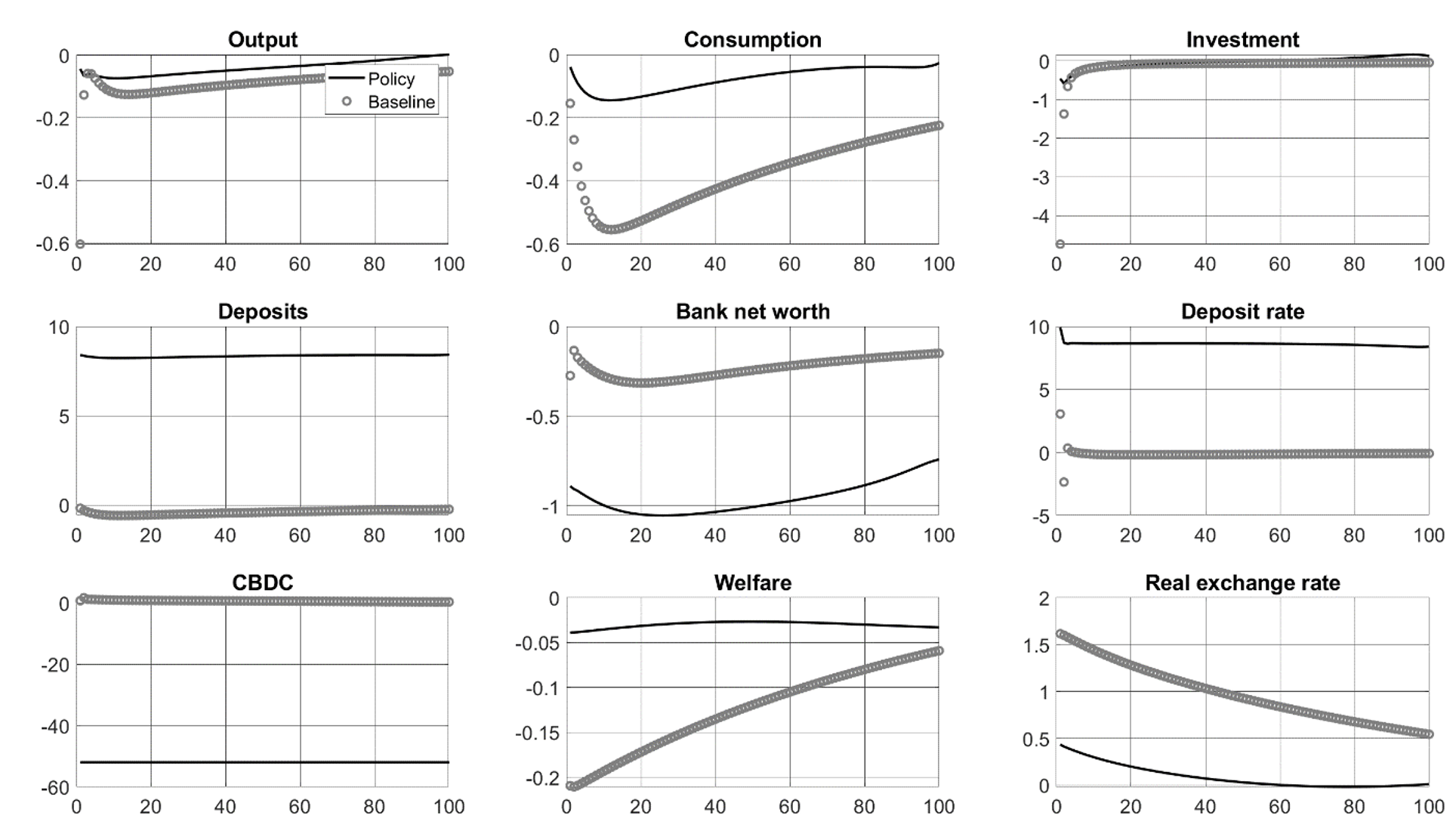

Next, we solve the model non-linearly to study the transition between the steady states with and without a CBDC. Transition takes time because there are frictions both in the real economy (i.e. price rigidity, monopolistic competition) and on financial markets (financial frictions). As a result, the economy does not adjust immediately to the new steady state, leading to welfare losses during the transition to the new equilibrium. During the transition, for example, credit is disrupted in the initial periods as banks take time to adjust to the new equilibrium. Since bank net worth accumulates gradually from bank profits, adjustment of the deposit rate is slow compared to a frictionless environment and deposits become relatively less attractive to households until the new equilibrium is reached.

Figure 2 Unconstrained transition to new equilibrium with central bank digital currency and transition under a holding limit calibrated to 50% of steady-state demand for CBDC

Note: Variables are reported in percentage deviations from the steady state with CBDC. The black line shows the transition in the home economy under the occasionally binding constraint and the grey dots the unconstrained transition path. The model is solved with global methods. Under the constrained simulation, the CBDC is issued in the home economy and, during the transition period, supply of CBDC is constrained to 50% of the steady-state demand for CBDC. The limit is gradually lifted back to the level of steady-state CBDC demand after period 100.

For low steady-state CBDC demand (i.e. 5% of quarterly steady-state output in our simulations), introducing a CBDC has no material macroeconomic impacts. For plausibly higher steady-state demand (i.e. 30% of quarterly steady-state output in our simulations) the transition to the new steady state is characterised by significant volatility in CBDC, cash, and deposits, leading to volatility in loan rates, investment, and consumption, as the grey dots in Figure 2 show. Demand for CBDC and cash overshoot their new equilibria in the short run, thereby crowding out bank deposits and leading to a fall in investment and consumption. Output declines initially and, after the initial volatility has subsided, increases slowly towards the new equilibrium.

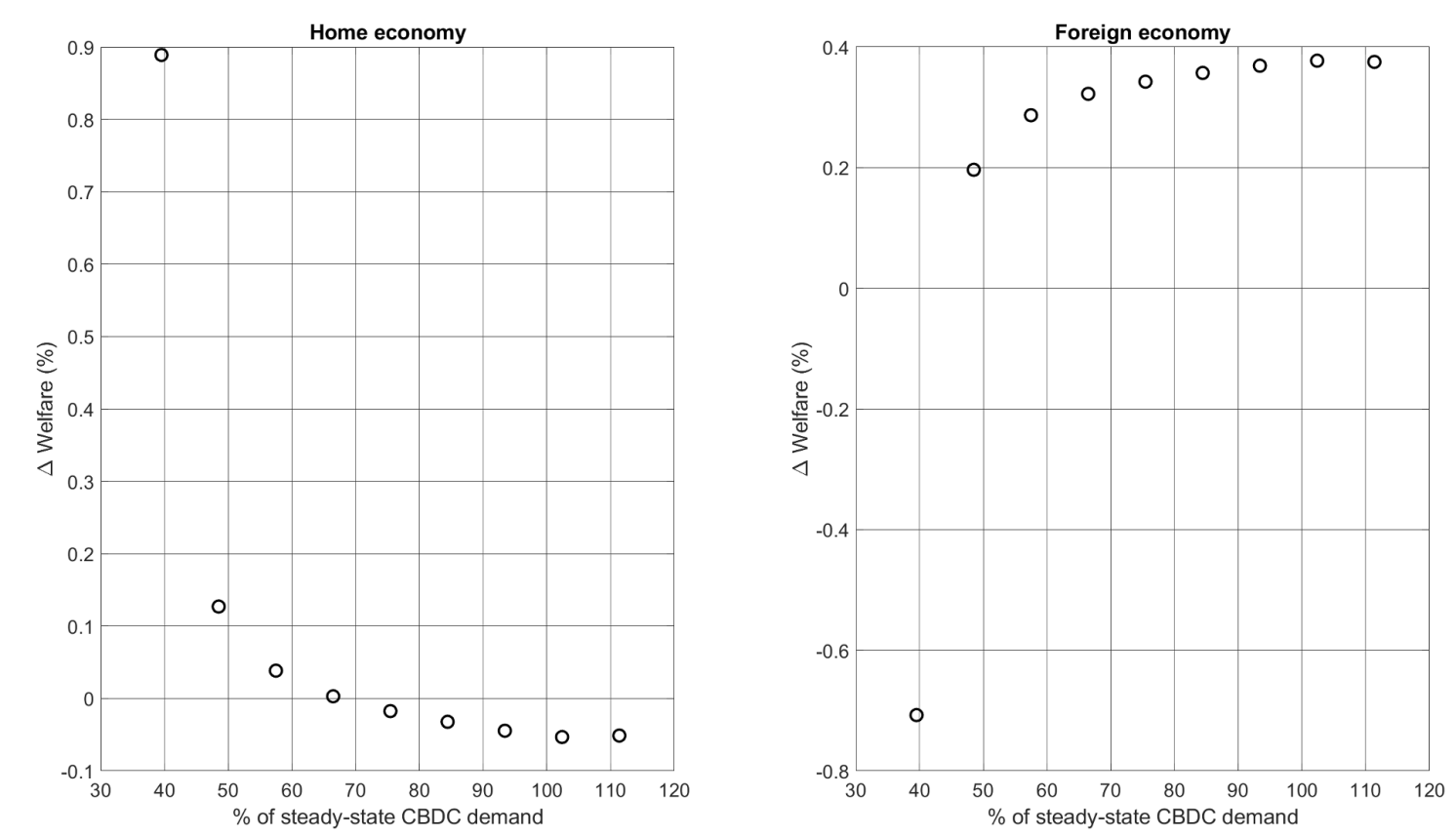

Figure 3 Welfare gains (or losses) for alternative levels of central bank digital currency holding limit

Note: The figure shows the change (in percentage points) in welfare relative to the steady state without a CBDC for alternative levels of the CBDC holding limit during the transition, expressed in percent of steady-state demand.

Finally, we investigate how alternative policies reduce volatility during the transition. We consider different instruments. First, the presence of soft and hard holding limits; second, a two-tiered CBDC remuneration scheme that penalises ‘excessive’ holdings of CBDC by applying a negative interest rate to CBDC holdings above a certain limit; and third, restrictions on non-residents’ CBDC holdings that either preclude non-residents to hold CBDC or result in higher cross-border transaction costs in CBDC for non-residents. In addition, we investigate whether active central bank balance sheet policies, where the central bank purchases private-sector assets to balance CBDC issuance, are effective in smoothing the transition. All policies are only active during the transition and terminated in the new steady state. We find that binding caps, reported by the black line in Figure 2, are most effective in reducing disintermediation and output losses in the transition and in minimising international spillovers. Simulations show that initial output losses in the transition are reduced significantly, while deposits may even increase. That happens because demand for bank deposits is no longer crowded out by excess demand for CBDC in the initial periods, as CBDC is supplied gradually to consumers. During the transition, therefore, households are constrained in the amount of funds they can hold in CBDC and adjust deposit holdings only gradually. This provides the banking sector with sufficient time to adapt to the new environment, in turn helping to keep loan supply and investment more stable. Overall, binding caps limit excess demand for CBDC and prevent disorderly withdrawal of bank funding, thereby stabilising credit supply and mitigating output losses, which yields welfare gains during the transition phase to the new equilibrium. Our simulations suggest that the optimal level of holding limits that minimise welfare losses is around 40% of our simulated ‘high steady-state CBDC demand’ (see Figure 3).Applying this calibration to the euro area, back-of-the-envelope calculations suggest that a limit close to €3000 per capita would be effective in managing excess demand.

Source : VOXeu

.jpg")

")

")

.jpeg")

")

")

")

")

")

")