Firms seem to have responded to rising carbon costs by adapting rather than relocating their business operations. This column uses a comprehensive measure of carbon costs and data on over 3 million firms from 32 countries from 2000 to 2019 to show that carbon costs hardly depressed the performance of an average industrial firm. While limited employment reductions are observed, a large number of firms ramped up their investments in response to higher carbon costs, and losses and exit probabilities have not noticeably increased.

To achieve international and national climate goals, policies are needed that induce firms to shift from carbon-intensive to carbon-free technologies (Van der Ploeg and Venables 2023). A central concern, however, is that intensifying unilateral climate policies would damage firms’ competitive position and thereby slow down economic activity. Another concern is carbon leakage: firms might want to avoid locally raised costs by relocating to weaker-regulated jurisdictions. Such effects would make domestic climate action less effective with respect to the goal of reducing carbon emissions globally.

Evaluating carbon costs: The ‘Swiss cheese problem’

The empirical evidence on the effects of carbon costs remains scarce. We know quite much about how firms are affected by policies that explicitly price carbon emissions, like the EU Emissions Trading System (EU ETS) and some national carbon taxes (Köppl and Schratzenstaller 2022). But climate policies around the world thus far did not focus on explicit carbon taxation. Even today, about four-fifths of global carbon emissions don’t face an explicit carbon tax (World Bank 2023).

By contrast, implicit instruments like fuel excise taxes, subsidies, and standards have predominantly determined how expensive it is for firms to emit carbon (OECD 2015, Carhart et al. 2022). For instance, Sen and Vollebergh (2018) show that fuel excise taxes typically function like a carbon tax on fossil fuel consumption, and requirements to add a certain percentage of clean fuels to fossil fuels drive up costs in a similar manner. Van der Ploeg and Venables (2023) argue that a transition to lower- or zero-carbon technologies also requires a mix of policies other than explicit carbon taxes. Therefore, in a new paper (Trinks and Hille 2023) we examine explicit and implicit carbon costs stemming from the broad mix of policy instruments.

Now, think of the cost base for global carbon emissions as a Swiss cheese and the weight of this cheese as the total cost burden faced by firms. Explicit carbon prices could be considered one of the many slices (policy measures) of the entire cheese. The slices that have been studied thus far have a relatively small surface area (for example, the EU ETS covers about 4% of global emissions) and have been relatively thin, with historically low price levels. Moreover, the slices contain many holes, i.e. exemptions or conditionalities due to which parts of the slice face no tax.

The large remainder of the cheese consists of implicit carbon costs. Because of this focus on individual slices and the implicit nature of many policy instruments, it is hard to judge how heavy the entire cheese would be and how it would ‘weigh-in’ on firms’ economic performance.

Novel firm-level evidence

In a new paper (Trinks and Hille 2023), we tackle this challenge using two innovations. First, we use a comprehensive measure of carbon costs that helps identify the weight of the total cheese that industrial firms face in various sectors, countries, and over time. We find that taking a broad perspective on carbon costs is important. Our estimates for total carbon costs exceed average explicit carbon prices (Dolphin et al. 2020) by more than a factor of 15 over our sample period. Moreover, the variation studied is considerable: on average, carbon costs more than doubled over the sample period. This variation is comparable with the observed rise of energy prices (e.g. Marin and Vona 2021). The comparatively high level and large variation in carbon costs provide a fruitful basis for learning about the potential impact of intensifying climate policies.

Second, the measure of carbon costs is linked to rich global microdata about industrial firms’ production activity and performance to contribute to generalisable results. The dataset covers up to 3.1 million firms in the period 2000–2019. It spans 32 countries which together make up three-quarters of global carbon emissions. The study evaluates the impact of rising carbon costs on a broad set of firm performance outcomes.

The effects of carbon costs are limited and concentrated

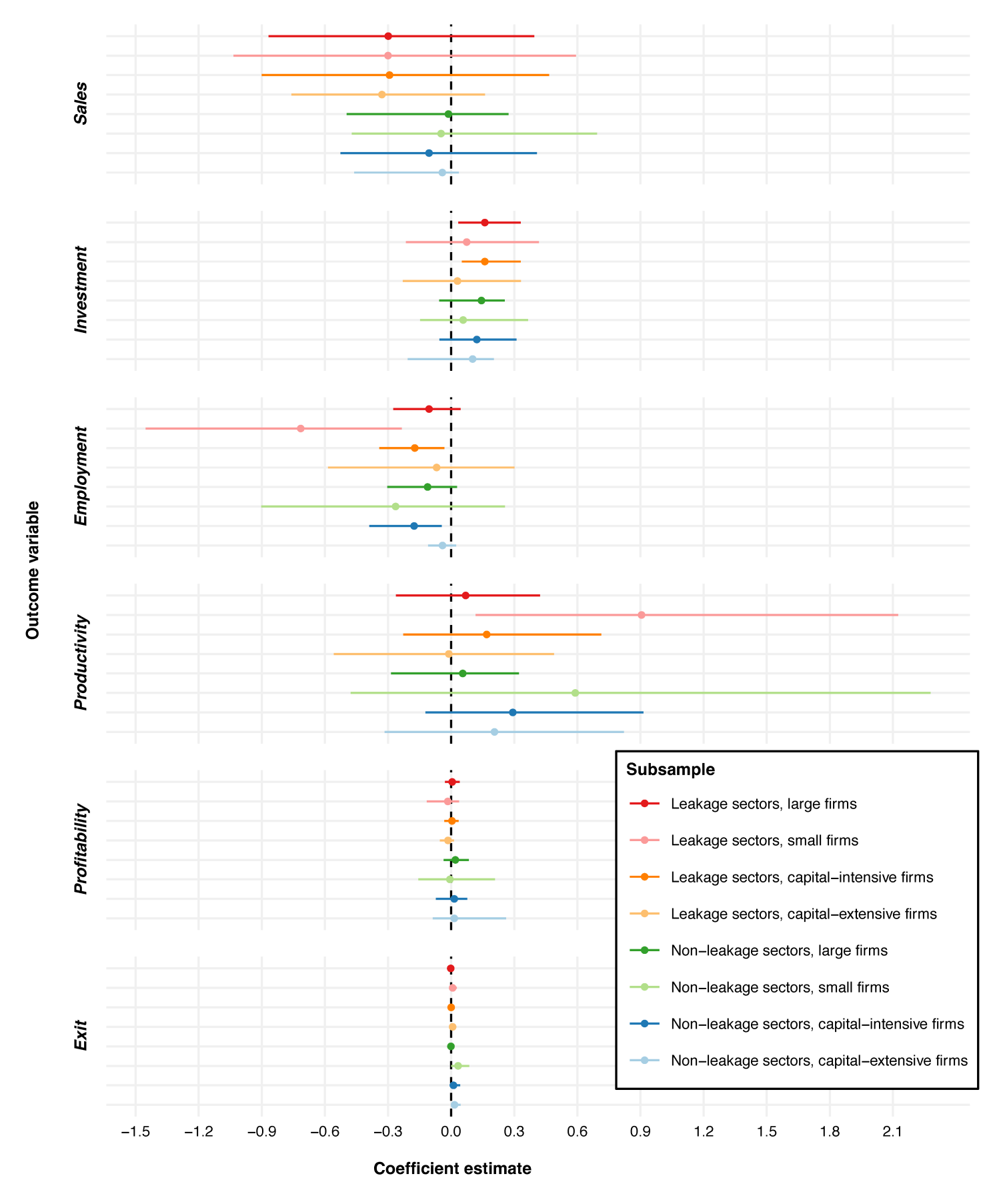

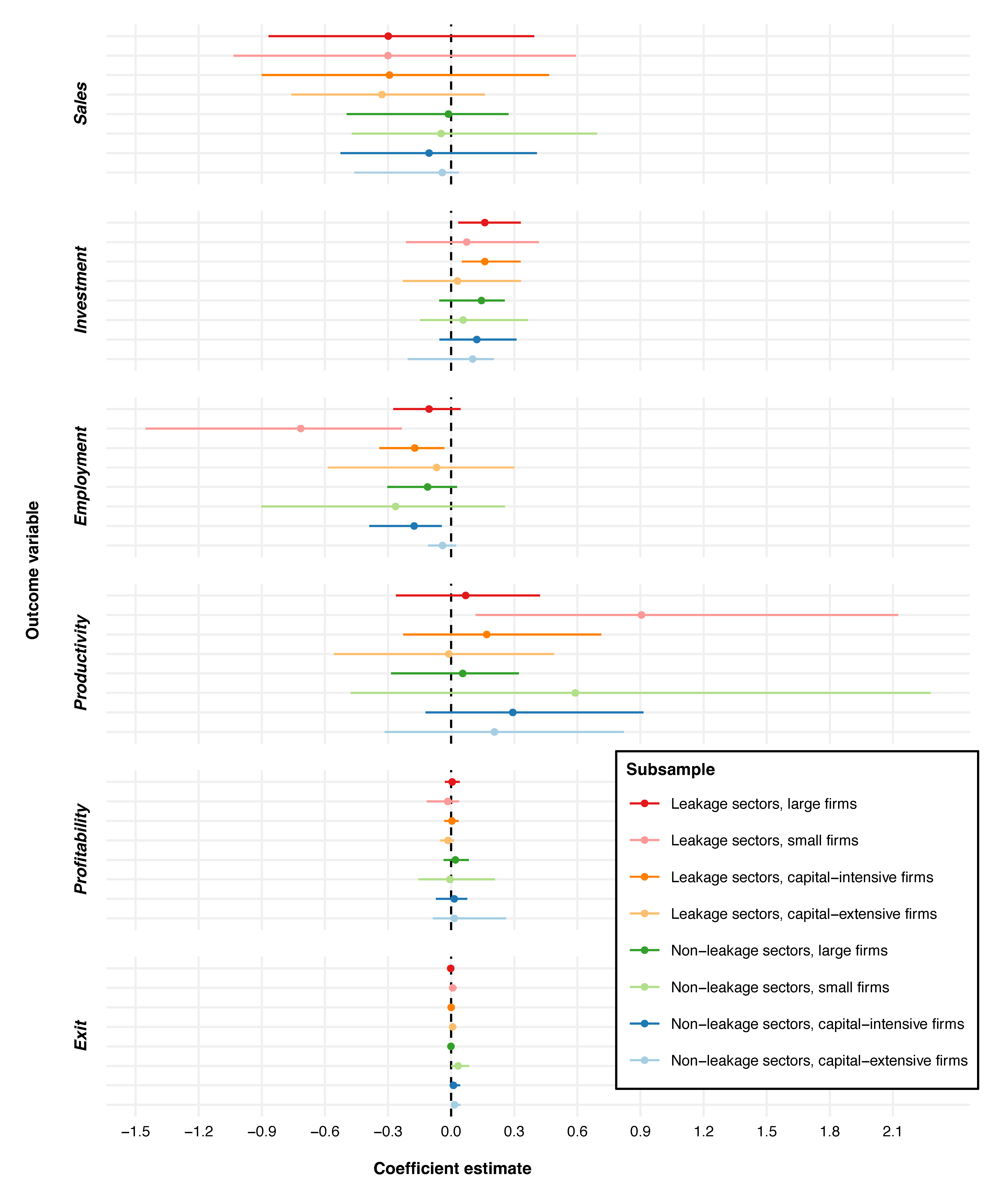

We find little evidence that carbon costs damage the performance of an average firm. This seriously questions the view that higher costs of emitting carbon would impair firm performance and induce firms to look elsewhere. But the impact differs across subgroups. Performance effects are most pronounced for sectors sensitive to leakage effects and for EU countries. Figure 1 visualises the impact of several subgroups of interest. Specifically, we observe modest employment reductions in capital-intensive firms (which also tend to be carbon-intensive) and in the smallest firms in leakage-prone sectors, such as mining, cement, and basic metals. In the latter, productivity improves alongside the decline in employment. The employment effects are generally in the order of 2% for a USD 50/tCO2e increase in carbon costs. In leakage-prone sectors, we further see that large and capital-intensive firms ramped up investments, while losses and exit probabilities are not increased. The investment effect is generally around 3% per USD 50/tCO2e rise in carbon costs. These findings add to the comparable prior evidence on explicit carbon pricing instruments (Dechezleprêtre et al. 2023, Köppl and Schratzenstaller 2022) and energy prices (Marin and Vona 2021). The findings may be explained by firms’ partial pass-through of carbon costs to customers, the still comparatively modest carbon costs they faced, and adaptations made to their production processes to cope with rising carbon costs.

Figure 1 Effect of carbon costs on performance outcomes in various subsamples

Notes: Dot indicates the coefficient of carbon costs in the baseline model, which can be interpreted as an elasticity for Sales, Investment, and Employment and semi-elasticity for Productivity, Profitability, and Exit; Line indicates the 95% confidence interval robust to clustering at the sector and country level. Note that estimates and confidence intervals for Exit are small and insignificant for all estimations.

Policy lessons

Policymakers may use these findings to help assess the risk of adverse effects of climate policies and to efficiently design these policies. Specifically, three lessons may be learned from our study. Firstly, our analysis underlines the relevance of taking a broad perspective of carbon costs: there is a broad and complex mix of policies that explicitly and often implicitly impose costs on firms. Secondly, accounting for total costs and using very rich microdata on industrial firms around the world, we find little evidence that carbon costs negatively impact firm performance. In some specific subgroups, we see some employment reduction but these are modest and tend to be accompanied by productivity improvements. Thirdly, the positive investment effects, together with no noticeable increase in losses and exit probabilities, provide indications that firms responded to rising carbon costs by adapting rather than relocating their production processes. Indeed, firms’ investment and locational decisions are also driven by their expectations about future carbon costs (Trinks et al. 2022). A policy lesson, therefore, is that policy instruments should be aligned with targets and predictable to allow firms to anticipate and not be surprised.

Going forward, the risk of relocation and leakage might become more important if ambitious climate policies were introduced in one country but not in others and consumption patterns would not change. To understand such effects, our empirical analysis can be supplemented with trade model analyses to inform about potential long-term sectoral effects (e.g. Bollen et al. 2020, Hoogendoorn et al. 2021). The present evidence, however, underscores that climate policies can be strengthened with limited economic damage to firms.

Source : Reuters

")

")

.jpeg")

")

")

")

")

")

")